Table of Contents Show

Weak demand globally, along with the potential impact of the incoming Trump administration, has caused yet another delay in unwinding OPEC’s production cuts.

Now, instead of unwinding over 2025, OPEC is telegraphing a much longer period, from April 2025 through 2026. This addresses the core problem with OPEC’s prior strategy: Markets didn’t believe global economic activity would quickly rebound and allow for a rapid unwinding of the cuts.

A slower unwinding reduces the impact on price. Even so, forecasters expect supply growth to exceed global demand growth in 2025. Economic activity would have to accelerate, perhaps from greater stimulus in China, to allow OPEC to add back barrels without driving Brent lower.

Potential tariffs and sanctions under the new presidential administration could hit the global economy hard and slow activity, which is likely why the cuts aren’t set to unwind until the end of Trump’s first 100 days. So, we’re uncertain whether OPEC will turn the taps back on in April.

On the gas side, US gas producers remain challenged in the closing months of 2024 as low gas prices and unexpected productivity in basins dampened activity. However, we think the outlook for this resource is improving. And European storage draws are deeper and ahead of schedule, indicating a rough winter and elevated summer refilling season.

The European gas market’s main concern is its sensitivity to perceived supply disruptions, with various events contributing to significant near-term gas price volatility, including the expiration of Russian supply contracts by the end of 2024.

Here, we outline our expectations for the oil and gas industries and the companies that are best positioned to succeed amid this environment.

3 Key Themes for the Oil & Gas Industries

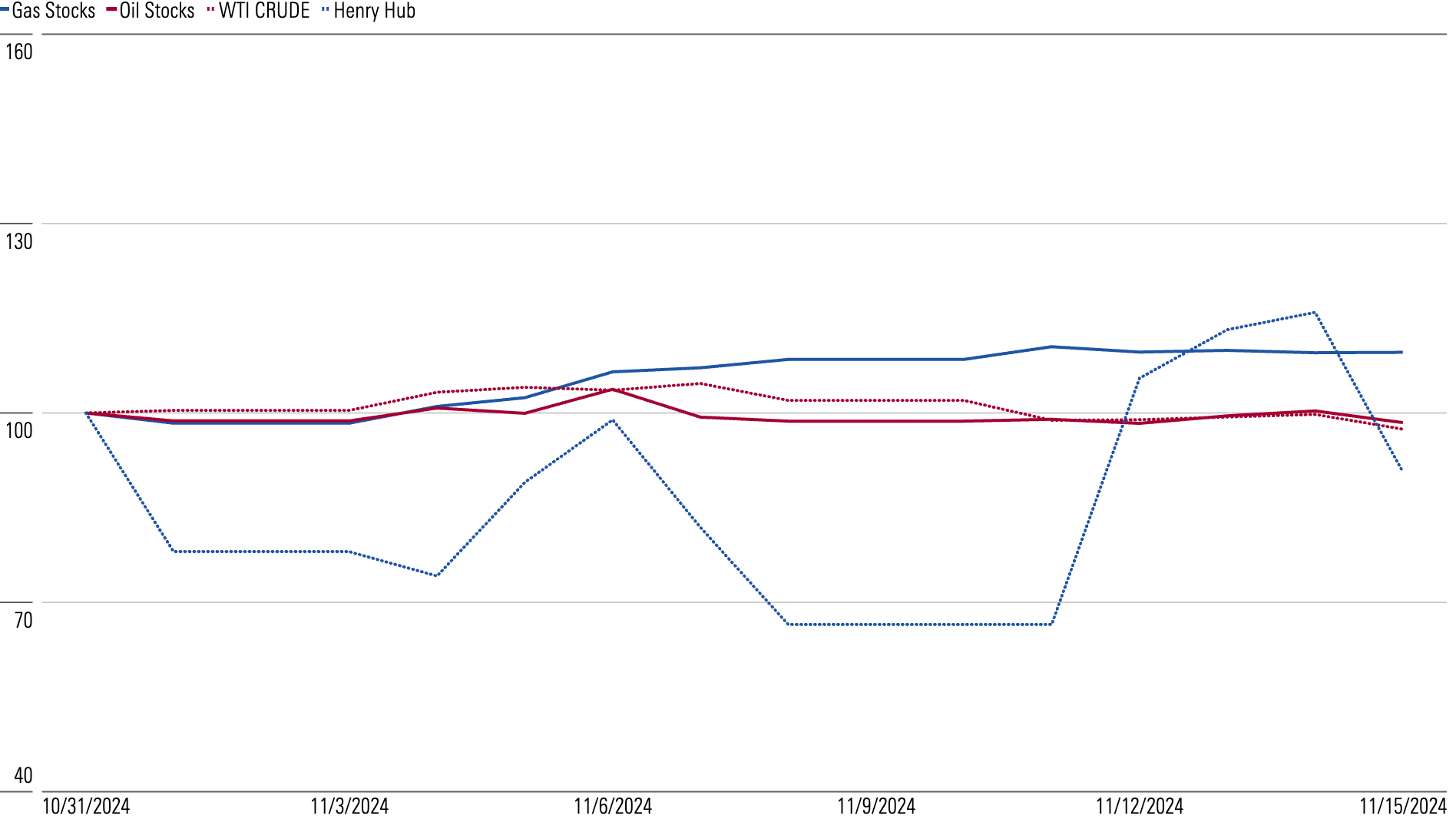

Supply concerns continue to pressure oil prices. Unsurprisingly, oil prices are taking a hit this quarter, as supply concerns remain the top focus for investors. OPEC revised its plans, pushing the unwinding of its supply cuts back to April, but we remain skeptical it can keep this timetable. Demand data over the next month or two is likely to heavily influence OPEC’s decision on future extensions. Further oil price downside remains highly probable. We expect OPEC will extend the supply cuts past April, especially if the incoming Trump administration follows through on promises of tariffs and sanctions.European liquefied natural gas prices bolstered by winter conditions. Asian LNG prices dipped as Japan reduced its natural gas usage. On the other hand, European LNG prices spiked due to rapid drawdowns on stockpiles, signaling that the region will experience a cold winter. LNG prices are now low enough in Asia, where price-sensitive consumers like China and India are ramping up imports. In the US, Henry Hub prices dipped due to the aftermath of several hurricanes. However, we don’t expect them to trough for long. Hurricane season is over in the US, and winter seasonal patterns should lift gas prices.Market is uneasy on oil oversupply resolution. Uncertainty surrounding global oil supply and demand has weighed on stock performance for oil producers. Oil names like Devon DVN and Hess HES look undervalued. Instead, the market has pivoted to gas-leveraged names. Potentially higher gas demand, driven by AI and data center applications and new LNG production, supports elevated North American natural gas prices by the end of 2025. Watchlist names include EQT EQT and Antero Resources AM, as well as Kinder Morgan KMI, Williams WMB, and Enbridge ENB.

Our Overview: Oil & Gas Industries

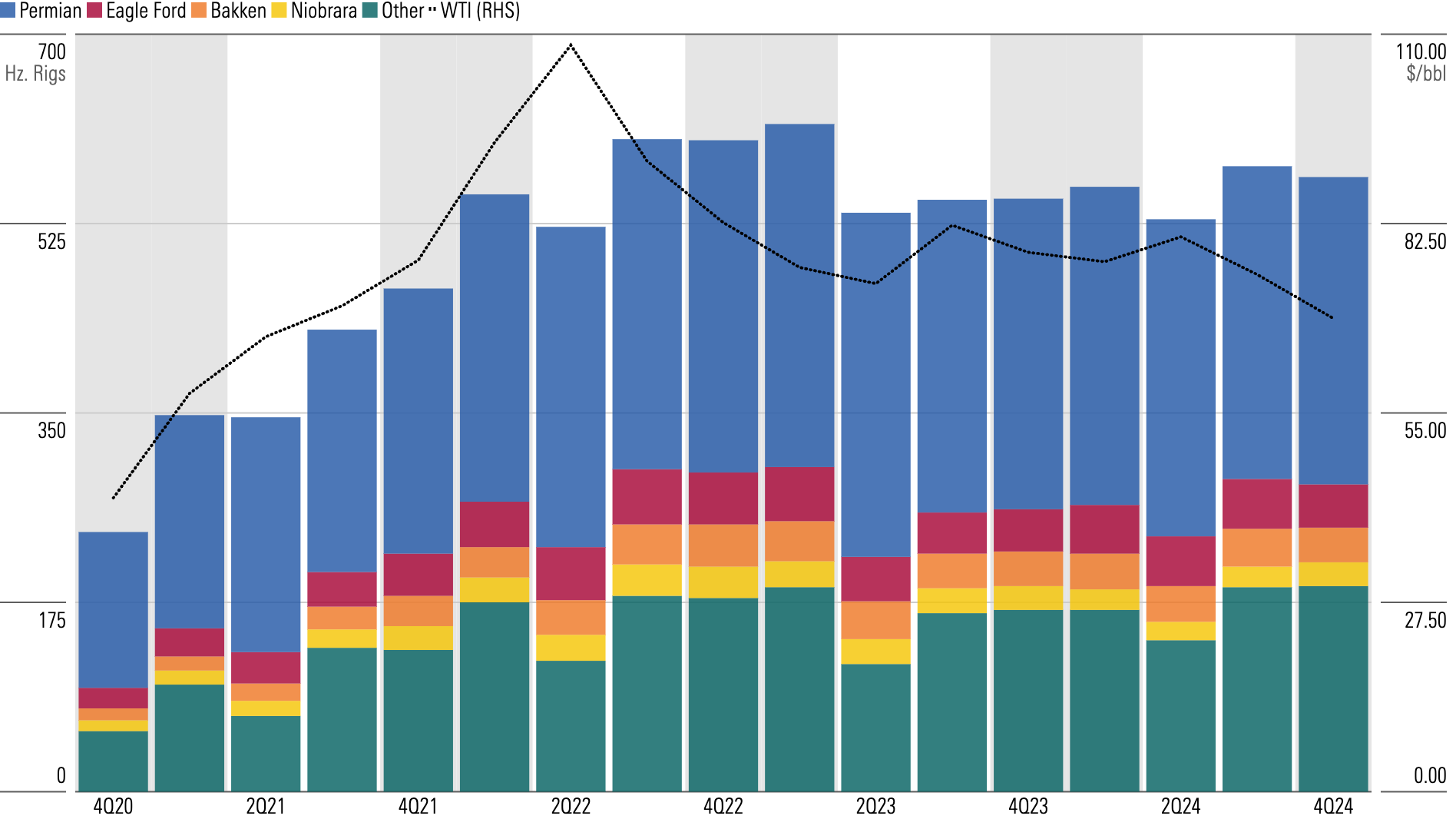

Ongoing US exploration and production consolidation will likely pressure oil rig activity levels.

Consolidation and productivity in the Permian basin drove a slight sequential decline in rig activity. However, activity in other basins more than offset those production declines.

While there was a slight uptick in total production from the third quarter, we don’t see any catalysts to drive activity in the near term. Oil markets remain well supplied, with concerns about oversupply continuing to weigh on prices as geopolitical risks fade.

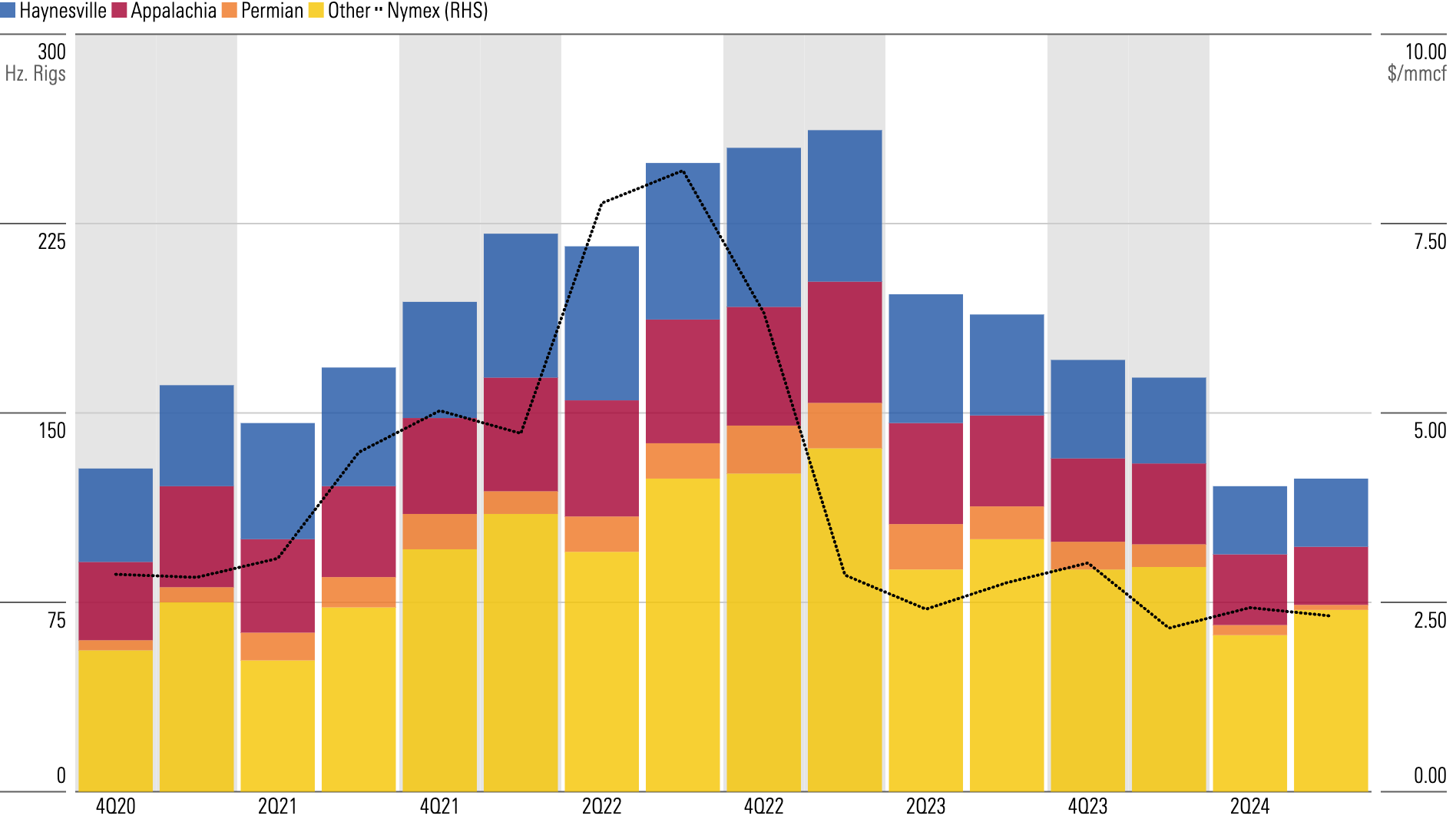

On the gas side, we think the outlook is improving, but that doesn’t mean more drilling activity.

Rather, we expect US gas producers will focus initially on previously shut-in wells or deferred wells for near-term production gains at minimal cost before adding rigs.

To meaningfully increase drilling activity, producers would need to see sustained higher gas prices. We are watching for AI and data center demand to help the near-term 2025 domestic outlook and new US liquefied natural gas export capacity to boost 2026 expectations.

What the Trump Administration Could Mean for Oil and Natural Gas Stocks

The results of the presidential election led to a sharp diversion in the performance of our covered exploration and production stocks.

Oil firms remain anchored to West Texas Intermediate, but gas producers became untethered from Henry Hub.

Trump had campaigned on unlocking energy production, but we think materially higher oil production is unlikely given the already existing oversupply of oil, continued efficiency gains in producers’ current operations, and US producers’ incentives.

While oil production will likely remain constrained, natural gas should benefit far more from a lighter regulatory touch. A shift toward greater deregulation and faster permitting should remove barriers for LNG facilities, while new power plants should bolster US demand.

4 of the Most Attractive Energy Picks

Energy sector bargains have sharply declined this year. Of our energy coverage, 28% remains undervalued (4 or 5 stars), compared with 34% in our last report.

Our top picks in the energy sector include:

HF Sinclair DINO: Recent mergers and acquisitions activity should help the firm capture a growing renewable diesel business. We also expect management’s strategy to improve the efficiency and reliability of its portfolio.Schlumberger SLB: Despite near-term cyclical weakness, we like SLB’s long-term offshore project opportunity, its digital investments, and its upside from a successful integration of ChampionX.Hess HES: The stock’s discount persists, given anxiety over the proposed Chevron acquisition and Exxon’s arbitration with Chevron. One party should close the deal, but Hess’ assets look attractive, even on their own.ExxonMobil XOM: Exxon plans to double earnings and cash flow from 2019 levels by 2027 on a combination of structural cost reductions, portfolio improvement, and growth across its upstream, downstream, and chemical segments.

|

Stock |

Ticker |

Morningstar Rating |

Fair Value Estimate (as of Dec. 19, 2024) |

Price/Fair Value Estimate (as of Dec. 19, 2024) |

Uncertainty Rating |

Economic Moat |

|---|---|---|---|---|---|---|

|

HF Sinclair |

4 stars |

$58 |

0.60 |

Very High |

Narrow |

|

|

Schlumberger |

4 stars |

$57 |

0.65 |

Medium |

Narrow |

|

|

Hess |

4 stars |

$178 |

0.73 |

High |

Narrow |

|

|

ExxonMobil |

3 stars |

$135 |

0.79 |

High |

Narrow |

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.