Table of Contents Show

The Bond Markets Weak Links – When Will Things Break?

From Our Audience

__________________________________________________________________________________________

THE BOND MARKET’S WEAK LINKS? WHEN WILL THINGS BREAK?

Chris a couple Q’s after your awesome recent discourse on the “math” we ALL face (not just your favorite president, ha ha!)

What do you see as the weakest link(s) that could cause a full-on crisis for Treasuries and the rest of the markets? Dumping by China as tariff retaliation? Others?

You and others for some time have suggested the day will come when yield curve control becomes a necessity to stave off full collapse, and to make the “math” easier for funding/refunding government debt. On that what do you make of (Treasury Sec. Scott) Bessent’s suggestions of targeting the long end of the Treasury market…?

__________________________________________________________________________________________

First off, it’s been grossly overrated (more often than not by the usual scare monger suspects out there) the extent to which China especially would have the ability to punish the U.S. or our Treasury

markets by “dumping” U.S. paper. As you see in the nearby chart from a great and exhaustive look at the Treasury market by Wolf Richter back on Christmas Eve (read it at https://wolfstreet.com/2024/12/24/who-bought-and-holds-the-recklessly-ballooning-us-national-debt-even-as-the-fed-is-unloading-its-holdings/) China about then held just under $1 trillion of the $36+ trillion of Uncle Sam’s I.O.U.’s.

Hayman Capital’s noted China hawk Kyle Bass recently updated that number to, lately, something like $750 billion. Further, making the same point on this that Richter did, he explained that of all the things to be concerned about where China is concerned, their holding roughly 2% of all outstanding Treasury securities is decidedly not one of them (see https://www.youtube.com/watch?v=4nIytIv9BWk.)

With tariff wars heating up as I am writing this, there is, to be sure, renewed talk of there being less foreign demand, net, for U.S. paper in the years ahead. In part, this is due to the reality that—assuming Trump’s mercantilism leads to reducing America’s overall trade imbalance with the rest of the world—it would simply translate into less need for trading partners to hold/trade in dollars, period. As I have mentioned in times past, nobody seems to have explained to the president that—when you have the world’s reserve currency and, as Trump is demanding, everyone must use it or face punishment—by definition you MUST run trade imbalances, all else being equal.

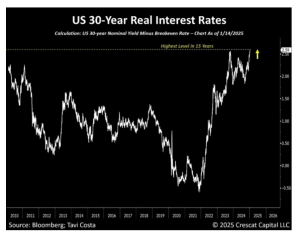

But even on this subject, I don’t see any reason to anticipate some sudden comeuppance for Treasuries or the U.S. currency. Indeed, on the former (as I discussed over the past weekend) Treasuries have been on a scorching and near-panic rally suddenly in anticipation of economic weakness and such. Added to that the last few days is the Atlanta Fed’s view that Q1 G.D.P. may actually contract by 1.5% when we get the number.

Notwithstanding that, the big “threat” to Treasuries as I still see things is the ongoing inflation impulse and the sheer volume of debt that needs to be rolled over/issued. And I should specify that the threat is less to the government’s ability to place all this paper but to people who buy it and suffer the kinds of additional capital losses we’ve seen over the last few years. Sure, we may see yields soften a bit more in the months ahead as the economy weakens, investors become more skittish, etc. But the long-term supply issue is still front-and-center as a reason why nobody at this point should think this is a great buying point to get in to Uncle Sam’s I.O.U.’s.

I found it interesting when Bessent a few times, actually has floated the notion that his boss wasn’t (for now) going to browbeat Fed Chairman Powell over the federal funds rate but instead focus on “bringing down” long-term borrowing costs set by the bond market. For the most part he’s repeated his plan dubbed “3-3-3” — which aims to get the deficit down to 3% of GDP from above 6% by cutting regulation, sustaining growth of 3% and boosting oil production by 3 million barrels a day.

As I have explained a few times in recent weeks, there’s a snowball’s chance in Hell of achieving this. Further, both the House and Senate budget frameworks recently passed will add several trillion more to the overall debt over the next decade; the latter’s measure being an especially odious continuation of Washington pork spending. But not to be outdone, House Speaker Johnson is suggesting again that he’s going to drop back and punt via a C.R. (Continuing Resolution) once more, funding the government for a while at 2024 levels despite those levels under more scorn than ever thanks to what the D.O.G.E. effort has been revealing.

All this will be coming to a head over the coming couple weeks as the budget fight and Trump’s quest for his “one big, beautiful…”er, I mean “ONE BIG BEAUTIFUL BILL” runs into that wall of reality and that recalcitrant “math.” If the president (again) meekly signs off on the Johnson/Thune Swamp spending levels as usual (as he did last time) without even a whimper of protest, it will vindicate the bond market vigilantes and keep upward pressure on long term Treasury yields, all else being equal.

On the day Trump was inaugurated for the second time, Jim O’Neill, the former chairman of Goldman Sachs Asset Management and a former U.K. Treasury minister, wrote of this looming “first big test” of the president when it comes to the bond market; see https://www.project-syndicate.org/commentary/trump-bond-market-first-big-test-by-jim-o-neill-2025-01. Without some significant sign that Trump will even forcefully call out the G.O.P. leadership over its already-exhibited spending priorities (which—in case you missed it—includes massive additional spending for the military in the Senate-passed bill, among other things) he’ll be at odds even more with the bond vigilantes.

Add to the that the tax cut extensions, more new tax breaks and the rest—and the likelihood that what savings from D.O.G.E. spending cuts/waste and fraud eradication efforts do survive won’t move the needle sufficiently—and the “book” on Trump 2.0 will be galvanized. And that will be enduring and even rising inflation and interest rates to go along with that, even if the economy loses some steam.

Time will tell at what point, if this plays out as unfortunately seems more likely, rates have stayed/risen sufficiently high for long enough to cause Trump and Bessent to do something overt to cap long-term yields. While I am overjoyed to see the extent to which Elon Musk and his team have revealed just how deep the rot, grifting and everything go in the federal budget most everywhere, we need to be realistic about the notion that the majority of the House and Senate alike will continue things as is if they can get away with it. That will mean a more stark fiscal crisis; and yes—at some point it will force drastic measures to cap borrowing costs.

For now, Bessent will hold the party line and claim (with other Cabinet mates and the president himself) that tariffs will NOT lead to a rise in costs for American businesses and consumers (generally false) and that his “3-3-3” plan will work to bring inflation and interest rates down, as regulations are also trimmed (generally Wonderland forecasting.) I’m actually surprised we haven’t heard the term “voodoo economics” resurrected! But what Bessent has done is to fire a shot across everyone’s bow, I.M.O. in stating the goal of reducing Treasury yields in the market.

OMINECA NEWS?

Chris – While I saw that you reposted the news Omineca just put out as well as some thoughts from Dean (Nawata) I was hoping for more color commentary from you. Don’t know if I’m a little desensitized or what, but once again it didn’t strike me as anything much beyond “Hurry up and wait.” I just don’t get the continued delays…WHERE’S THE GOLD?..

________________________________________

The February 24 news (at https://ominecaminingandmetals.com/news/omineca-announces-operational-re-start-of-the-underground-placer-gold-recovery-program-at-wingdam/) did on the surface leave some sense of a continuing “running in place.” But, it does seem that, at last, gold is going to be pulled from underground and start to be reported on in the coming few weeks.

Expanding on what the P.R. said, the delay from when it looked like we were at this stage late last year was due to the government asking additional questions about the rejiggered excavation plan. As C.E.O. Tom MacNeill reminded me when we talked a couple days after this news came out, the company did respond to the B.C. ministry promptly. But by that time, folks were starting to leave for the Christmas holidays and Omineca was left in limbo for a stretch once more.

And an added delay due to that was that mining workers who were standing by twiddling their thumbs for the most part (though some time was utilized in testing and retesting equipment, fixing what was necessary etc.) ended up going elsewhere temporarily to work on other gigs.

But now everyone needed is back and everything is in place. So, barring Mr. Murphy making a surprise return visit, MacNeill was optimistic that the next news from underground will finally be of the first recovered gold.

I also asked about assay results from the recent underground drilling. They have been incrementally coming back to TerraLogic and—as was his view when we spoke—will likely be released all in one batch once compilation and analysis is done.

DID YOU FORGET FRONTIER?

Thanks for your recent segregating of those companies you are most keen to double down on; I’ve followed the advice on most. Wondering why Frontier Lithium, which you’ve always spoken well of, was not on the list (unless I missed something)…

_______________________________________________________

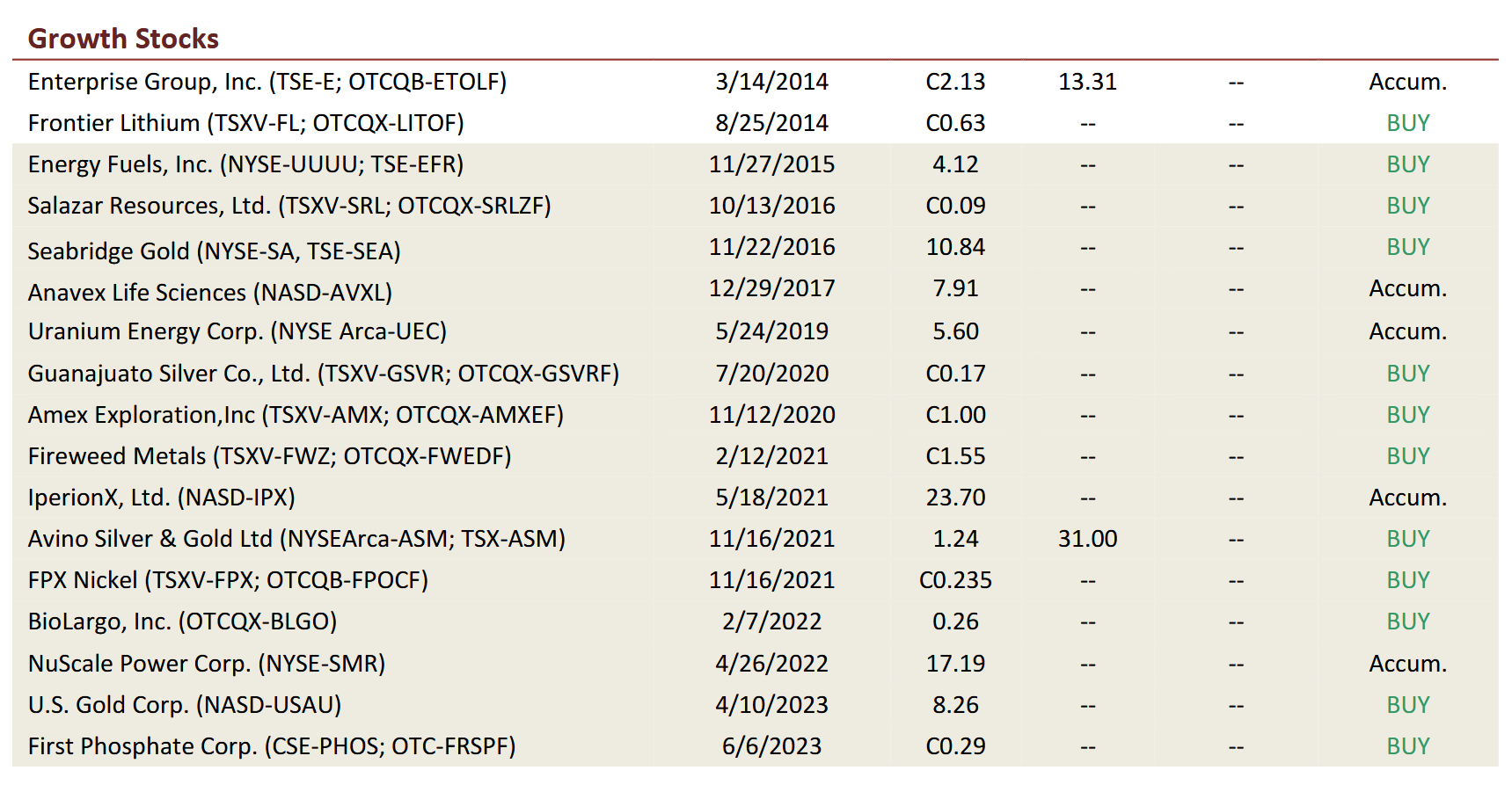

No, you didn’t miss anything. Notwithstanding my confidence that Frontier shares will eventually get back up closer to where (if nothing else) last year’s Mitsubishi deal valued them, I continue to worry that it’s going to be a long slog. That number, lest you’ve forgotten, was around C$1.50/share; nowhere near where we thankfully cashed in some chips around the C$4.00 all-time high, but more

than double the current share price.

The big “macro” issue is that the lithium price itself is unlikely to stage a decent, sustained rally for some time to come. I am regularly on calls/webinars with several consultancies and experts that specialize in battery/base metals fundamentals; and every single one of them by and large holds that we’re at least a couple years from the present renewed oversupply being worked out AND there being more clarity on future demand trends.

I’ll have more color on those prospects in the near future, together with that for other base and battery metals.

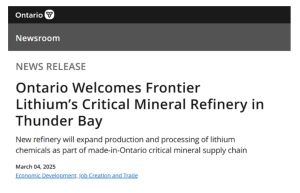

Some good news just came out for Frontier uniquely, though, as I already just shared earlier this week on Tuesday (and clarified Wednesday) at https://mailchi.mp/frontierlithium/fdprnvintnt and https://mailchi.mp/frontierlithium/fdprnvintntcrrctn, respectively. And that is in the form of a Letter of Intent from both the federal and Ontario provincial governments that would bring significant cooperation and funding for Frontier’s proposed lithium conversion facility in Thunder Bay, Ontario.

FL shares jumped on the initial news to around C80 cents before pulling back on the correction. While it was nice to see that bit of renewed life, my take is that this, too, will be a long process, albeit “juiced” a bit now by government resolve in the would—be 51st state to accelerate whatever needed to develop resources and get them to markets everywhere. In the end, while I continue to view Frontier’s world class PAK/Spark resources and growing complex as woefully mispriced, getting something closer to fair pricing is going to remain hostage to the broader funk for lithium generally for quite some time, I fear.

SEABRIDGE OUTSIZED DROP ANYTHING TO WORRY ABOUT?

Chris, I know that PM stocks overall were pulling back in Q4 last year, but I’ve been startled by the extent of Seabridge’s drop. Shocker especially given that it’s hardly the typical junior but has such large reserves!

How worried should we be about this, or is it overkill/overreaction?

__________________________________________________________________________

It’s looking the last several trading days as if at least some realize that the drop in Seabridge was overkill. Its shares recently bounced to approach the $12 area anew as I write this; still uber-cheap I.M.O. given the nature not only of the reserves/resources at KSM but the several other advancing stories of the company.

The majority of the negative sentiment came courtesy of a legal challenge to Seabridge’s “Substantially Started Designation” for KSM as I discussed at the time (see https://www.seabridgegold.com/press-release/seabridge-s-ksm-project-substantially-started-determination-challenged-by-tsetsaut-skii-km-lax-ha for the company’s November 25 news.) As Chairman / C.E.O. Rudi Fronk explained in it and then to me separately afterwards, this controversy seems (my characterization) a largely manufactured one on the part of a Frist Nations band whose roughly 30 members simply decided not to engage, cooperate or be a part of the public discourse over this whole project just to make their presence known.

There seems to be essentially no legal basis for undoing Seabridge’s designation; however, though even the government “can see right through this,” it’s likely that a decision won’t come for a year or so. The good news is that this nuisance does not in any way seem to be affecting discussions with, now, a reported three “finalist” J.V. partners. And the company has not had to curtail any activities.

“Keep your eye on the prize” is apropos here. As Fronk pointed out again recently, if you use a $2,600/oz. gold price and $4/pound for copper now (both prices are, of course, significantly higher these days) KSM’s first production plan has an NPV of some $15 billion right now against a market cap of under $1.2 billion at this past week’s end.

Elsewhere, life and progress go on, notably at the Iskut Project to the west of KSM. The company recently discussed the remainder of its 2024 drilling and plans for 2025 to, among other things, define an initial resource (see https://www.seabridgegold.com/press-release/seabridge-gold-expands-iskut-s-snip-north-target-and-prepares-to-initiate-resource-definition-drilling-in-2025) later this year. The belief is that Iskut could well host a KSM analogue; as Fronk said in this recent release, “We have defined a large, intense and extensive hydrothermal system that remains open down dip to the West and Northwest. This discovery will be our key exploration focus in 2025, working to delineate a mineral resource as quickly as practical. Our excitement for this discovery is enhanced by the fact that we have not yet found the intrusive source of the mineral system discovered last year. Our expectation is that building resources on Snip North in 2025 will provide critical knowledge transferable elsewhere on the Iskut Property where we see multiple centers with potential for additional discoveries of Cu-Au porphyry systems.”

Aggravating as it’s been to see the soured market sentiment of late, I’ll reiterate that Seabridge remains an advanced exploration play that should be a core holding of your portfolio (and with more news to come still on its other projects apart from KSM.)

WHAT WILL BE SALVAGEABLE FROM ROYAL HELIUM?

…Curious about what if anything you can offer RE: Royal Helium and its progress through bankruptcy. It comes as a shock, of course, especially after your strong advocacy…

__________________________________________________________________

To be sure, even with the unanswered questions and all since the management coup of last summer, I never would have expected to see this. And I wish there was something positive I could bring to a story that over not many months’ time went from all the fanfare of Steveville’s opening (including all the media and government officials taking part led by Premier Danielle Smith, with former C.E.O. Andy Davidson at left)…to initial production challenges…to those being mitigated to a great extent, leading to, I’m told, a total of 18 trailer loads of helium to the company’s chief customer…to the management team being forced out.

I’ve attempted somewhat to piece together the ways in which C.E.O. David Young (who has repeatedly refused to engage with inquiries, even prior to the bankruptcy fling on January 20) has either 1. Just run Royal into the ground and/or 2. Positioned it for a fire sale to some he’s been in cahoots with (which, as some of the history comes out, could lead to other legal challenges.) Regrettably, we’re all flying blind, able to only cling to the notion that the company’s assets, Steveville plant and the rest should be deemed to be of much greater worth than the company’s debt.

So, though I wish I could offer some specific encouragement, we’re all hostage to events and can only hope that, once the process is done, we as the existing shareholders end up with something.

NEWSLETTERS MORE SCARCE?

Chris, Is the era of your newsletters over? Curious, as to your seemingly changing distribution

habits/frequency…

___________________________________________________________________

Not at all…at least once a month I will continue to send out a typical, full-fledged “regular issue” even if the exact timing fluctuates. Sometimes it’s been and will continue to be a couple times/month, though that’s been a bit less so in recent months as I do more smaller, piecemeal items too.

In the coming couple weeks or so you’ll be seeing at long last a revived Members only page with both past newsletters/emails archived as well as added video/audio content. You will still be receiving an email of everything as it comes out, however.

I’ll also shortly be updating a prior Members “handbook” of sorts as a reference. Among other things it will remind everyone that there are generally three different kinds of emails I send out:

1. General market commentary, some interviews, etc. intended for wide circulation to paid

Members and others.

2. “Regular” newsletters such as this one (where almost every time the tables of allocations, specific recommended holdings, etc. are updated) and

3. Other “between-issues” alerts as I have called them, which are simpler-formatted emails that have specific Members-only news, recommendation changes or additions and the like.

As you’ll see in the heading of this issue, one thing I’m modifying is to number ALL Members- only mailings in running order. Chronologically, whether a between-regular issues email or more typical regular issue as is this, they’ll all be in running order so you’ll know if you missed something along the way (General circulation items won’t be numbered at the moment.)

Two more quick notes for now: As I trust you have noticed over time, pretty much no week goes by without me sending you something. So be mindful, too, that without any warning your email server might decide to place this week’s missive from me in your spam folder. Even I at times (and I do scour my own spam folder a couple times per day normally, just to be sure I’m not missing anything) find that items/people I have subscribed to for a long time end up there on occasion.

Secondly, frequency of emails from me will be increasing, net, as I go to more succinct ones generally, so as to have less occasion (with the burden that brings) to send out veritable books as I have sometimes! That should keep things more manageable for you.

MORE ETF & COMPANY COMMENTS

_____________________________________________________________________________________________________

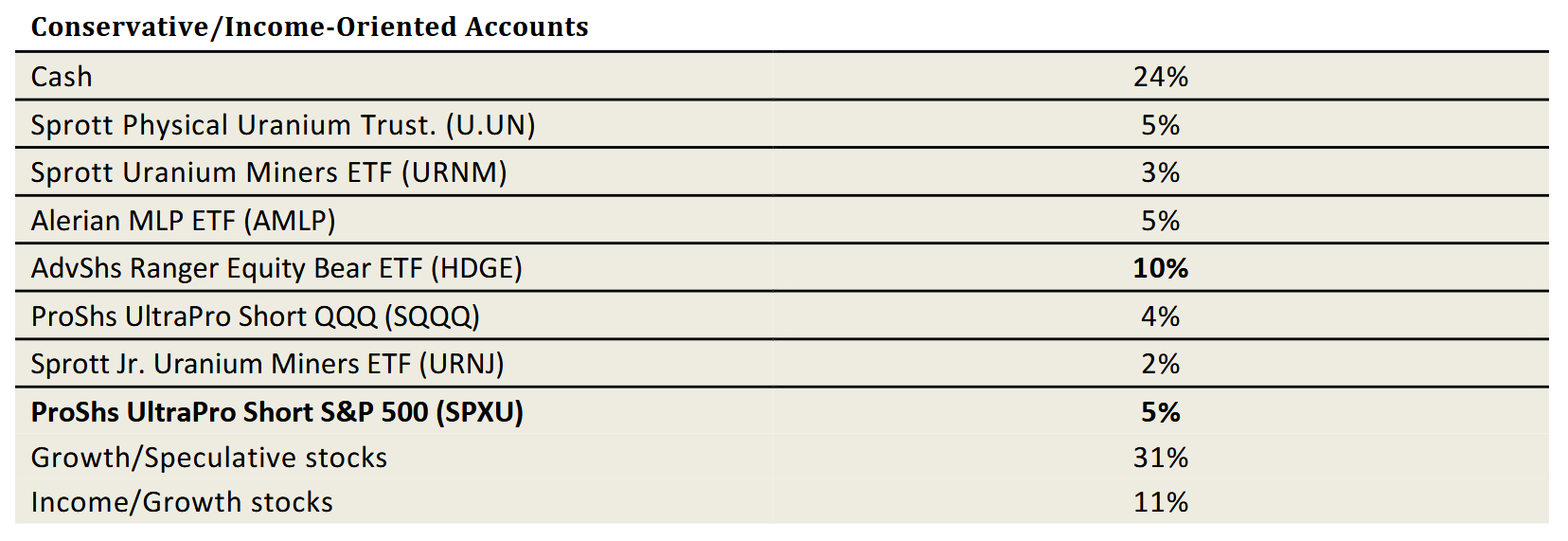

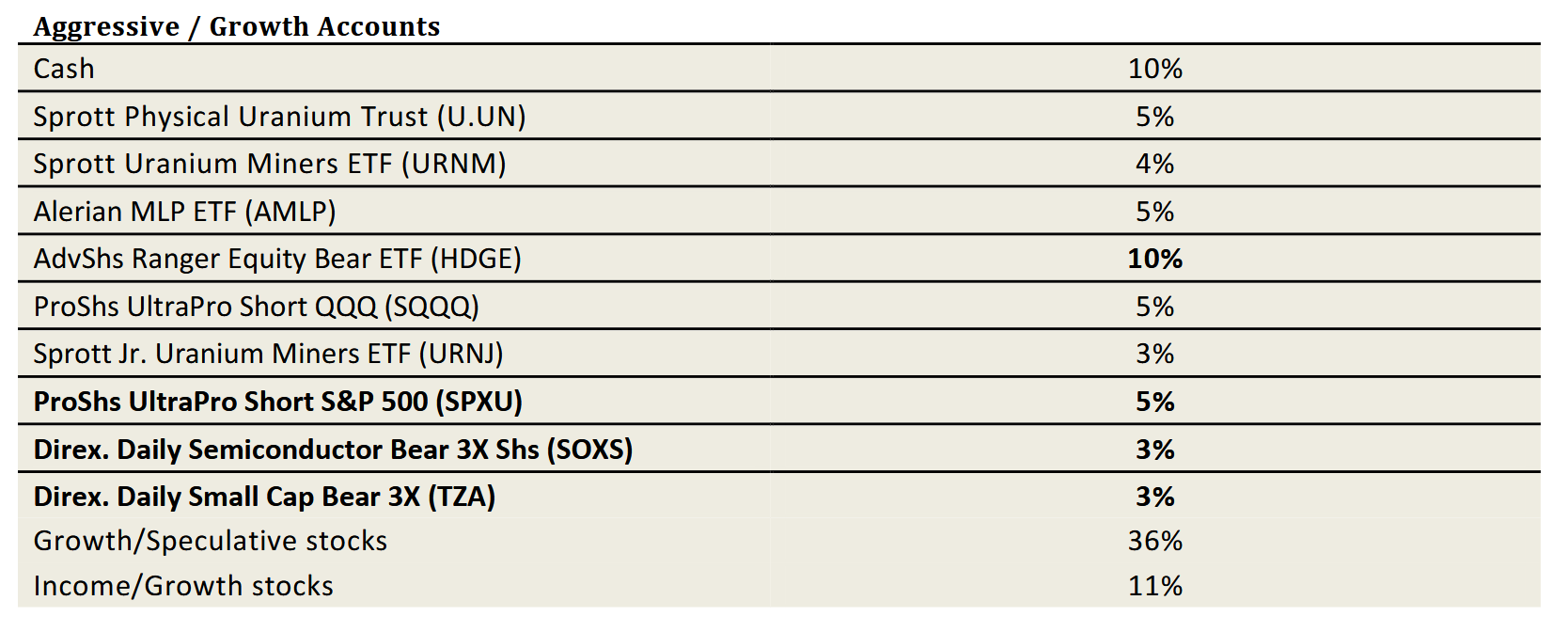

With the unfolding correction now, our game plan increasingly will be to 1. Mitigate/offset the overall market losses via some exposure to inverse ETFs, 2. Selectively look at individual stories and themes alike that will actually do better in the part-stag lationary, part-uncertain environment and 3. Be patient with if not add to “known quantities” whose individual stories are that compelling…and/or where the markets’ throwing babies out with bath water makes them more so. Over the coming few weeks I’ll update everything on our recommended list, prioritizing those with near-term news and/or where the markets have overshot to the downside.

___________________________________________________

First off, the uranium space is one where I am getting close to going back to a BUY on everything. I have said for quite some time that one of the reasons I like the fundamental setup here is that uranium is one commodity that is least likely to suffer a drop in demand no matter the economic outlook (unlike, for instance, oil which has been beaten up—unduly, yes—over relatively more legitimate fears of less demand as recession looms.)

At https://www.ft.com/content/d0faf091-50b4-4878-ae08-ea6dc07db993?segmentId=3f81fe28-ba5d-8a93-616e-4859191fabd8 is a very good piece from a few weeks ago from the Financial Times’ Camilla Hodgson and Ian Johnston on the intractable supply challenges. More so, they explain how—as Scott Melbye and I discussed back in December in our coverage of the overall sector’s dynamics (see https://www.youtube.com/watch?v=jxEfAbFynCU) –evolving global dynamics/relations are going to keep “Eastern” uranium closer to home. And in my view it all underscores here especially that the recent weakness in the sector more in sympathy to the broad markets is unlikely to last very long.

__________________________________________________

Last but decidedly not least for the moment, that still-open private placement I’ve told you of in BacTech Environmental that started with the objective of raising a hoped for “bridge” of C$300,000 has already garnered commitments of near double that and—as the company announced Friday—will now probably close in the neighborhood of more like C$1 million.

At https://bactechgreen.com/press-release/bactech-closes- irst-tranche-of-unit- inancing/ you can read more details of this and more.

The company is most notably on course to file its final patent on its “Zero Waste” technology before April 5th. At that time, it will provide more details on this groundbreaking work which Dr. Paul Miller and the team at Mirarco in Sudbury have accomplished. As I have pointed out, this kind of news relating to a developed nation and established mining jurisdiction like Canada (as opposed to Ecuador, but notwithstanding the robust economics eventually emanating from the Tenguel Project there) will be a lot more dif icult for markets/industry to ignore!

The clock is ticking: if we have not already been in touch on this P.P. and you have an interest, get with Ross or myself A.S.A.P.!

_______________________________________________________________________

Don’t forget to follow my thoughts, focus, occasional news on covered companies

AND MORE pretty much daily ! ! !

* On Twitter, at https://twitter.com/NatInvestor

* On Facebook at https://www.facebook.com/TheNationalInvestor

* On Linked In at https://www.linkedin.com/in/chris-temple-1a482020/

* On my You Tube channel, at https://www.youtube.com/c/ChrisTemple (MAKE SURE TO SUBSCRIBE!)

RECENTLY CLOSED POSITIONS

_____________________________________________________________________________________________________

The current allocation and individual recommendations which follow this section are but a part of our experience/story. Below are those ETF’s and stocks we’ve sold of late (typically, this is about a three month-running list), together with the approximate gain/loss on each. Figures are on a total return basis for dividend-paying securities and also take into consideration specific weighting/trading recommendations during our coverage as appropriate:

Security (stock or ETF)

— Piedmont Lithium (PLL)

— Anavex Life Sciences

— U.S. Natural Gas Fund (UNG)

— ProShares Ultra Bloomberg Nat Gas (BOIL)

— Izotropic Corp. (IZO)

Disposition

Stopped out on 12/13; 47% GAIN on remainder; 494% total GAIN on position

Partial sale 1/13; 140% GAIN from Dec ‘17etc

Sold 1/13; 24% GAIN from Feb ’23, etc

Sold 1/13; 17% GAIN from June ’24 etc

Partial sale 1/22; 230% GAIN from Jan ’21,etc

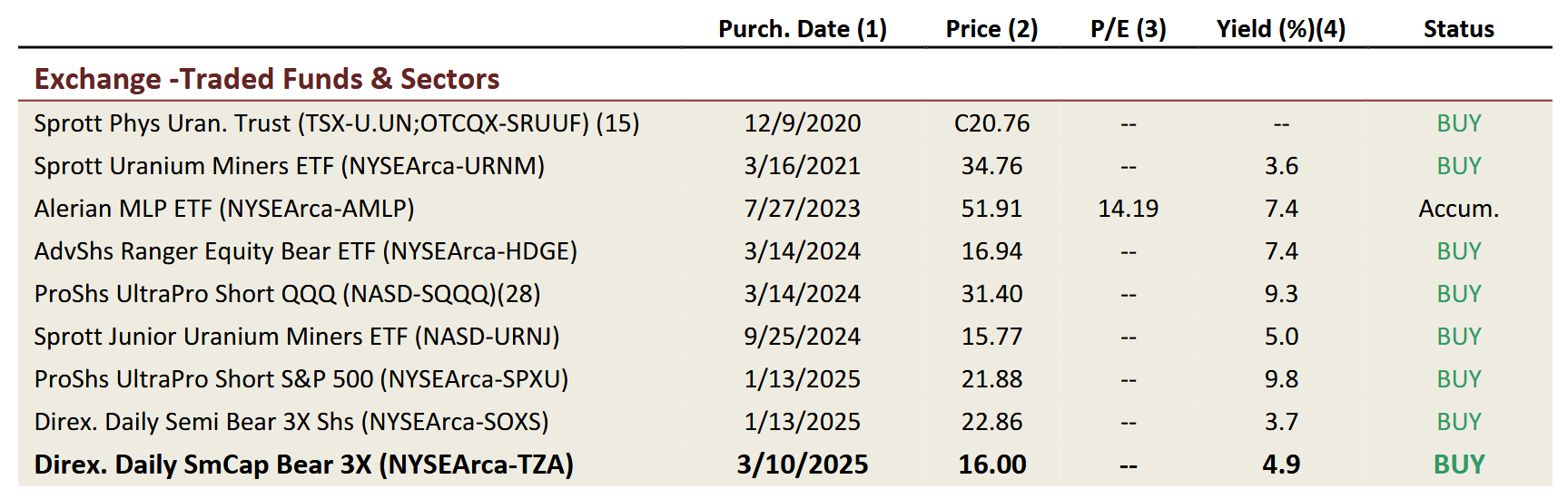

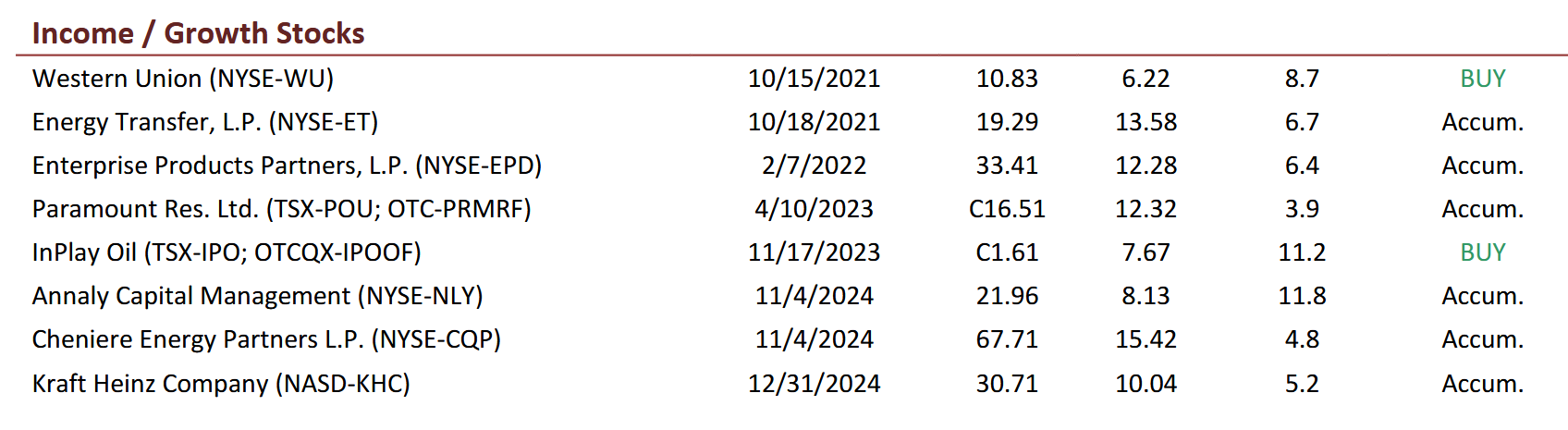

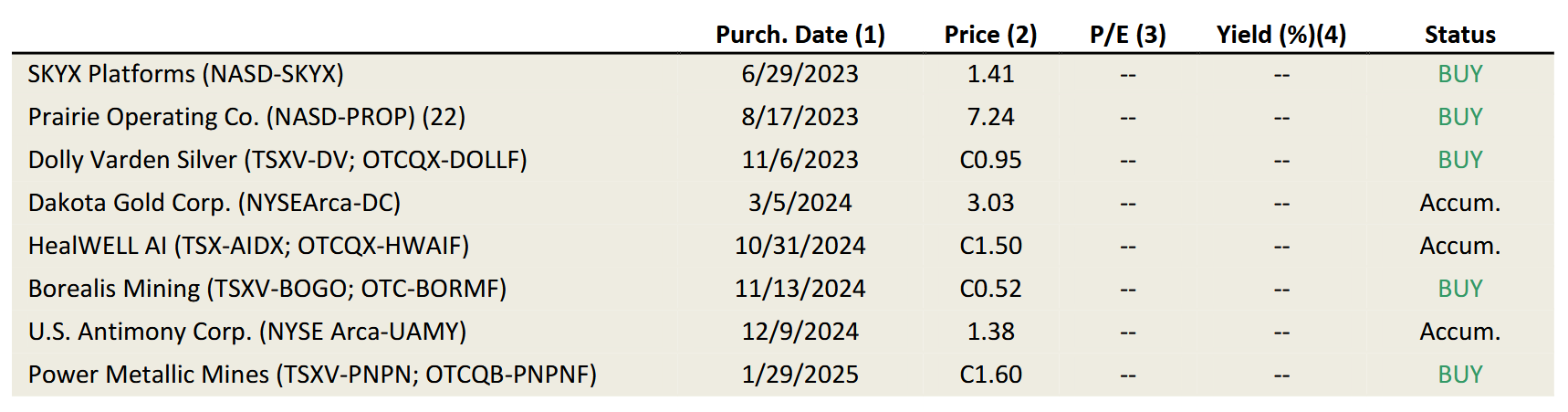

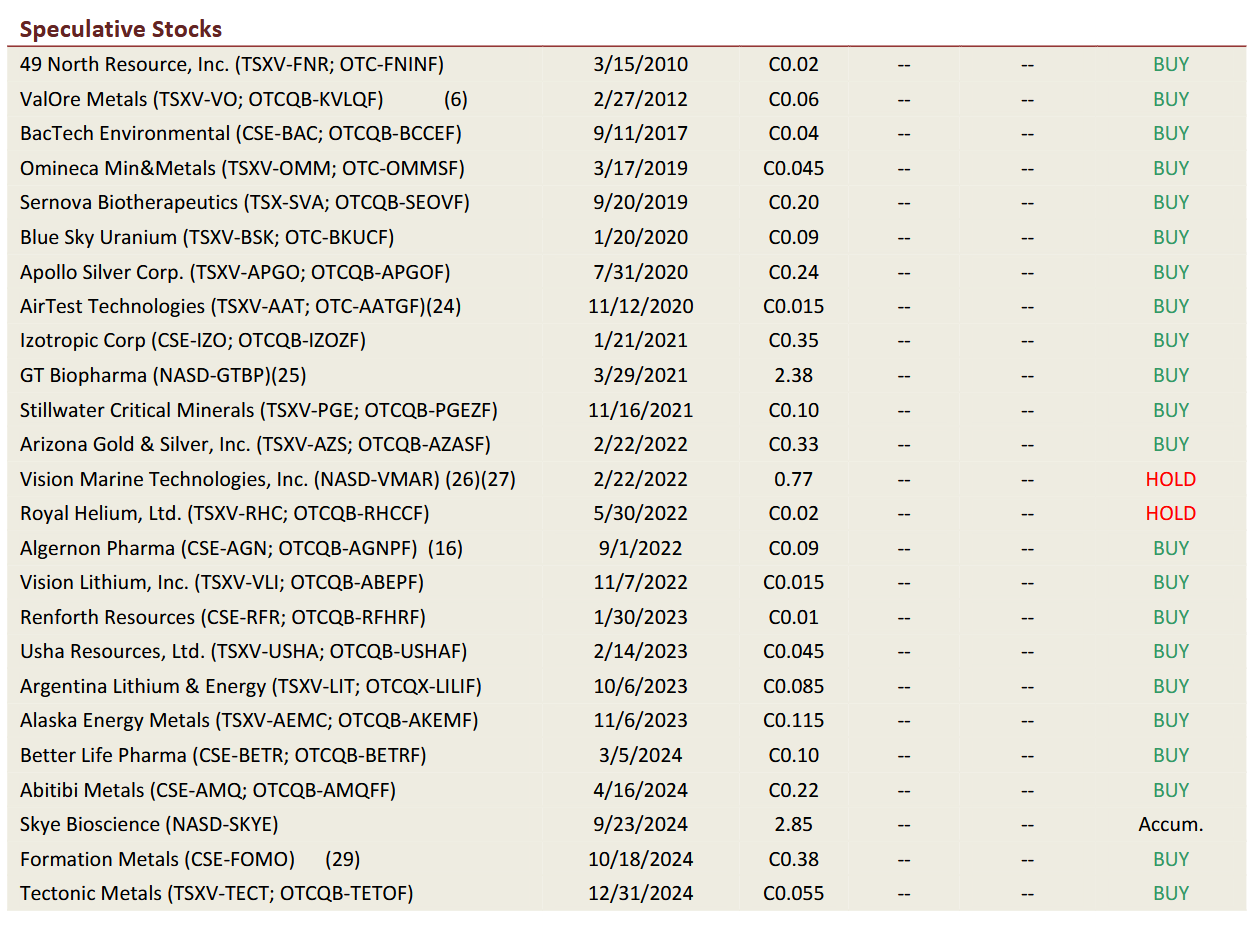

PORTFOLIO ALLOCATIONS

INDIVIDUAL INVESTMENT RECOMMENDATIONS

________________________________________________________________________________

1. Represents date of initial recommendation; does not reflect any subsequent status/weighting changes and trading.

2. Prices/other info. as of market close on Feb. 28, 2025; pricing information in U.S. currency unless otherwise noted.

3. P/E stats are typically represented as Price/FFO for REITs and other covered companies using that measure

4. In the case of inverse ETFs, yield quoted is on a trailing 12-month basis and does not necessarily reflect current expected yields

6. The former Kivalliq Energy. Price reflects 1-for-10 consolidation effective 6/28/18

15. Formerly Uranium Participation Corp.; commenced trading July 19, 2021 at a 1-for-2 consolidation v. Uranium Participation Corp.

16. Share price reflects 4—for—1 split for AGN effective 3/3/23

22. Price reflects a 1—for—28.6 shares consolidation effective 10/12/2023

24. Price reflects a 1-for-5 shares consolidation effective Feb. 1, 2024

25. Price reflects a 1-for-30 shares consolidation effective Feb. 5, 2024

26. Price reflects a 1 – for – 15 consolidation effective Aug. 22, 2024

27. Price reflects a further 1-for-9 share consolidation effective Oct. 8, 2024

28. Price reflects a 1-for-5 shares consolidation effective Nov. 7, 2024

29. Formation was spun out of Usha Resources on 10/18/2024; each USHA shareholder received one share of FOMO for every 5 USHA shares.

Explanatory Notes: The purchase dates given for each of the stocks recommended above is the date on which a Member receives an actionable instruction to buy/accumulate. Typically, the purchase (and, where appropriate, recommended sell) date is determined as falling on the same day said recommendations are given via the e-mail updates or, in the alternative, the regular newsletter upon its delivery to Members. In addition, we determine these dates based on any specific instructions given subscribers, such as target prices for buying/selling, stop loss orders, etc.

Definitions: Categories of stocks are compiled above based on our assessment of a variety of factors. Those individual stocks labeled “Income/Growth Stocks” are deemed the most conservative, as well as providing current returns via dividend income. “Growth” and “Speculative” stocks are so labeled based on our assessment of current health of the underlying company, business prospects and more, with those classified as “speculative” generally carrying the higher relative risk. Subscribers are encouraged to regularly read updates given by the Editor on these companies to help in determining the proper portfolio exposure to these stocks, and are reminded to invest based on the Editor’s overall asset allocation recommendations as well.

Status: Recommended stocks and ETF’s are rated as “Buy,” “Accumulate,” or “Hold” based on the Editor’s current assessment of each based on valuation, changing business prospects and other factors. Stocks rated a “Buy” should be purchased at currently published or even higher prices. Stocks rated an “Accumulate” should be purchased at current or, preferably, lower prices, on any short-term weakness. Stocks rated a “Hold” should be retained, but no new purchases are recommended. Changes from the last published list are in bold print above as a reminder, as are new recommendations.

____________________________________________________________________________________________________

The National Investor is published and is e-mailed to subscribers from chris@nationalinvestor.com. The Editor/Publisher, Christopher L. Temple may be personally addressed at this address, or at our physical address, which is — National Investor Publishing, P.O. Box 1257, Saint Augustine, FL 32085. The Internet web site can be accessed at https://nationalinvestor.com/ . Subscription Rates: Go to https:/www.nationalinvestor.com/subscribe-renew/ for Membership options for all our content/recommendations. Trial Rate: $75 for a one-time, 3-month full-service trial. Current sample may be obtained upon request (for first-time inquirers ONLY.)

The information contained herein is conscientiously compiled and is correct and accurate to the best of the Editor’s knowledge. Commentary, opinion, suggestions and recommendations are of a general nature that are collectively deemed to be of potential interest and value to readers/investors. Opinions that are expressed herein are subject to change without notice, though our best efforts will be made to convey such changed opinions to then-current paid subscribers. We take due care to properly represent and to transcribe accurately any quotes, attributions or comments of others. No opinions or recommendations can be guaranteed. The Editor may have positions in some securities discussed. Subscribers are encouraged to investigate any situation or recommendation further before investing. The Editor receives no undisclosed kickbacks, fees, commissions, gratuities, honoraria or other emoluments from any companies, brokers or vendors discussed herein in exchange for his recommendation of them. All rights reserved. Copying or redistributing this proprietary information by any means without prior written permission is prohibited.

No Offers being made to sell securities: within the above context, we, in part, make suggestions to readers/investors regarding markets, sectors, stocks and other financial investments. These are to be deemed informational in purpose. None of the content of this newsletter is to be considered as an offer to sell or a solicitation of an offer to buy any security. Readers/investors should be aware that the securities, investments and/or strategies mentioned herein, if any, contain varying degrees of risk for loss of principal. Investors are advised to seek the counsel of a competent financial adviser or other professional for utilizing these or any other investment strategies or purchasing or selling any securities mentioned. Chris Temple is not registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. He is also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

Notice regarding forward-looking statements: certain statements and commentary in this publication may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 or other applicable laws in the U.S. or Canada. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of a particular company or industry to be materially different from what may be suggested herein. We caution readers/investors that any forward-looking statements made herein are not guarantees of any future performance, and that actual results may differ materially from those in forward-looking statements made herein.

Copyright issues or unintentional/inadvertent infringement: In compiling information for this publication the Editor regularly uses, quotes or mentions research, graphics content or other material of others, whether supplied directly or indirectly. Additionally he makes use of the vast amount of such information available on the Internet or in the public domain. Proper care is exercised to not improperly use information protected by copyright, to use information without prior permission, to use information or work intended for a specific audience or to use others’ information or work of a proprietary nature that was not intended to be already publicly disseminated. If you believe that your work has been used or copied in such a manner as to represent a copyright infringement, please notify the Editor at the contact information above so that the situation can be promptly addressed and resolved.

The post The Bond Markets Weak Links – When Will Things Break? appeared first on The National Investor.