Table of Contents Show

Stock image.

For my entire decades-long career in capital markets, I’ve made the case that gold is not just a shiny relic of the past, but a serious, strategic asset for modern investors. After years of pounding the table, it feels pretty good to say that the world’s central banks—and now the US banking system—are finally catching up.

As of July 1, 2025, gold will officially be classified as a Tier 1, high-quality liquid asset (HQLA) under the Basel III banking regulations. That means US banks can count physical gold, at 100% of its market value, toward their core capital reserves. No longer will it be marked down by 50% as a “Tier 3” asset, as it was under the old rules.

This is a seismic shift in how regulators perceive gold, and it’s a long-overdue recognition of what many of us have known for decades: Gold is money. And it’s the kind of money you want to own when the world is on fire.

Central banks know that gold is real money. Shouldn’t you?

Obviously, I’m not the only one who believes this. Central banks have been leading the charge for 15 years. In the first quarter, central banks added 244 metric tons of gold to their official reserves, according to the World Gold Council (WGC). That’s 24% above the five-year quarterly average.

This isn’t a one-off anomaly. It’s part of a longer-term trend that began in earnest after the 2008 financial crisis and accelerated after gold’s reclassification under Basel III in 2019. According to the WGC, about 30% of central banks say they plan to increase their gold holdings in the next 12 months—the highest level ever recorded in their survey.

Why are central banks buying gold? The same reason you or I would: to protect against currency debasement, geopolitical turmoil and runaway debt. As global fiat currencies get printed with increasing abandon, I believe the yellow metal remains one of the few truly finite, unprintable stores of value.

So, if the world’s central banks are moving into gold, shouldn’t retail investors be doing the same?

The retail reawakening

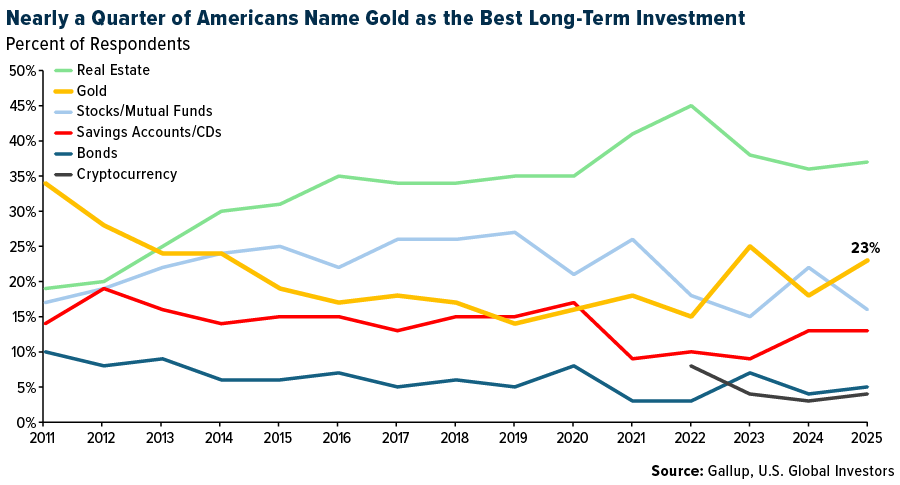

The answer, thankfully, is yes. According to Gallup’s latest polling data, nearly a quarter of US adults now say gold is the best long-term investment—a sharp increase from last year, and well above the 16% who say stocks. Only real estate ranked higher.

This could be significant. For the first time in over a decade, Americans say they’re prioritizing gold over equities. Investors appear to be increasingly skeptical of the stock market’s near-term trajectory, and they’re returning to what has historically worked in times of uncertainty.

I’ve said for years that gold belongs in every diversified portfolio. Back in 2020, I told CNBC that I believed gold could hit $4,000 an ounce on looser monetary policy and central bank balance sheet expansion. Fast forward to today, and the metal is trading at $3,340.

Today I’d like to adjust my forecast.

With the implementation of President Donald Trump’s tariffs, continued global uncertainty and rising central bank gold demand, I now believe gold could go as high as $6,000 an ounce over the medium- to long-term.

The curious case of gold miners

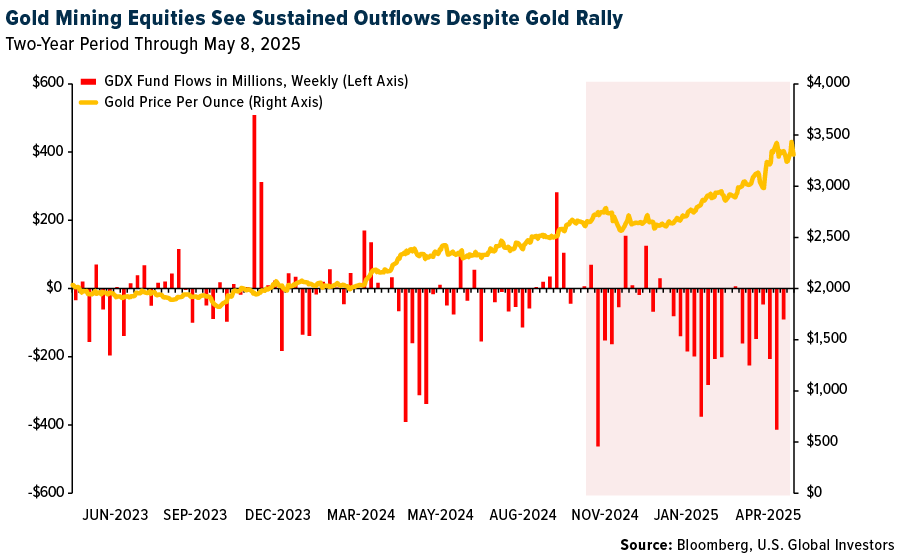

But here’s where things get interesting—and puzzling. While gold prices continue to make new all-time highs, gold mining stocks have been seeing sustained outflows.

The VanEck Vectors Gold Miners ETF (GDX), which tracks many of the world’s largest publicly traded gold producers, has been bleeding capital for months. Even as gold prices surge, weekly fund flows have been negative, with investors pulling billions out of mining equities.

This disconnect is hard to ignore. It points to a deeper concern investors may have about the operational and financial health of mining companies. Unlike physical gold, which simply tracks the spot price, miners are exposed to cost inflation, labor shortages, geopolitical risk and more. These headwinds aren’t new, though, and they shouldn’t obscure the fundamental leverage that quality mining stocks offer in a rising gold environment.

Historically, gold stocks tend to lag the metal itself until higher prices are deemed sustainable.

Institutional capital tends to wait for the “all clear” sign. That often means retail investors can front-run the rotation. If gold prices stay elevated—or go higher, as I expect—I believe we’ll see renewed flows into the mining space.

Meanwhile, we’ve seen investors increasingly favor physically backed gold ETFs and streaming/royalty companies as lower-risk ways to gain exposure. That’s understandable. These vehicles offer gold’s upside with fewer operational headaches.

But let’s not forget that miners still dig the stuff out of the ground. When margins improve, they can offer significant torque.

Be the bank

Basel III is more than a regulatory change. I believe it’s a validation. It affirms what many of us have long believed about gold’s status as a monetary asset and a hedge against chaos.

If the world’s most powerful financial institutions are increasing their gold exposure, and regulatory bodies are reclassifying it as a top-tier liquid asset, what’s holding the average investor back?

As always, I recommend a 10% weighting in gold, with 5% in physical gold (bars, coins, jewelry) and 5% in high-quality gold mining stocks, mutual funds and/or ETFs. Remember to rebalance on a regular basis.

(By Frank Holmes, CEO of U.S. Global Investors)