Stock image.

The risk premium for options is rising in assets from stocks to gold, even as implied volatility on benchmark indexes has been either steady or falling for most of this year.

While that may seem counterintuitive, it’s in large part because the actual market swings have been so lackluster. That’s boosting the risk premium, or difference between how much traders expect a market to move and how much it has moved.

The narrow ranges — and rising risk premium — can be pinned on different factors depending on the market. Rate-cut expectations are driving gold, supply and demand outlooks are hemming in oil and uncertainty around the Federal Reserve, corporate earnings and retail flows are affecting stocks.

In equities, options volume hit a record in September, and expectations of market moves have increased somewhat as investors start to add hedges around year-end. But there’s only so much traders will pay up for options if realized swings remain constrained.

“Fixed-strike volatility has actually increased quite a bit in the past few weeks, and implied volatility is elevated relative to realized volatility metrics,” said Robby Knopp, co-head of the S&P options desk at Optiver in Chicago.

Low correlation has kept a lid on S&P 500 Index volatility, as individual equities moving at different speeds in different directions cancel each other out. As a result, the VIX has stayed muted even as single stock volatility jumps with the earnings season looming. The difference between the VIX Constituent Volatility Index and the Cboe Volatility Index last week was the biggest since the end of January, and it’s near the top of the range over the past two years.

“The spread between single-stock vol and index vol has widened amid low SPX-implied correlation and high dispersion,” Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence, wrote in a note last week.

The poster child for limited movement may be oil, which has been stuck in a range for the past few months. An outlook for a glut has been balanced by attacks on Russian refineries and export facilities, which may curb some near-term supply.

That’s kept a lid both on volatility and skew, as geopolitical flareups have been quickly resolved, offering if anything an incentive to sell into the short-lived spikes in call volatility.

The United States Oil Fund’s spread between one-month implied and realized volatility is in the 77th percentile over the past year, according to data compiled by Bloomberg.

“Day to day, it does appear to be vacillating a lot, but if you take 10 steps back, it’s vacillating in a very strict range,” said Samantha Hartke, Americas head of market analysis at Vortexa. “There is really no incentive to commit to a significant position in the crude market at this point.”

How much of the oil currently in tankers “is absorbed into storage versus consumed for prompt demand could well be the next tipping point,” she added.

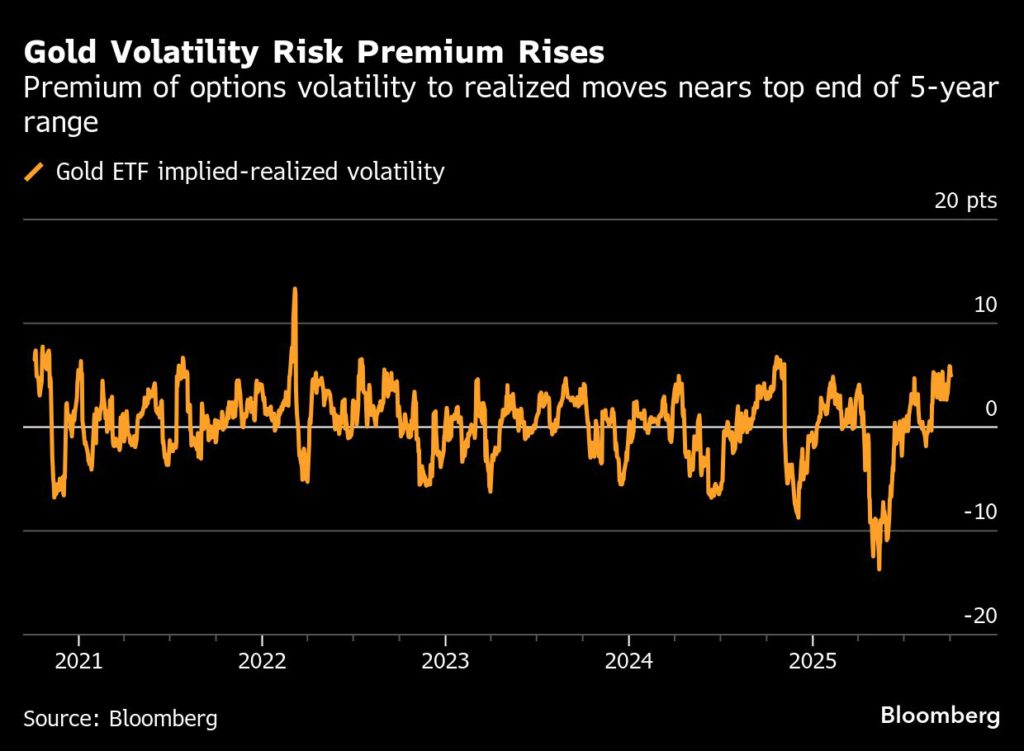

While in some other markets the drop in realized volatility has been the driver, gold is an outlier. Implied volatility has been climbing over the past month as bullion surged to record after record, with the US government shutdown adding another layer of uncertainty for investors. That’s pushed option risk premium to the high end of the range over the past five years.

Risk premiums have increased since early September as a function of gold breaking fresh records, dealers charging more to offset greater delta-hedging costs and increased investor demand for bullish tail options after the FOMC meeting, according to Aakash Doshi, global head of gold and metals strategy at State Street Investment Management.

“Gold vol risk premiums have not been this rich since the early days of the Russia/Ukraine war in 2022,” said Doshi. “During aggressive price spikes, options premiums can really soar due to investor FOMO.”

That could change if the rally tops out, with $4,000 an ounce in sight, and gold stabilizes like other markets.

“As the market steadies between $3,800-4,000/oz and price vol realizes low levels, premiums will likely come off after the violent swings in September,” Doshi said.

(By David Marino and Yvonne Yue Li)