Scoop up some mining stocks. Stock image

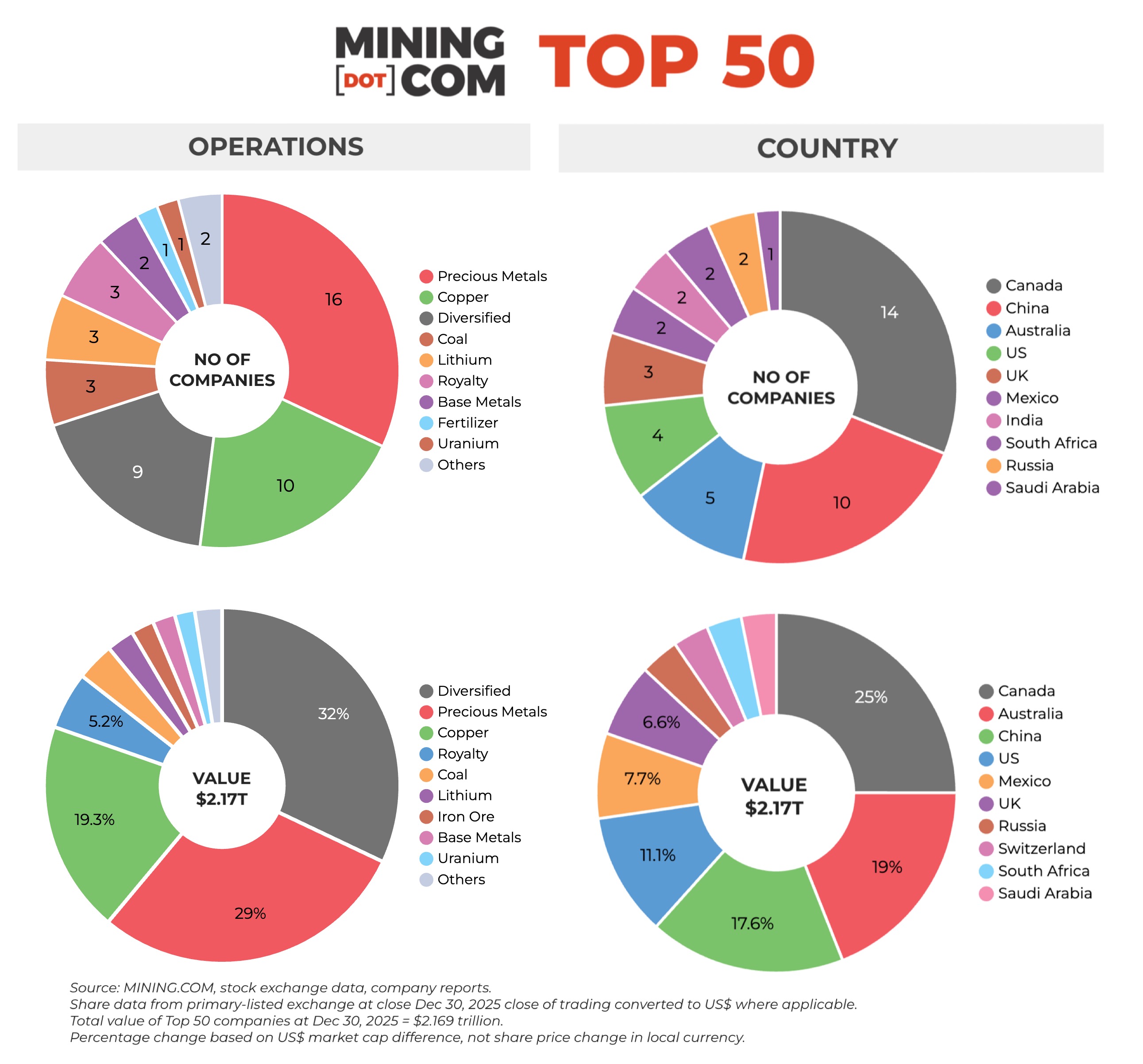

At the end of the fourth quarter the MINING.COM TOP 50* ranking of the world’s most valuable miners had a combined market capitalization of $2.17 trillion, up an astonishing $892 billion in 2025.

Most of the gains accumulated in the second half and after three years of stagnation, the market valuation of mining and metals appears to have finally caught up with other sectors. The building blocks of the global industrial economy are finally seen for what they are: critical.

From lip service (not even), Western governments (the US in particular) are now putting money behind mining, catching up to a competitive strategy China has successfully employed since the turn of the century.

The ranking is based on a company’s market capitalization in local currency on its primary exchange and then converted to USD so the near-double digit decline in the greenback this year gave some support to stock and commodities prices. But a rerating of the industry has been long overdue.

Most of the credit for the 70% jump in the value of the Top 50 can go to rampant precious metals prices and copper, but gains have been broad-based and even old-economy iron ore and much reviled lithium joined the party, albeit late.

The best performing list shines with gold and silver counters including a five-fold increase for Fresnillo, the London-listed silver miner controlled by Mexico’s Peñoles, which has now cemented its position halfway up the ranking after dropping in and out for years.

The stiff competition to make the list this year is evidenced by the fate of Coeur Mining. After entering the Top 50 for the first time at the end of September, a middling performance in Q4 saw the Chicago-based silver and gold miner fall out of the ranking despite more than tripling in value over the course of 2025.

Apart from all things precious and base, rare earth was the standout story of 2025. Perth’s Lynas Rare Earth squeaked in at no 49 after at the end of Q3 to join Las Vegas-based MP Materials which rocketed up the charts in the first half after a groundbreaking deal with the Pentagon.

MP Materials still show gains north of 200% for the year and Lynas has doubled, but that was not enough and now both counters have fallen out of the ranking again, leaving only China Northern Rare Earth to represent the 17 elements as it has for years.

Taking the place of the rare earth stocks are the world’s two largest lithium producers. A boost to the price of the battery metal in the second as oversupply began to ease, saw Chile’s SQM and US producer Albemarle return to the Top 50, bringing the number of lithium miners back to three.

The sector peaked in 2022 with six stocks in the ranking and Tanqi Lithium ranked 58th at the moment may well join its Chinese counterpart Ganfeng if the lithium uptrend continues, but Australian producers like Minerals Resources and Pilbara Minerals (now PLS Group) may have a harder time of it.

Since inception, the MINING.COM TOP 50 was headed by two firms – BHP and Rio Tinto – the only miners with consistent market capitalizations above $100 billion (with a wobble here and there). Now there are five firms with the distinction.

With a string of acquisitions behind it, Chinese champion Zijin Mining, worth $124 billion after a 127% appreciation only just pipped Southern Copper, which has also embarked on an aggressive expansion strategy, for third, up 64% to $119 billion.

Southern Copper, the NYSE-listed mining arm of Grupo Mexico, was joined by Newmont in the triple digit club last quarter but unlike its acquisitive peers, shortly after swallowing Australia’s Newcrest Mining for $17 billion, Denver-based Newmont embarked on a multi-billion dollar divestiture program.

Agnico Eagle and Kirkland Lake Gold combined in 2022 and the Toronto-based group continues to bolt on assets, making it a candidate for the $100 billion mark should gold continue its gravity defying rally. Agnico has doubled in value this year and is worth $86.3 billion.

Anglo and Teck Resources could yet turn out to be the biggest mining deal of the decade now that Ottawa has blessed the combination, thanks in no small part to Anglo’s commitment to move its London headquarters to Vancouver.

But scaling the $100 billion level may prove elusive. Despite double digit gains, both Teck and Anglo made the year’s worst performer list – just another indication what a wild ride 2025 has been.

Anglo-Teck would hardly crack the top 10 with a combined value of a shade under $68 billion, but will place it ahead of Swiss miner and commodities trader Glencore, which once again underperformed in 2025.

That would add insult to injury for Baar, which tried and failed to acquire Teck a couple of years ago and is still trading, nearly 15 years later, below its 2011 IPO price.

NOTES:

Source: MINING.COM, stock exchange data, company reports. Share data from primary-listed exchange on December 30, 2025 close of trading converted to US$ where applicable. Percentage change based on US$ market cap difference, not share price change in local currency.

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining (the gold and uranium giant may list later this year), Eurochem, a major potash firm, and a number of entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry, and how far upstream is the bulk of its revenue, before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or even warrant a seat on the board? This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialised financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy or Bayan Resources where power, ports and railways make up a large portion of revenues pose a problem. The revenue mix also tends to change alongside volatile coal prices. Same goes for battery makers like China’s CATL which is increasingly moving upstream, but where mining will continue to represent a small portion of its valuation.

Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat (now Valterra) to track PGM representation in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly, we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta.

With other groups like Mexico’s Penoles where refining and chemicals make up a substantial part of the business where possible the Top 50 would include separately listed operating subsidiaries that are dedicated to mining. This is also why Southern Copper represents Grupo Mexico in the ranking.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology: email Frik Els at [email protected] with Top 50 in the subject line.