Silver Crown Royalties has had a great six month performance, up over 300% from way oversold levels, handily outperformed the silver (“Ag“) price. Why such a strong showing? As mentioned in prior articles & CEO interviews, a tipping point has been passed.

When Silver Crown’s shares were under C$7, (now ~C$25), investors feared it lacked critical mass. The Company was stuck in a chicken or egg situation.

Most precious metal royalty/streaming companies start out quite small and are very high risk due to constraints on capital and trust in management to; 1) see meaningful deal flow, 2) choose good projects, and 3) fund transactions without onerous debt and/or equity.

On January 13th, I believe the tipping point arrived as well-known & respected strategic investor & junior mining advisor Michael Gentile invested in the Company. Gentile is well-connected with institutional & high net worth investors.

Mr. Gentile is the largest shareholder in over 25 juniors, sits on several company boards, and is a valued strategic advisor. In 2021 he co-founded Bastion Asset Management, a Montreal-based hedge fund managing over C$750M.

The PPX Mining royalty becoming a valuable paying asset pushed Silver Crown even further over the top. At an assumed US$80/oz Ag over the next several years, the IRR on PPX would be over +100%. When PPX was signed, the Ag price was < $31/oz.

Minimum deliveries (the cash equivalent of) 14,062.5 ounces of Ag/qtr. commenced this quarter. At the front-month Ag price of $78/oz, this single royalty alone equates to ~C$6M/yr. in cash flow

PPX runs through early-2030. As a reminder, SCRI holds a 15% royalty on PPX’s Igor 4 project in Peru. This flagship asset truly shows what management can do. CEO Peter Bures has up to 20 deals like this under careful review at any given time.

Without overstating the importance of positive cash flow and a growing cash balance (now ~C$15M + ~C$23M worth of warrants if exercised), let me briefly reiterate how much it helps the Company.

First, counterparties are much more willing to sign deals, happy to take shares and/or cash, having seen how well the shares are performing. Second, management has the luxury of picking and choosing only the very best projects/mines to back.

Third, due to reasons 1 & 2, management can lock up attractive transaction economics. CEO Bures repeatedly states in interviews that 20%-25%+ IRRs continue to be sought.

This is a very strong investment hurdle. The fact that his team has so much deal flow is telling. To be honest, I thought when the Ag price soared last year, deal flow might vanish…

The opposite happened, deal flow is excellent, proving there are not many companies doing what Silver Crown is. This is why famed junior mining investor Michael Gentile is invested (his first-ever royalty company).

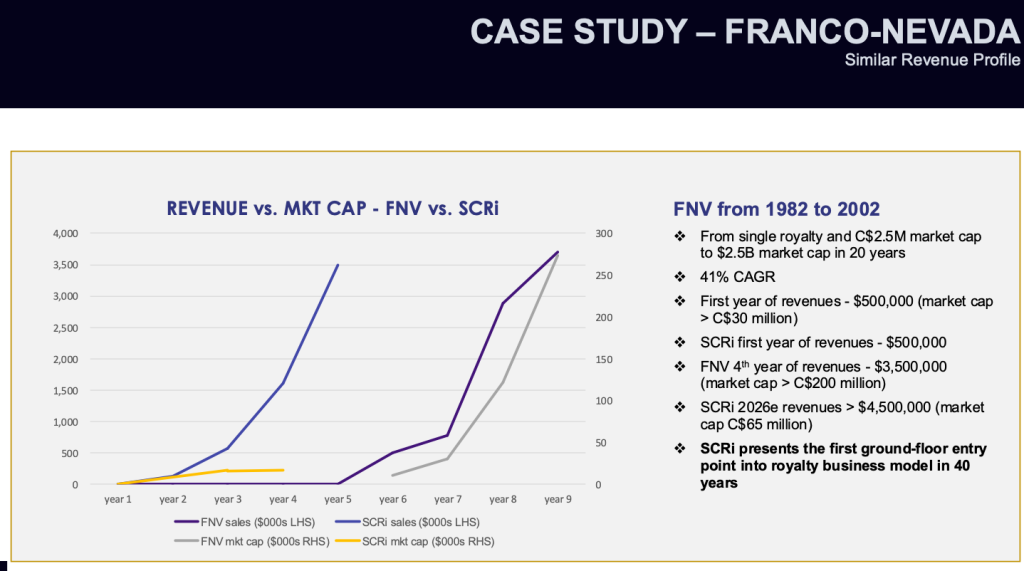

Mr. Gentile recently called Silver Crown a top-10 holding, and one he might NEVER sell. He added that the Company could become a “mini Franco-Nevada,” and pointing out that Franco’s cost of capital is just 5-7%.

Silver Crown’s cost of capital is at least double that, but is falling as it de-risks the business model by growing sustainable cash flow and diversifying the number and range of royalties by project stage & jurisdiction.

As an aside, trading liquidity is picking up, now averaging ~35k shares/day in Canada + the U.S., equal to ~1.75M shares/day of a C$0.50 junior miner.

Signing deals with excellent economics, and having crossed definitively into positive operating cash flow, gives the team breathing room to be highly selective going forward.

Notably, Bures has always said there will be setbacks along with winners like PPX. It has not been smooth sailing for three other transactions. The team has prudently taken write-downs.

Written down assets still have residual value. If they come back into compliance, they can still work out, especially if the Ag price were to be higher when the ounces start flowing.

One write-down is a non-cash impairment of C$940K on its Gold Mountain royalty, due to a 3-yr pause in cash inflows as the new operator optimizes its operations.

Importantly, there’s drop dead date on Silver Crown’s royalties. The royalty is on the asset not the operator and lasts for life of mine (subject to cumulative production caps).

An impairment was also taken on the BacTech royalty (a bio-leaching project in Ecuador), as BacTech failed to make significant progress on financing & development milestones. And an impairment on the Pilar Gold royalty due to repeated delays in central Brazil.

With commodity prices strong, the chances of Gold Mountain, BacTech & Pilar regaining their footing is not insignificant, timing unknown. Having said that, these deals will be far less important as larger ones are announced.

Said another way, it will become harder and harder for Silver Crown’s existing and future portfolio companies to disappoint if precious & base metals remain strong or climb higher! Remember, ~75% of the time Ag is a by-product, not the primary mined metal.

The above metal price gains are really important. Many analysts, consultants, pundits believe these metals are headed higher. I agree. Not necessarily in the coming weeks/months, but over the medium-to-longer term.

Given the Middle East crisis, global inflation will be higher than expected, perhaps a lot higher. That’s bad for most companies. By contrast, Silver Crown’s royalties are not impacted by portfolio company production costs, but benefit 100% from a higher Ag price.

Silver Crown is attractively valued and has under 8M fully-diluted shares outstanding. That’s unheard of for Canadian & Australian junior miners. It trades at a modest discount to peers on an Enterprise Value to 2027e revenue basis.

However, if one agrees that the Company’s revenue & cash flow growth will be greater than peers for (at least) several years, then today’s valuation could offer an attractive entry point.

That’s why Mr. Gentile says he might NEVER sell Silver Crown, because it’s like a mini-Franco Nevada. It’s quite possible, albeit far from a sure thing, that attributable Ag ounces paid to the Company (in cash, not Ag) could double each year from 2024 through the late-2020s.

That’s the potential upside… Not just rapid growth prospects, but also the meaningful de-risking that has occurred, and will continue, upon the announcements of new royalties.

I recognize it’s aggressive to compare tiny Silver Crown to giants like Franco-Nevada, Wheaton Precious Metals, Royal Gold, or mid-tiers Triple Flag Precious Metals, and Osisko Gold Royalties, but readers should note these companies all started out small like Silver Crown.

They all had high costs of capital until they reached tipping points, upon which cost of capital declined all the way to the current 5%-7%. All had spectacular growth in revenue, cash flow & share price in their early years.

What’s different for Silver Crown? 2025-26 is a more bullish Ag price environment than the gold price gains that launched other royalty companies higher.

Also, a proven, arguably superior business model (less competition for Ag-only royalties, specializing in royalties only, minimum payment clauses, staged milestone-based investments, ability to deploy equity, cash and/or debt).

Unless the Ag price collapses, the downside for Silver Crown seems fairly limited. I asked ChatGPT about that, see below. Quote, “…royalty/streaming companies rarely fail outright, they overwhelmingly get acquired or consolidated into larger platforms.”

If downside risk is limited (my opinion, shared by CEO Bures & Mr. Gentile, but no guarantees), and capital gain potential is substantial, Silver Crown Royalties offers a compelling risk/reward proposition at current Ag prices, with FREE added torque upon higher Ag.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about Silver Crown Royalties, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Silver Crown Royalties are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Silver Crown Royalties was an advertiser on [ER] and Peter Epstein owned shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.