The following article relies upon public information (press releases, sedar fillings, YouTube transcripts, corp. website & slide deck). The views, opinions, commentary, peer comparisons, etc. are entirely that of Epstein Research, not Frontier Lithium. Please see disclaimers/disclosures at bottom of page.

For nearly three years, from late 2022 to 2H 2025, the benchmark 6.0% spodumene concentrate (“SC“) price was falling or bumping along a bottom around $650-$850/t. During that nuclear winter, ALL lithium (“Li“) projects slowed to a crawl.

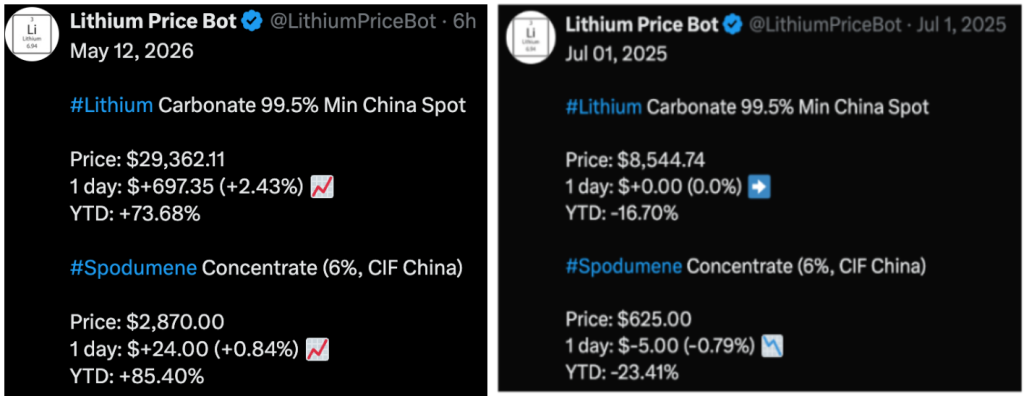

However, the pain is behind us. The sector-wide pushback of project timelines virtually ensures stronger SC pricing going forward. The recent SC6% price in China of US$2,870/t is a far cry from last Summer’s $625/t!

UBS is forecasting $4,250/t next year, but most analysts & consultants are closer to $1,500-$2,000/t. Some will (presumably) raise targets, which would be bullish for the sector.

To be clear, $2,870/t is already quite good, enough to get most projects into production. Over several years, juniors used $1,350 to $2,000/t long-term assumptions on SC6% (or SC6% equiv.) grade material in PEA/PFS/BFS reports.

A relatively advanced development-stage company (DFS delivered May-2025) I’ve been following is Frontier Lithium (TSX-v:FL) (OTC: LITOF), advancing its PAK Lithium Project in NW Ontario.

PAK consists of a Li mine & mill project, and a proposed conversion facility project in Thunder Bay, Ontario. Combined it would be a significant, vertically-integrated operation of 200,000 tonnes SC6%/yr, feeding an initial 20,000 tonnes Li carbonate equiv. (“LCE“)/yr.

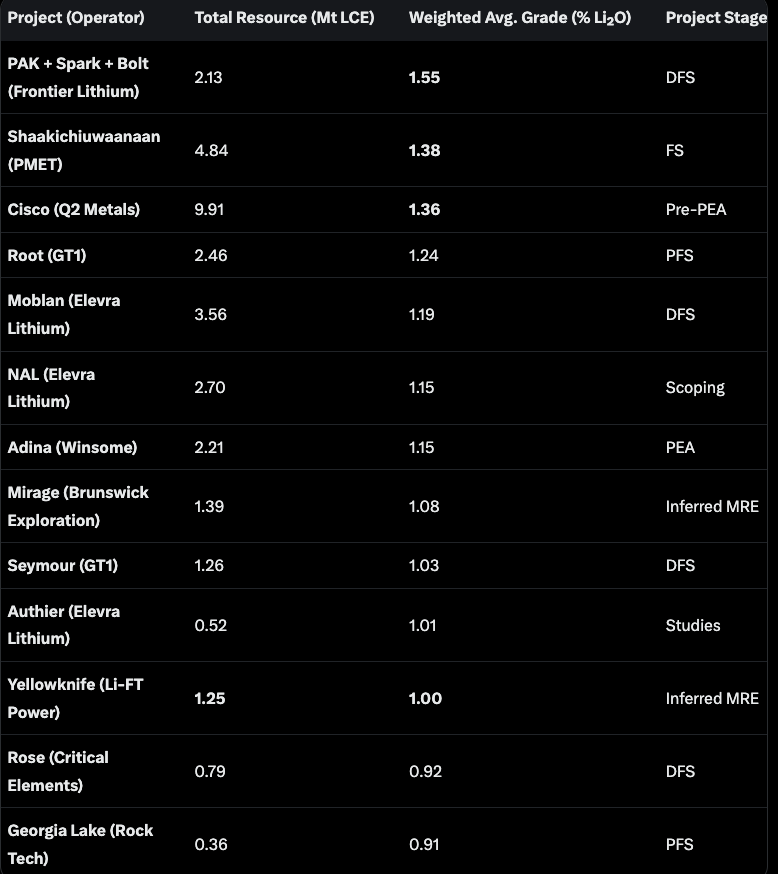

PAK has N. America’s highest-grade spodumene project (~2.1M tonnes LCE at 1.55 Li₂O, with very low deleterious materials). The DFS outlines a 31-year mine life. Economics at a base case US$1,475/tonne deliver a C$932M post-tax NPV(8%), and an IRR of 18%.

HIGHEST GRADE in CANADA, others avg. 1.12% Li₂O

At $2,870/t, (all else equal), a linear extrapolation of NPV/IRR would be C$3.0B/33%. This means Frontier is valued at just 4% of its PAK project NPV (at spot pricing, mine/mill only), very low compared to PMET Resources, valued at 16-17% of NPV($2,870/t).

That valuation differential is notable, and it gives Frontier zero credit for the conversion facility asset.

Granted, PMET has a monster project that’s still growing, three times the number of tonnes of LCE of PAK, yet it’s valued ~8x higher at C$1.3B vs. Frontier at C$156M (fully-diluted enterprise values).

There are very few advanced-stage Li projects in safe jurisdictions like Ontario. Especially ones backed by giants like Japan’s Mitsubishi Corp. (7.5% owner at project level), and Panasonic (a MOU with Mitsubishi for a significant, de-risking, off-take agreement for Li hydroxide).

Panasonic is a major Li-ion battery producer. The MOU sets the framework for a future definitive off-take agreement with competitive pricing. Panasonic is an excellent partner with U.S. EV battery production in their Kansas & Nevada factories for 73 GWh annually.

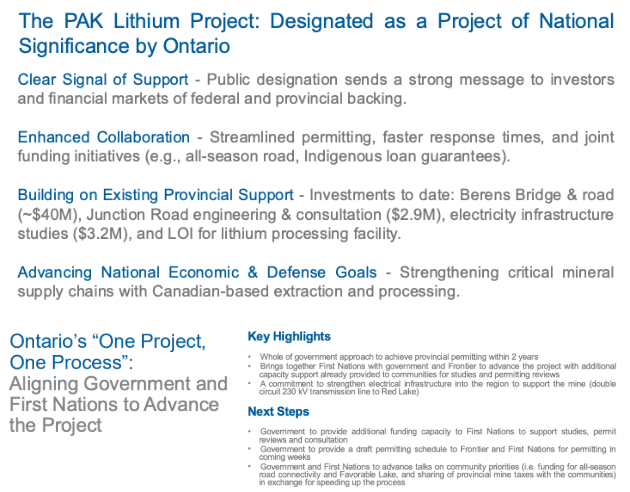

Mitsubishi’s 7.5% project-level stake includes the conversion facility. Earlier this year, Ontario and the Federal government pledged a combined C$240M to fund this critical project. Note, this article focuses on the nearer-term SC6% production story.

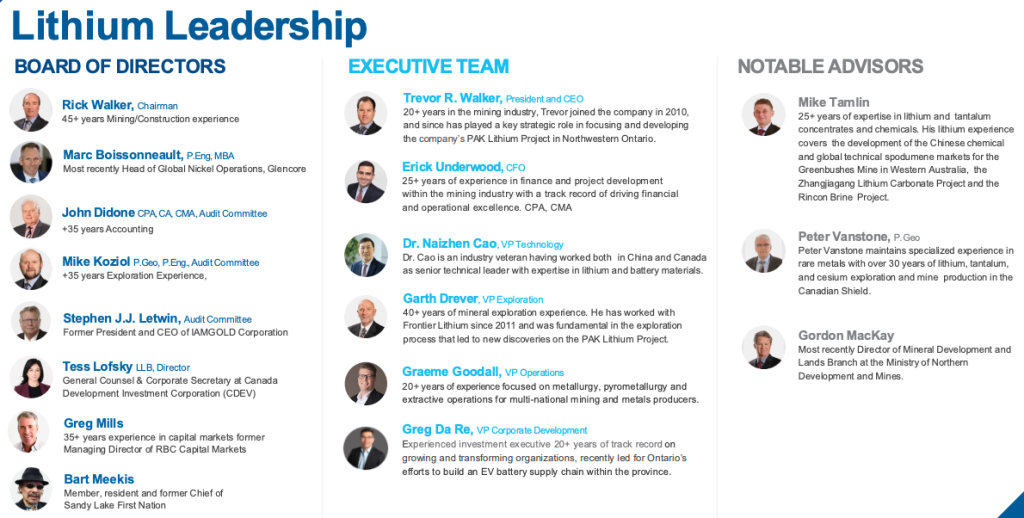

Frontier has established an Executive Advisory Council (“EAC“) to support its transition to execution readiness. The EAC will provide strategic, technical, financial, and industry guidance.

The initial members of the EAC are Bruce Turner, P.Eng., and Dr. David Deak, PhD. Turner brings extensive experience in large-scale open-pit mining and project development from BHP, Mitsubishi Materials, and other major operations.

Dr. Deak is a leader in the Li-to-EV value chain, with prior executive experience at Lithium Americas, Tesla, and other firms in battery materials, renewable energy, and critical minerals. PLEASE SEE Board & Mgmt. team members here…

As M&A picks up in the Li space like it has for gold, silver, copper, PMET could be acquired first, but there will be ample investment appetite for dozens more. In my view, Frontier has a top 5 or 6 Canadian hard rock project, and top 2 or 3 at BFS stage.

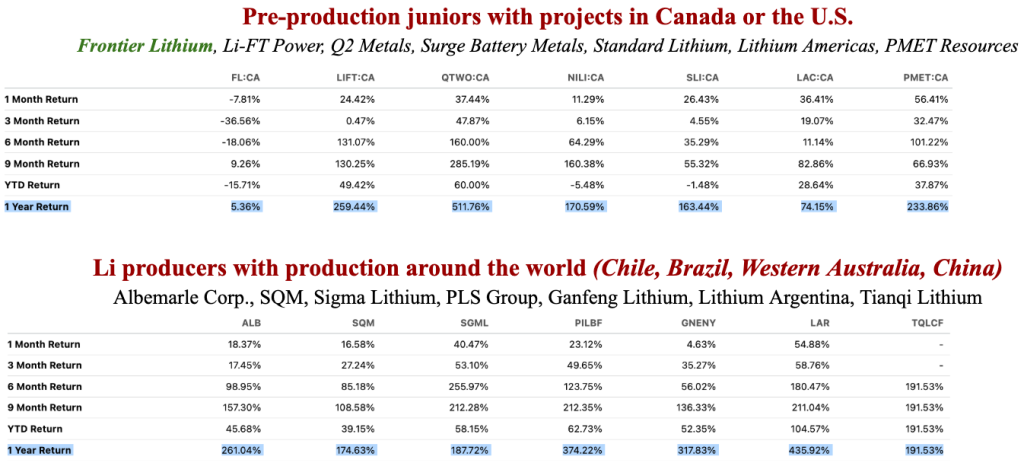

Given this bullish narrative for Li and for Frontier, why has the share price languished? In the above chart, notice that Frontier is up just 5% in the past year vs. these pre-production juniors +74% to +512%. Many producers are up 100s of percent as well.

I believe there are five primary concerns regarding the PAK project. First, time to initial production. Second, project remoteness (access to regional infrastructure).

Third, (overly ambitious?) plans for a downstream conversion facility in Thunder Bay, adding significant time, cost and distraction. Fourth, ongoing funding requirements, and fifth, will Mitsubishi increase its 7.5% stake to 25%, as it’s entitled to?

How many of these concerns are Company specific? Most Li projects in Quebec, like those owned by Q2 Metals (pre-PEA) & PMET, are remote, require significant additional support for infrastructure, are years from production, and need ongoing equity funding.

Quebec’s largest projects (Q2’s Cisco, PMET’s Shaakichiuwaanaan), are in the remote Eeyou Istchee James Bay region, 6–20 km off existing all-season highways, with rail access (~150 km to Matagami). From there, another 800+ km to St. Lawrence ports (e.g., Bécancour).

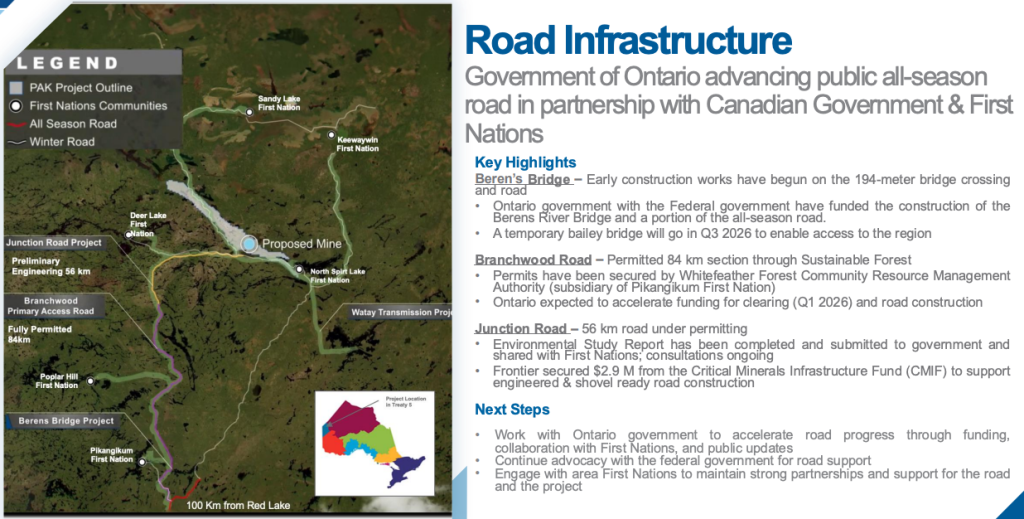

PAK is ~175 km north of Red Lake, Ontario via winter roads (all-season road + bridge meaningfully funded & under construction). PAK has shorter integrated logistics. SC will eventually go directly to its Thunder Bay conversion facility/port (~500 km in total).

It’s true the conversion facility carries substantial funding & execution risk, but it’s not the main focus at this time. More importantly, the Company receives zero value for it, despite my belief it’s worth north of C$100M.

The other company-specific risk is a concern that Mitsubishi might not move to a 25% project-level ownership from its current 7.5%.

Twenty six months ago Mitsubishi invested C$25M at an implied C$333M valuation, when the SC6% price was around $950/t. With SC6% now three times that, meaningful project advancements and government buy-in, Mitsubishi remains engaged.

Think about it, SC6% is 3x higher, yet Frontier’s enterprise value is just C$156M. If/when a top up to 25% is completed, probably after permitting in late 2027 or early 2028, that should bring in C$100s of millions, offsetting the need for major new share issuances.

Management is considering non-equity sources of funding until Mitsubishi’s cash lands. For instance, it could probably sell a 1.5% NSR for C$30-$70M. There’s serious interest from multiple parties in a royalty on PAK.

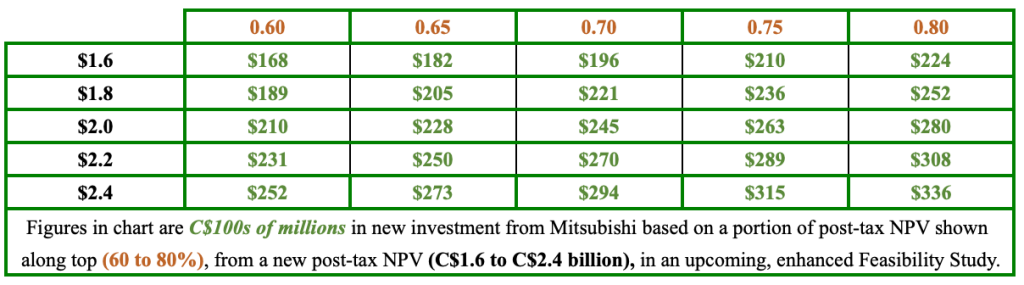

After topping up to 25%, Frontier will be on the hook for 75% of cap-ex. An incremental investment by Mitsubishi would be based on a fraction of a new post-tax NPV, see table above.

If the second tranche of (25.0% – 7.5% = 17.5%) is made at an implied 70% of a new C$2.0B NPV, that would be C$245M. Management hopes to deliver an enhanced Feasibility Study in 1Q/27 incorporating increased throughput scenarios and a shorter mine life.

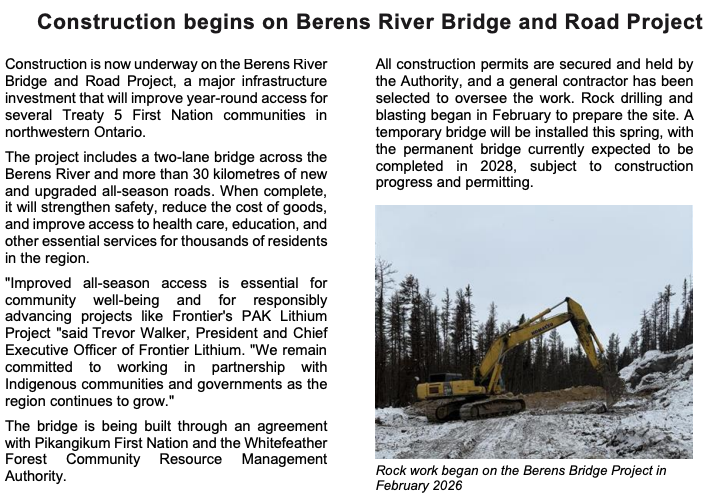

For years, investors have worried about the logistics around the critical need for all-season roads/bridges to support PAK. Who will pay? How many years to build? Recently, two things have changed things for the better.

The Trump Administration has lit a fire under Canadian natural resource & logistics projects, leading for example to Ontario’s 1 Project 1 Process initiative, expediting permitting to under 24 months.

Ontario and Ottawa committed nearly $80M toward the Berens River Bridge and all-season road linking six remote First Nations communities, and the PAK project.

Ottawa finalized up to $6.1M in non-repayable Critical Minerals Infrastructure Fund support for engineering & permitting of a 56 km access road, plus a transmission line connecting PAK to the power grid.

Second, stronger Li prices due to surging Battery Energy Storage System (“BESS“) demand.

While a bit of uncertainty remains on how much Frontier will have to pay, it will likely be no more than $10s of millions, spread over a few years. Ontario and the Feds are backing public infrastructure for First Nations, they will fund the lion’s share.

Ontario selected PAK as one of the first projects under One Project, One Process. Readers are encouraged to review the images in this article focusing on regional infrastructure.

They convey the latest info as of April. Long-term shareholders might not notice yet, but things are moving in the right direction, not just SC6% prices. Readers are encouraged to take a closer look at Frontier Lithium (TSX-v: FL) / (OTC: LITOF).

Like for all Li juniors globally, the past three years (until about six months ago) were rough, but many have soared in value while Frontier has not. That could change at any time.

Make no mistake, Frontier is a high-risk proposition, but in my view no more risky than most other top Li plays at similar development stage, (Frontier backed by Mitsubishi Corp. & Panasonic), and less risky than earlier-stage projects or juniors in less favorable jurisdictions.

Disclaimers/Disclosures:

Epstein Research [ER] has written a few articles on Frontier Lithium, but none in the past 18 months until now. Peter Epstein and [ER] have no prior business relationship with Frontier or its management team/board, but is actively pursing a paid mandate that could begin very soon. Readers should assume that Mr. Epstein is biased in favor of Frontier Lithium.

Mr. Epstein does not currently own shares of Frontier Lithium, but has in the past, and may acquire some in the open market in the near future. The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Frontier Lithium, including but not limited to, commentary, opinions, views, assumptions, facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities.

[ER] is not directly employed by any company, group, organization, party, or person. The shares of Frontier Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of funds. It is assumed and agreed upon by readers that they will consult with their own financial advisors before making investment decisions.