Despite serious doom & gloom, silver (“Ag“) is up +123% in the past year. However, the near-month futures contract is down ~38% from ~US$122/oz in late January. To say that Ag has been volatile would be an understatement.

Post the U.S./Israeli attack on Iran on Feb. 28th, precious metals initially jumped on safe-haven demand, but then fell due to a stronger US$ and the selling of the most liquid assets first to raise dry powder.

Some precious metal bulls are surprised and disappointed that gold (“Au“) & Ag have sold off. However, the vast majority of financial institutions and precious metal pundits remain bullish over the medium-to-longer term.

Ag in particular looks strong as substitution is not realistic for the most critical high-tech & military applications where Ag’s superior electrical/thermal conductivity, strong resistance to oxidation, and unmatched optical reflectivity reign supreme.

Recycling is on the rise, but not fast enough to plug the mined Ag deficit. Only sustained, elevated, Ag prices can resolve ongoing shortfalls.

When one bets on a junior miner, primary risk factors include; jurisdiction, management team, and prospective mine logistics. Investors don’t want to nail the theme (higher precious metal prices), only to be derailed by a company-specific factor.

Development risks can’t be avoided, but some projects are riskier than others. In looking at the Top-10 Ag producing countries, 40% (China, Bolivia, Russia & Kazakhstan) are places with very elevated risk profiles, especially for Western countries to rely on.

World-class primary Ag projects are rare and keenly sought after. High-grade? Even better. Almost every Tier-1 Ag-heavy project is in S. America or Mexico. Investors can easily become overexposed to those jurisdictions.

In my view, the best places to be developing projects in 2026 are the U.S. and Canada. The U.S. is especially attractive given tariff uncertainties and a wide range of newly enacted financial incentives (tax breaks, free-money grants, low-cost loans, etc.).

A primary Ag junior I continue to love is Blackrock Silver (TSX-v: BRC) (OTCQX: BKRRF). Its flagship project is in Nevada, USA, one of the world’s Top 2 or 3 mining jurisdictions. Nevada is known as the “Silver State” for a reason.

The nickname dates to the mid-19th century, following the discovery of the massive Comstock Lode — one of the richest Ag deposits ever found. Blackrock’s Tonopah West project sits in the historic Tonopah Silver District, part of the larger Walker Lane Trend.

This District is one of N. America’s most significant Ag camps, having produced ~174 million oz of very high grade Ag primarily between 1900 & 1930.

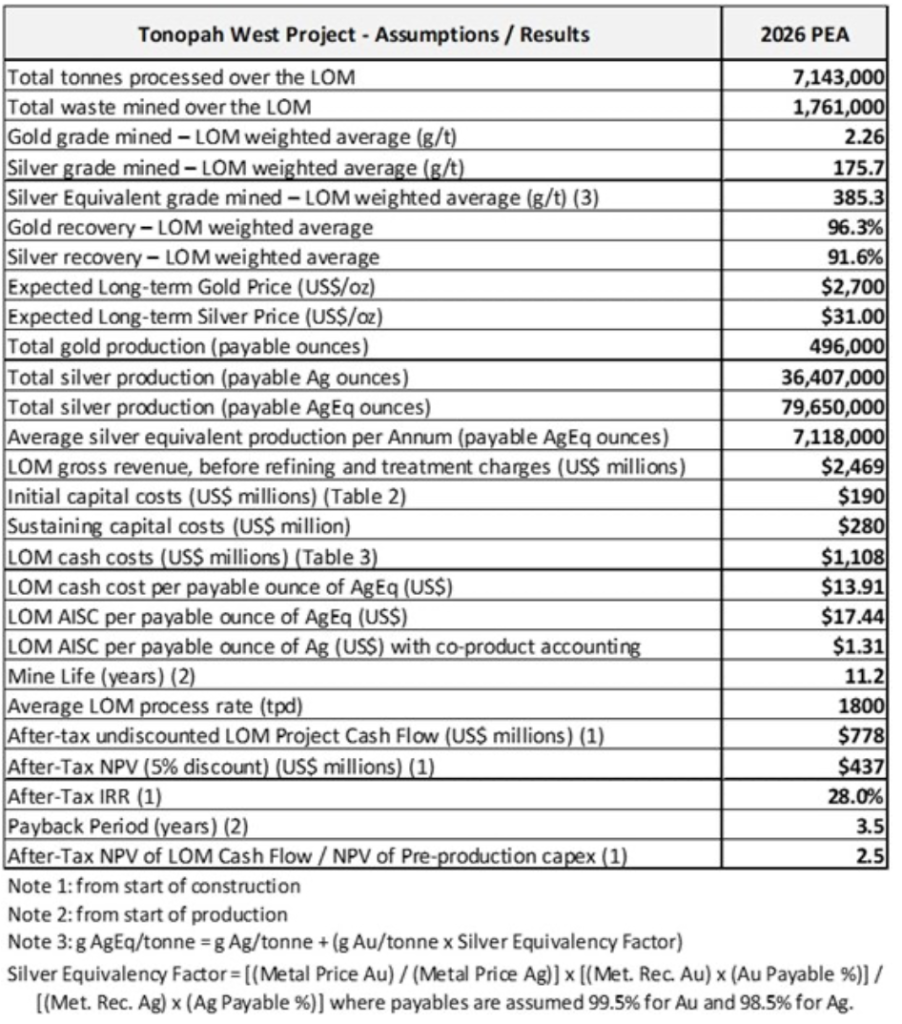

There’s BIG news at Blackrock, CEO Andrew Pollard and team just announced an updated PEA that, in my view, meaningfully de-risks the Tonopah West project. While still a PEA, not a PFS or BFS, consider the following enhanced preliminary economics.

Post-tax NPV(5%) came in at C$609M, but that’s using just US$31/oz Ag + US$2,700/oz Au. Two recent studies by Pan American Silver & Denarius Metals used $45 & $50/oz Ag, respectively.

Blackrock’s press release shows that at US$66.9/oz Ag & $4,554/oz Au, post-tax NPV is roughly ~C$2.2B with an IRR of +79% and a 1.4-year payback.

Readers should note that the mine life was extended from 8 years in the new PEA, but is still just 11 years. In my view, an acquirer or strategic partner could probably extend it further. Also noteworthy is the very low upfront cap-ex of C$265M.

The following table shows the main Ag-heavy transactions of the past 18 months. Notice the Ag prices when these deals were announced, all but one in the US$30s/oz. The world has changed since this tranche of M&A. Producers will have to pay up going forward.

That means at the indicated $66.9/oz, (currently ~$73.5/oz), the ratio of post-tax NPV to upfront cap-ex is a shockingly good 8.2 to 1. I recognize using near spot pricing is an aggressive take for a PEA-stage project, but I use spot for all peer comparisons.

All-in-sustaining-costs (“AISC“) is up considerably from the September 2024 PEA, but that largely tracks an industry-wide trend. US$17.44/Ag Eq. is squarely in the bottom quartile of mines & projects. For 4Q/25, the avg. AISC of producers was ~US$20/Ag Eq. oz.

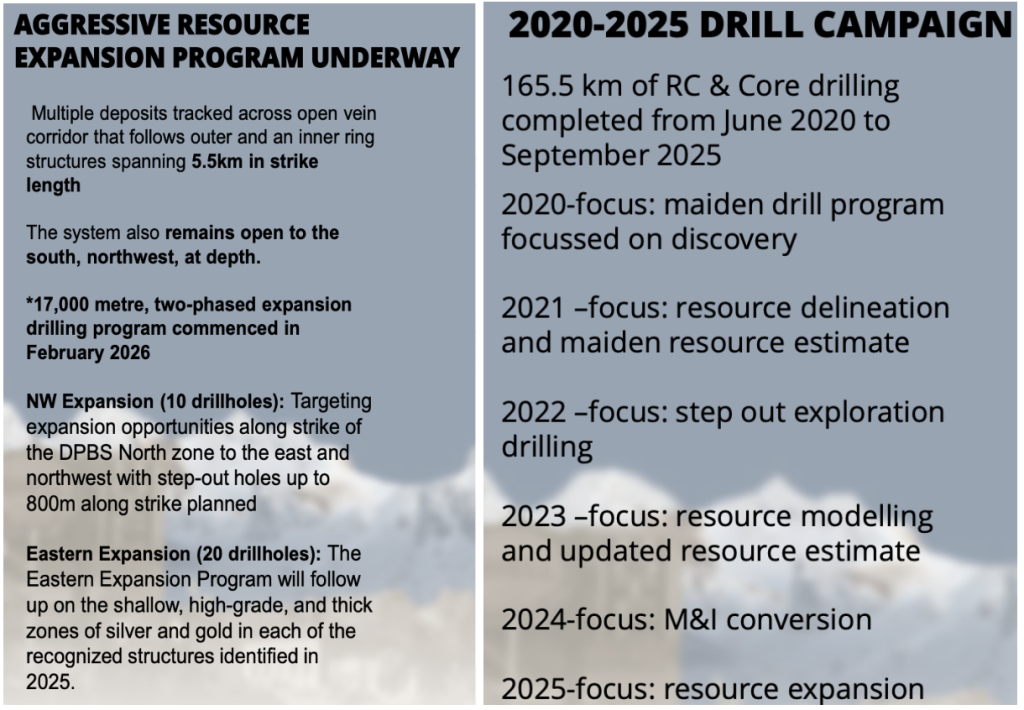

Near-term Ag futures are ~38% below January highs, so today’s levels are hardly a stretch in thinking about potential economics over the next decade. The updated resource estimate accompanying the PEA now shows nearly a third of total ounces in the Indicated category.

123.2M Ag Eq. ounces, nearly a third in the Indicated category…

Management believes exploration upside is robust. Expansion drilling to the NW identified more high-grade mineralization 500 m from the main zone. Eastern expansion drilling found several mineralized structures hosting shallow mineralization within a 1,200 m trend.

The consolidated land package consists of 25.5 sq. km (6,300 acres). A recent drill program targeted both resource conversion & expansion across multiple vein systems (especially DPB south, and NW step-out) with the goal of increasing resource continuity by linking zones.

Prospective acquirers of Blackrock include; Nevada Gold Mines (a Newmont/Barrick JV), AngloGold Ashanti, Pan American Silver, Fresnillo plc, Coeur Mining, Hecla, Kinross, Equinox Gold, First Majestic, Hycroft Mining, I-80 Gold, and SSR Mining.

If one considers Cu-heavy names that dabble on the precious metals side, one cannot rule out Freeport, BHP, RIO, Glencore, and the Grupo México/Southern Copper/ASARCO conglomerate (considerable assets in neighboring Arizona). Not that q2w

Several companies named are probably too big to care about tiny Blackrock, but mid-tiers looking to be taken out by Majors would benefit by beefing up with projects like Tonopah West.

Earlier I implied that S. American projects are more risky than Blackrock’s Nevada location, but there’s a lot more to be said about Tonopah West in particular. A key point is that it’s on private/patented land, meaning it will avoid the lengthy NEPA/federal permitting process.

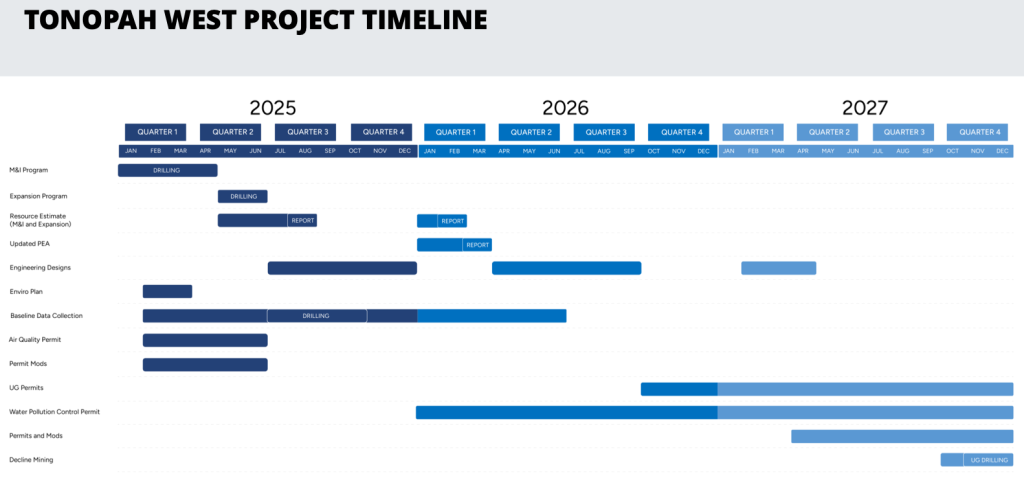

CEO Pollard believes Tonopah West might be the next U.S. based primary Ag project to enter production as it could be fully permitted and construction-ready by mid-2027. Multiple permitting-related press releases are expected through the remainder of the year.

The Project is on private land, enabling an expedited permitting path. The goal is to break ground on an underground portal and test mine in 2027, and possibly begin bulk sampling/test mining in 2028.

On March 3rd, management announced the receipt of the first of three permits from the Nevada Department of Environmental Protection.

Waste dump, stockpiles and portal entry engineering designs are on schedule and will be completed and used to calculate surface disturbance that will be the cornerstone for the Modification to the Nevada Reclamation Permit.

This five year permit, which can be extended & modified, allows for the disturbance of up to 150 acres. Data collection continues for the hydrogeological & geochemical programs that will form the basis for the Water Pollution Control Permit.

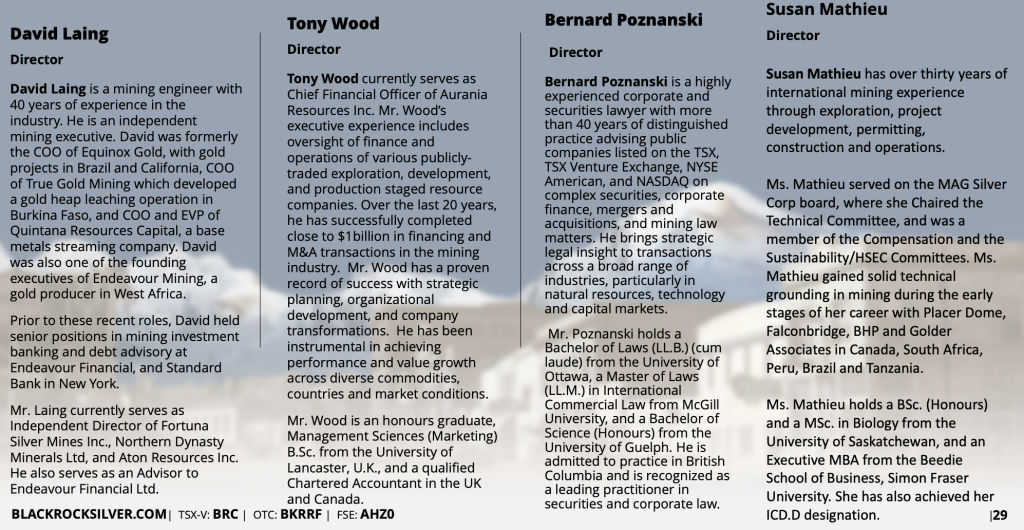

Two new Board members were announced on March 4th. Bernard Poznanski is a corporate & securities lawyer with 40+ years’ experience advising companies on financings, M&A, cross-border transactions, and governance, particularly natural resource companies.

Susan Mathieu brings 30+ years of global mining experience across exploration, development, and operations in leadership roles. She served five years on the MAG Silver board and holds science, MBA, and ICD.D credentials.

Logistically, it doesn’t get much easier. The Project is directly off a highway near power, workers, services & equipment. Another critically important factor is Tonopah West’s metallurgy.

The Project boasts simple, high-grade, narrow-veins. Therefore, processing should be straightforward –-> crush only, no flotation or gravity separation, allowing for a low-cost operation. Recoveries in the new PEA came in at a solid 96.3% Au / 91.6% Ag.

Importantly, approximately 80% of mining is planned as long-hole stoping (the cheapest conventional underground method). Tonopah West will produce Ag/Au (no zinc, lead, or copper and associated deleterious materials) in a clean, high-grade ore that should be in high demand.

Bottom line: Blackrock Silver is in the right place, at the right time with a very high-grade Ag-heavy project. The Company has an excellent management team & board, See bios above.

While many global projects at PEA stage are 6-12 years from production, Tonopah West could reach production in the mining-friendly jurisdiction of Nevada, USA a lot sooner.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Blackrock Silver, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Blackrock Silver are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Algo Copper was an advertiser on [ER]. Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.