Has a tsunami of precious metals M&A begun? I believe it has, highlighted by blockbuster deals for G2 Goldfields and Rupert Resources, not to mention Equinox Gold taking out Orla Mining. G2 and Rupert are noteworthy because they are not producers. In fact, they’re years from production (neither has a Feasibility Study yet).

Another important takeaway is that G2 & Rupert are being acquired at very strong valuations, at Enterprise Value (“EV“) to gold (“Au“) equiv. ounce ratios above C$550/oz! Granted, both have world-class projects with good grades (an avg. of ~3.9M Au Eq. ounces at ~3.8 g/t Au Eq.).

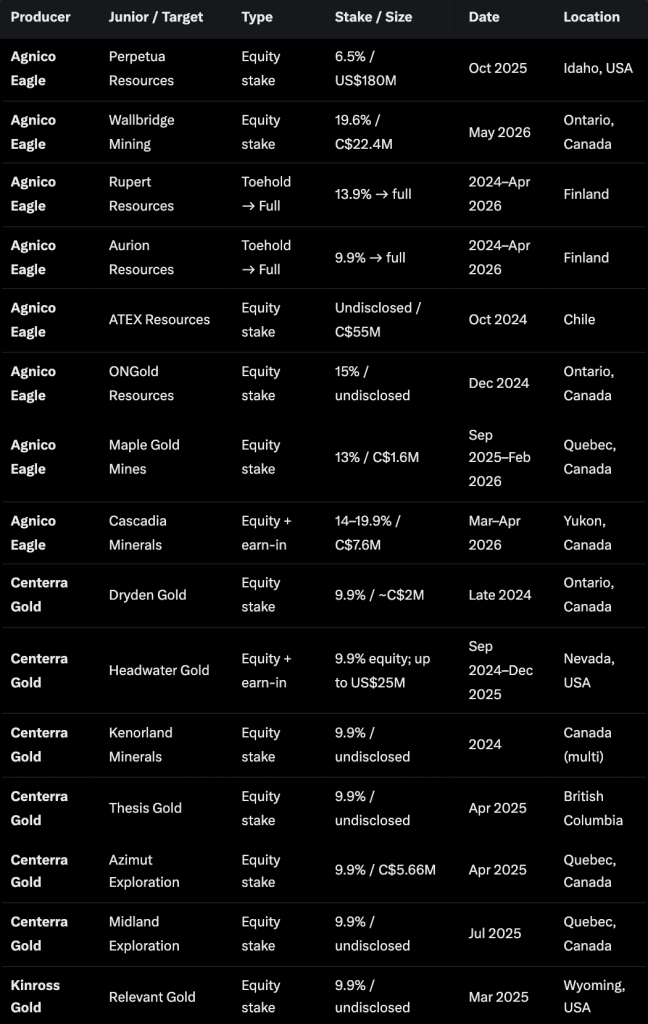

Clear evidence of an incoming tsunami can also be found in a meaningful uptick mid-tiers and Majors making investments directly into juniors. The following table shows a small portion of strategic investments made in the past year. I could show many more, but you get the idea.

Imagine how many juniors could be taken out in the coming years. Combined, producers are generating tens of billions in free cash flow per year. With Au around $4,500/oz, (almost $5,600 in January), top players have Nvidia-like margins.

What does this mean for other early-stage juniors, especially ones in great jurisdictions like Canada, with strong teams and high-grade prospects? District-scale, high-grade projects in prolific, safe jurisdictions, not too remote, surrounded by supportive local communities, run by strong management teams are ones to focus on.

Dryden Gold (TSX-V: DRY, OTCQX: DRYGF) controls 100% of a 90,000+ hectare land package along a 50 km gold-bearing trend in NW Ontario’s Manitou-Dinorwic deformation zone. This has district-scale potential in the Kenora Gold District.

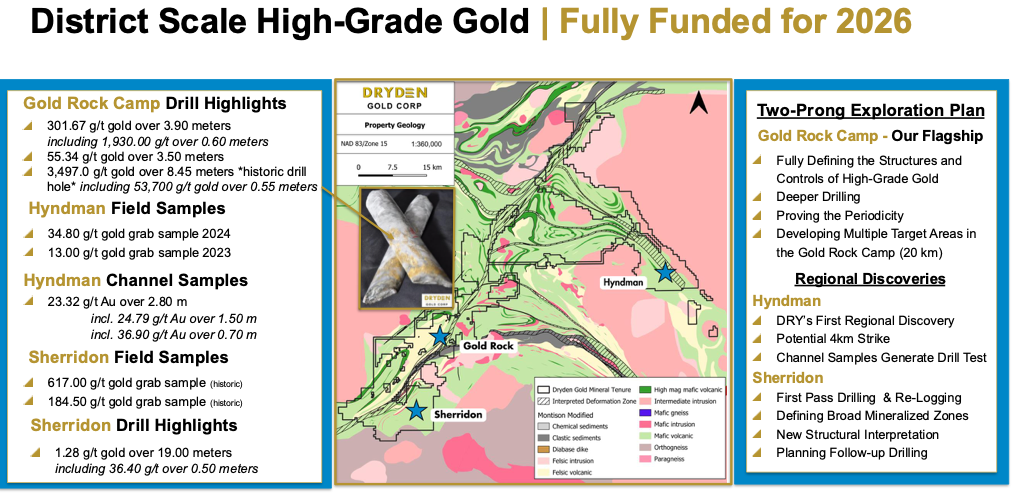

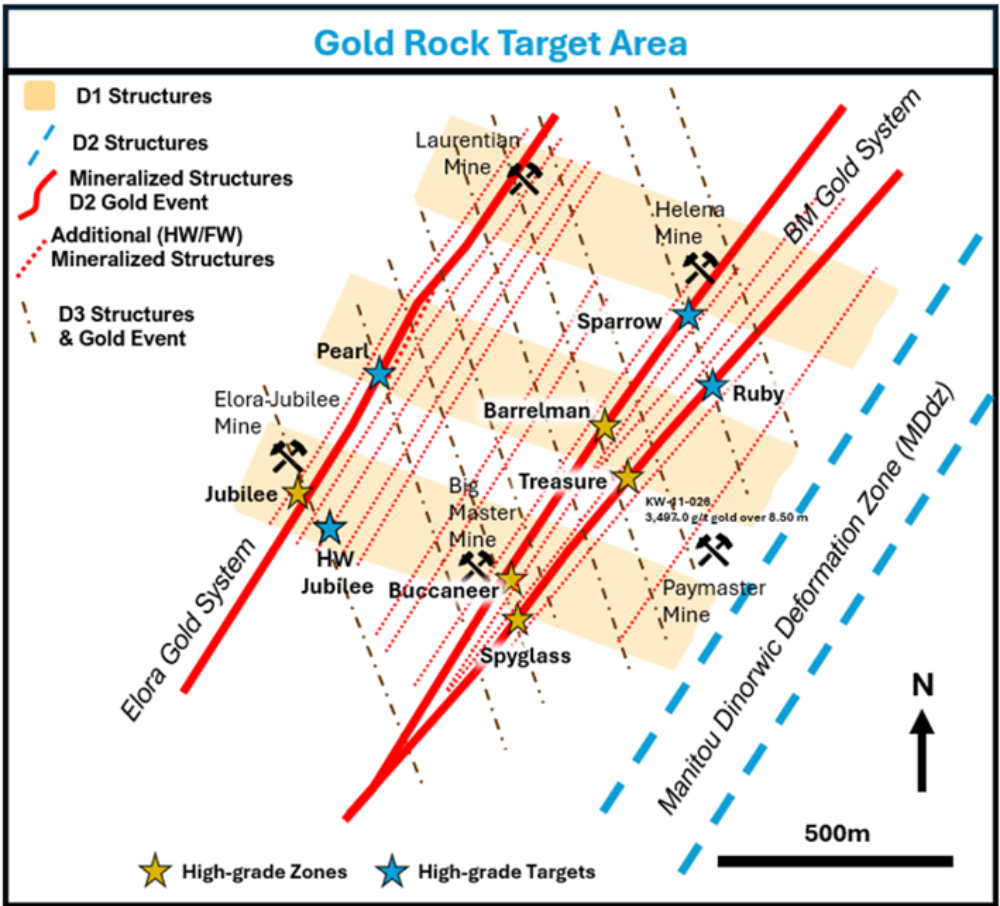

Dryden’s consolidated land package hosts high-grade structurally-controlled orogenic Au along a 20 km trend including the Gold Rock Target Area which includes the Elora Gold System (containing the Pearl & Jubilee zones), and the nearby Big Master Gold System (containing Treasure & Barrelman).

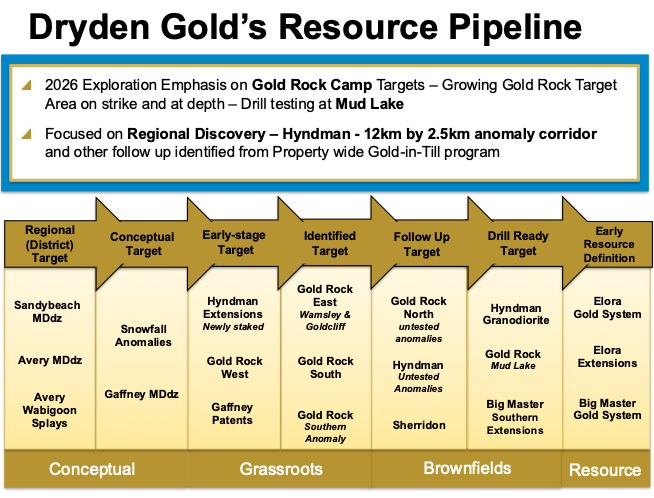

These targets focus on expansion on-strike, down-plunge. Hyndman is a 12 km x 2.5 km anomaly corridor with a distinct mineralization style). Sherridon has high-grade historic samples. Hyndman & Sherridon are separate regional targets receiving dedicated follow-up drilling this season.

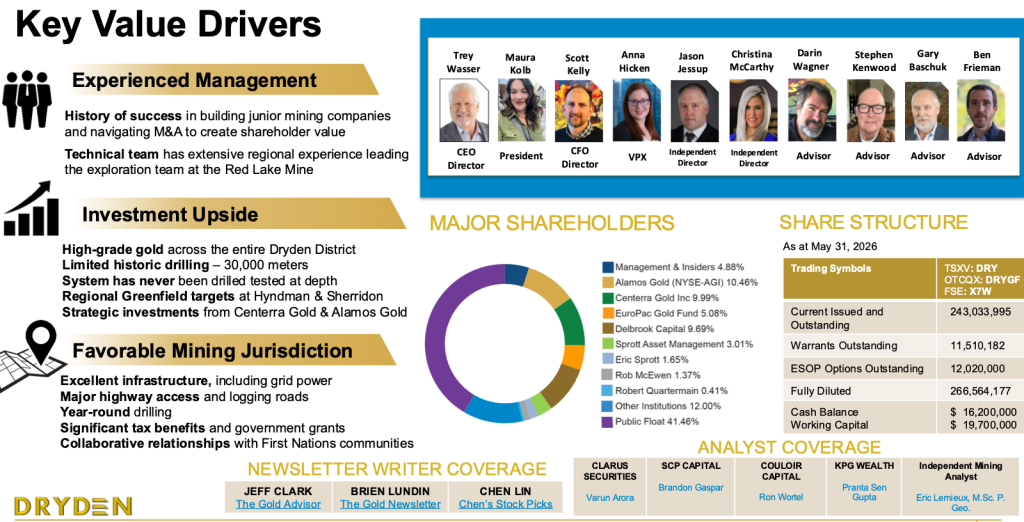

Dryden’s sizable portfolio sits in an under-explored greenstone belt with historic high-grade production . The team and the footprint are validated by significant equity stakes from Alamos Gold (10.5% owner) + Centerra Gold (9.9% stake). Importantly, ~C$9M was just raised, giving the Company ~C$20M in working capital. Both Alamos & Centerra topped up in the latest round.

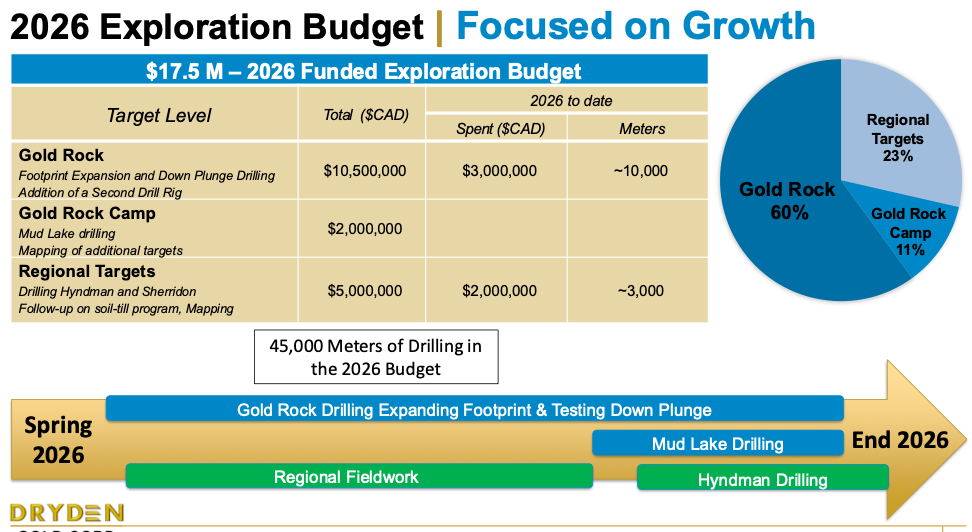

Management is fully funded for a 45,000-meter drill campaign at an industry-low, all-in drilling cost of ~C$330/meter. Dryden enjoys year-round site access, ensuring a steady cadence of news flow & investment catalysts. The additional funding will also significantly increase regional prospecting, mapping and sampling with three additional crews.

Recent drilling is building the case for a broader high-grade system, not just a single narrow target. Three new high-grade zones, and a single hole that intersected 15 mineralized structures, have strengthened the view that Gold Rock could host multiple parallel trends. I mentioned several targets/zones.

These kinds of Archean Au systems tend to host numerous stacked parallel structures. On April 2nd, additional smoke was identified via three high-grade discoveries:

Sparrow (BM1) — 4.3 m @ 32.9 g/t Au, incl. 0.5 m @ 252 g/t, from 160 m depth on a 300 m NE step-out from the Treasure/Barrelman zones.

Ruby (BM2) — 4.0 m @ 6.5 g/t Au, incl. 1.5 m @ 16.1 g/t, from 80 m depth on another 300 m NE step-out targeting the BM2 structure.

Buccaneer (BM1) — 3.8m @ 13.1 g/t Au, incl. 1.2 m @ 41.5 g/t, from 190 m depth, 80 m below the historic Big Master Mine workings, 300 m SW of Barrelman.

All three holes targeted intersections of the main mineralized structures (BM1 and BM2— parallel to the Manitou Dinorwic deformation zone) with newly identified D3 cross-cutting structures, focusing on intersections of the main mineralized structures (BM1, BM2, Elora — parallel to the Manitou Dinorwic deformation zone) with newly identified D3 cross-cutting structures.

The theory is that D3 intersections control the highest-grade Au was proven at Pearl, and is now confirmed in at least three more discoveries Gold Rock hosts at least 15 parallel mineralized structures, with many D3 intersections still untested.

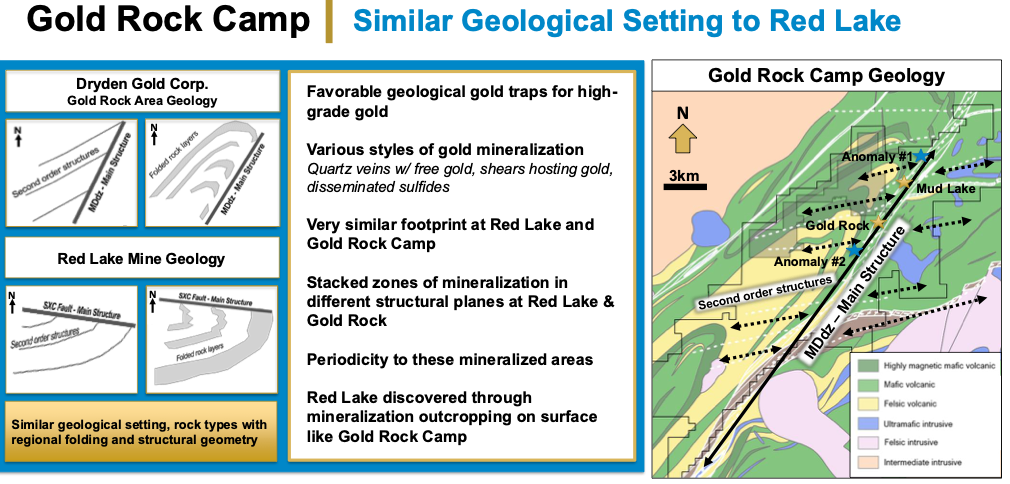

CEO Trey Wasser noted the program has “shifted into high gear,” with last year’s discovery of numerous stacked structures — comparable to the well known Red Lake camp.

Big Master shows the same structural patterns identified at the Elora shear, where drilling revealed vertically oriented high-grade, stacked mineralization. The improved and growing understanding allows the team to better predict mineralization across the broader Gold Rock system.

On June 4th the Company delivered another strong batch of drill intervals, highlighted by 14.8 m of 3.2 g/t Au, incl. 1.4 m of 25.6 g/t. In the PR CEO Wasser stated,

“The geology team continues to deliver both high-grade results and wide lower grade intercepts, near-surface, across the 1 square kilometer footprint at Gold Rock. Last year’s discovery of multiple parallel mineralized structures and the gold bearing D3 deformation event has led to the development of dozens of additional high-grade drill targets (Figure 1). We have now developed and tested the 3-D geological model to more accurately define new targets and expand known zones at depth.”

Notice the numerous named targets, incl. high-grade zones

President Maura Kolb P.Geo. added,

“…we have a high degree of confidence in the new geological model and want to accelerate its evaluation through a more aggressive drilling program… initial testing of near-surface structural intersections has delivered encouraging results. We believe there is significant potential to add value and expand the Gold Rock project by systematically testing these near-surface targets. There are currently very few drill pierce points below 300 meters and the down-plunge potential of the system is largely untested. Evaluating deeper targets is a priority… We will maintain an aggressive near-surface drilling program on newly discovered stacked structures while testing the deeper potential of the deposit.”

Management is steadily advancing and de-risking Gold Rock. The April discovery proved the geological model. May drilling at the Jubilee/Elora system added high-grade results. The June 4th PR showed wider, more consistent intercepts. Geological confidence is growing, with deeper drilling and a new regional target at Hyndman now in play.

Results are supportive of strike continuity, stacked structures, and depth extensions, substantially expanding the

potential of the mineralized footprint. Intercepts include spectacular grades. How spectacular? How about 301.7 g/t Au over 3.9 m, incl. 1,930 g/t over 0.6 m in May 2025, or an historical interval of 3,497 g/t Au over 8.45 m in 2011?

And, this was in one of the newly discovered stacked hanging wall structure. In February management reported 6.4 g/t Au over 3.3 m, incl. 152 g/t over 1.0 m in a new high-grade footwall zone. High grade is one thing, shallow depth is even better. February’s one meter intercept of 152 g/t was from 17-18 meter depth.

In mid-May the Company announced 2.9 g/t Au over 14.5 m which further defined mineralization at Jubilee. The team will add a second drill rig in July to further expand Gold Rock. One rig will continue to test across the stacked structures and infill between the high-grade zones. The second rig will drill deeper holes to expand the high-grade zones down plunge.

The Company is awaiting drill results from Hyndman, its first in-house discovery, marking a key milestone and potential catalyst. New soil data identified additional targets and is helping refine understanding of other large areas like Sherridon. The team is prioritizing and ranking targets to guide the planned 45,000-meter drill program, with Gold Rock remaining a central focus.

The Company is fully funded for its drill program across multiple targets (including Hyndman & Sherridon). property-wide gold-in-till anomalies further support exploration potential. Dryden reported results from 3,816 gold-in-till samples outlining multiple anomalies along a 65 km corridor, with especially strong responses at the Hyndman target.

These anomalies cluster at key structural intersections, extending across under-explored ground, confirming district-scale potential, and defining new priority targets.

This work led to the staking of 5,200+ additional hectares at Hyndman. In my view, these results continue to point to district-scale potential. The technical team has identified structurally controlled zones, and highlighted new areas (especially at Hyndman) as exciting drill targets.

Dryden Gold ((TSX-V: DRY, OTCQX: DRYGF) is funded for a lot of exploration across multiple targets in 2026. High-grade juniors with sizable land packages in Tier-1 locations like NW Ontario are very well positioned.

The Company doesn’t need higher Au prices to keep key shareholders Centerra & Alamos interested in learning more about its growing district-scale portfolio.

Today’s Au price above $4,500/oz makes those high-grade hits significantly more valuable, while at the same time potential strategic investors and/or acquirers are substantially stronger, enjoying tremendous cash free cash flow, to make numerous investments into companies like Dryden Gold.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Dryden Gold Corp, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Dryden Gold are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Dryden Gold was an advertiser on [ER]. Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.