Blackrock Silver is a sponsor of Epsten Research [ER], please see details at bottom of page.

Silver (“Ag“) is up +125% in the past year. However, investors are focused on near-month futures down ~39% from ~US$122/oz in January.

Gold (“Au“) is down ~$1,100/oz from its high of ~$5,600, attributable to central bank selling by Turkey & Russia to defend their currencies, and/or fund troubled economies. Some countries have slowed Au buying due to adverse impacts from the Middle East war. A strong US$ and a more hawkish U.S. FED are also weighing on Au.

However, the same bullish precious metal fundamentals that drove Ag/Au to ATHs in January have not changed. Globally, geopolitical risks only grow, further dividing the East & West. Debt levels are very high and rising. The U.S. has $39 Trillion in debt. In my view, central bank buying will return.

I believe high-quality Ag/Au developers & explorers offer attractive investment propositions. The last major bull market saw Ag run +1,100% from under $5/oz in Nov. 2001 to nearly $50 in April 2011. Au was +650% from $255/oz in July 1999, to $1,915 in Sept. 2011.

Compare those 10-12 year periods to the current bull market approaching 3 years. Au is +150% and Ag +265%. Room to run?

Make no mistake, even in a bull market, some projects are riskier than others. Readers can invest in precious metal juniors with promising assets in Canada, the U.S., and Australia. Or, push their luck in places like; Bolivia, Russia, Mali, the DRC, Panama, Guinea, Ghana, Burkina Faso.

Burkina Faso & Panama were once considered rising stars, but things change. Globally, resource nationalism and security issues (gangs/wars/coups) are not uncommon. Importantly, most Tier-1 Ag-heavy projects are in S. America or Mexico. The best places to develop projects are the U.S. and Canada.

The U.S. is especially attractive given tariff uncertainties and newly enacted financial incentives (tax breaks, free-money grants, low-cost loans, etc. for critical material like Ag. There’s also talk of streamlined permitting under the Trump Administration.

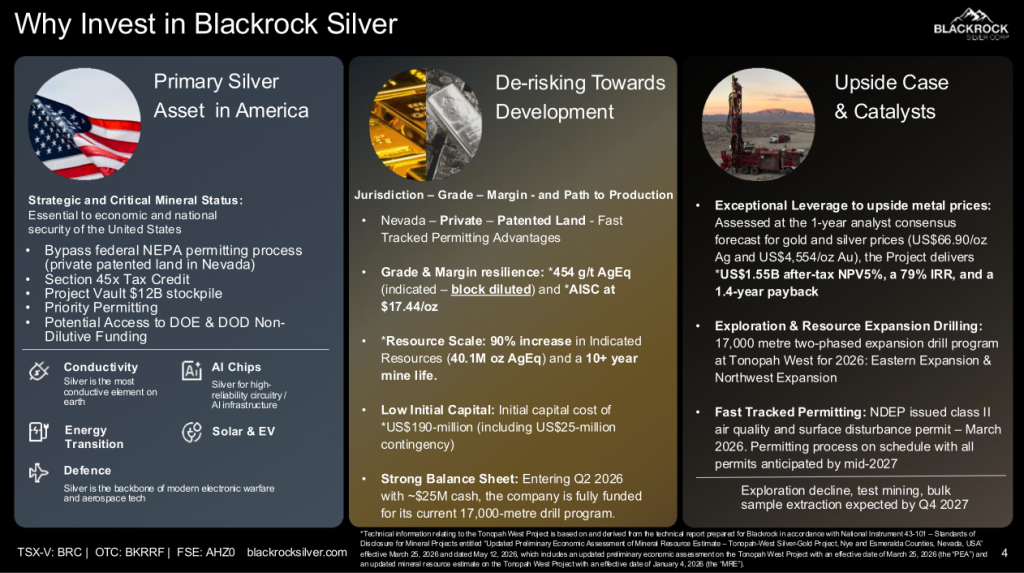

A primary Ag junior I continue to love is Blackrock Silver (TSX-v: BRC) (OTCQX: BKRRF). Its flagship project is in Nevada, USA, the world’s top mining jurisdiction (ranked #1 in the most recent annual Fraser Institute Mining Survey). Along with many Ag stocks down as much or more, Blackrock is down 50% from its high. Buying opportunity? Keep reading…

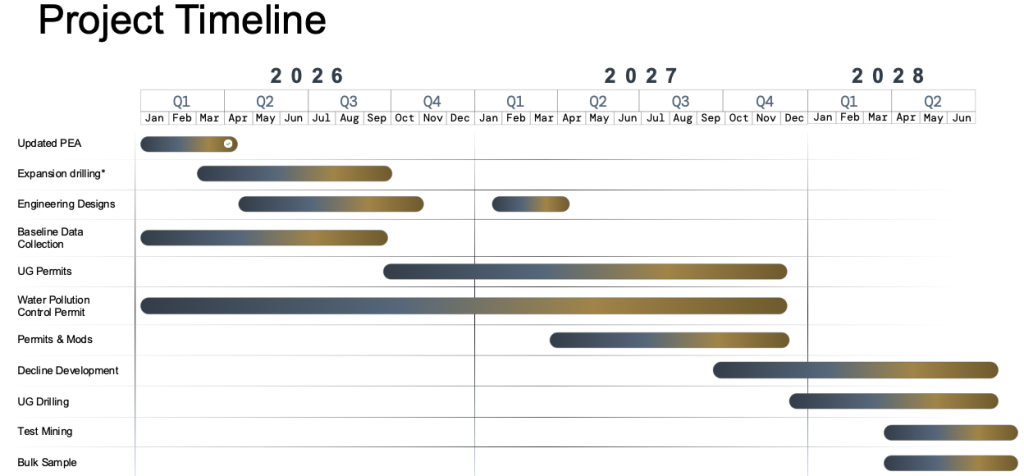

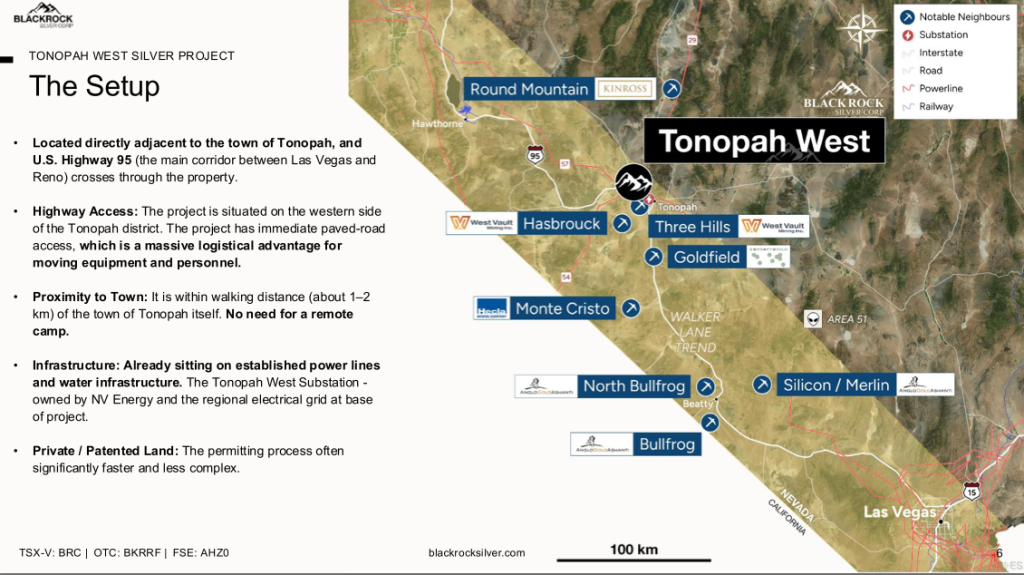

Blackrock’s Tonopah West project sits in the historic Tonopah Silver District, part of the larger Walker Lane Trend. Significant drill results are expected to start flowing in June, more on that later…

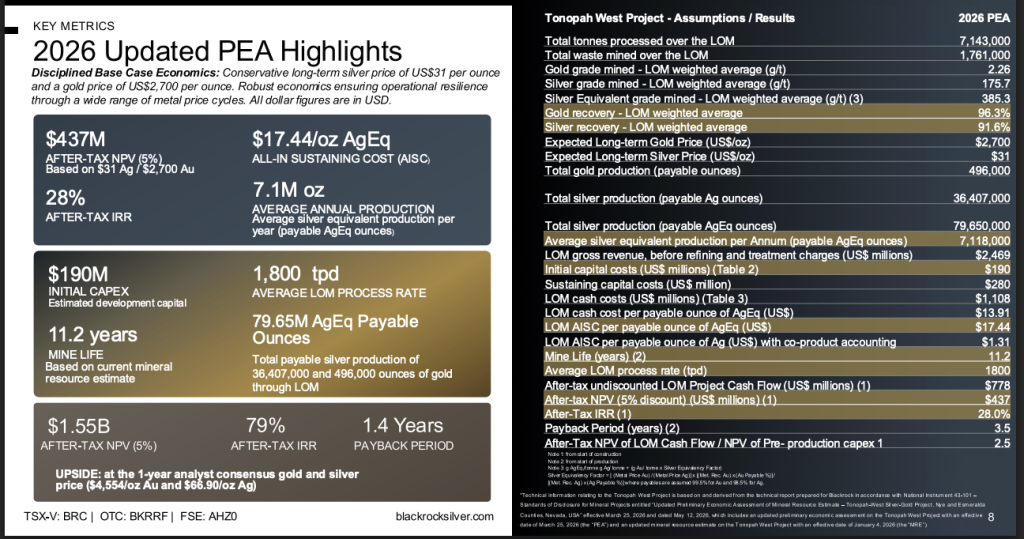

In late March, CEO Andrew Pollard and team announced an updated PEA that meaningfully de-risked the Tonopah West project. Consider the above enhanced preliminary economics.

Post-tax NPV(5%) came in at C$603M, but that’s using US$31/oz Ag + US$2,700/oz Au. Recent studies by Pan American Silver, Silverco Mining & Denarius Metals used US$44.6 to $50/oz Ag. The updated resource estimate accompanying the PEA shows nearly a third of total ounces in the Indicated category.

Blackrock’s press release showed that, all else equal, at US$66.9/oz Ag & $4,554/oz Au, post-tax NPV is roughly ~C$2.1B with an IRR of 79% and a 1.4-year payback. Note that near-month Ag futures hit $90/oz earlier in May. This means at $66.9/oz, (currently ~$75/oz), the ratio of post-tax NPV to upfront cap-ex is an amazing 8.2 to 1.

123.2M Ag Eq. ounces, nearly a third in the Indicated category…

The PEA showed very good recoveries (91.0-91.5% Ag, 96-97% Au), with clean metallurgy (silver + gold only, no base metals).

Using spot pricing is an aggressive take for a PEA-stage project, but I use spot for peer comparisons. Readers should note, mine life was extended from 8 to 11 years. In my view, an acquirer or strategic partner could reasonably be expected to extend it even more.

The very low upfront cap-ex of C$265M makes Blackrock a junior that could be acquired by dozens of C$3B+ companies. To be clear, management is in no rush to sell anywhere near today’s valuation. Nor is it forced to do a deal with a larger company anytime soon, unless on attractive terms. It has over C$20M in cash.

The following table shows Ag-heavy transactions from the past 18 months. Notice the Ag prices at the times when these deals were announced. All but one were in the US$30s/oz. Producers will have to pay up for Tier-1 assets going forward.

All-in-Sustaining-Cost (“AISC“) in the new PEA was up from the September-2024 PEA, but that tracks an industry-wide trend. Still, US$17.4/Ag Eq. remains in the bottom quartile. I estimate that for 1Q/26, the median AISC, was in the mid~US$20s/Ag Eq. oz.

On the higher end, Avino Silver & Gold, First Majestic, Americas Gold & Silver, Endeavour Silver, and SantaCruz Silver printed AISC figures between US$30 and $37/Ag Eq. oz. Even as West Tonopah’s $17.4/oz estimate climbs between now and first production, so too will the AISCs of most producers.

Blackrock’s project is not huge, but if/when it hits nameplate capacity of 7.1M Ag Eq. oz/yr., it would be larger than the current production rates of Aya Gold & Silver, Avino Silver & Gold, Americas Gold & Silver, and SantaCruz. Those four have an average market cap of ~C$3B.

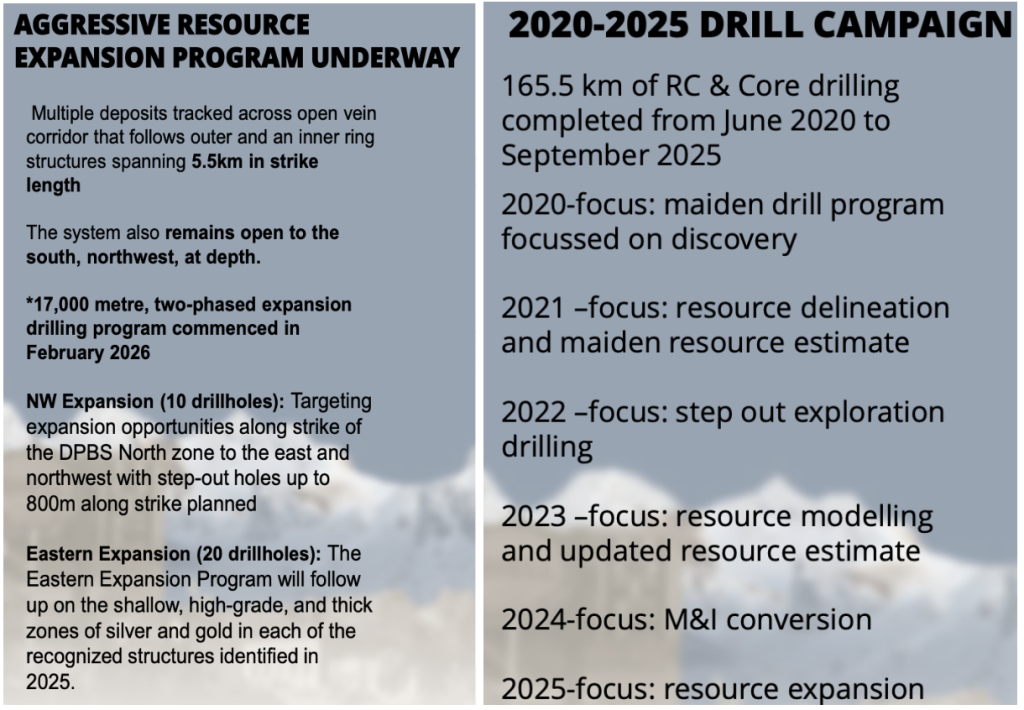

Turning to drilling, this is an exciting part of the story. Expansion to the NW identified more high-grade mineralization 500 m from the main zone. Eastern expansion found several mineralized structures hosting shallow mineralization within a 1,200 m trend.

The consolidated land package consists of 25.5 sq. km. A recent drill program targeted both resource conversion & expansion across multiple vein systems (especially DPB south, and NW step-out) with the goal of increasing resource continuity.

The latest program is potentially impactful. Results are expected to start flowing next month. In addition to low-risk step outs from known shallow, higher grade mineralization, major step-outs up to 800 meters are being done. Management calls the 800 m step outs “moonshots.” Presumably there are good reasons to attempt these moonshots.

See image below describing “Aggressive Resource Expansion Program…”

Less risky than 800 m step outs is high-impact drilling to the east where ~15M Ag Eq. (Inferred) shallow, higher-grade ounces have been delineated. Armed with a better understanding of this area, a doubling of that 15M figure this drill season is a reasonable expectation.

If 30M Ag Eq. ounces, that could move the needle on project economics. Management is hoping to pull forward higher-grade, less costly (shallow) ounces from end of mine life towards year 3 or 4.

The most likely acquirers of Blackrock? Nevada Gold Mines (a Newmont/Barrick JV), Agnico, AngloGold Ashanti, Pan American Silver, Fresnillo, Alamos, Coeur, Hecla, Kinross, Equinox Gold, First Majestic, Hochschild, I-80 Gold, B2Gold, and SSR Mining — and don’t ignore royalty/streaming giants like Franco-Nevada & Wheaton Precious Metals.

If one considers Cu-heavy names that dabble on the precious metals side, one cannot rule out Freeport McMoRan, BHP, RIO, Glencore, and the Grupo México/Southern Copper/ASARCO conglomerate (considerable assets in neighboring Arizona).

Mid-tier Polish producer KGHM operates in Nevada. Lundin Mining & HudBay Minerals could potentially care. I just name-dropped over two dozen groups, some of which CEO Pollard is probably talking with, but I don’t know which ones.

Many named could be too big to notice Blackrock Silver, but mid-tiers looking to be taken out by Majors would certainly benefit by beefing up with acquisitions of world-class projects.

A key attribute of Tonopah West is that it’s on private/patented land, meaning it will avoid the lengthy NEPA/federal permitting process. That’s why CEO Pollard believes the Project could be one of the next U.S. based primary Ag assets in production.

It could have key permits in place and be development ready in 2H/27. On March 3rd, management announced the receipt of the first of three permits from the Nevada Department of Environmental Protection. More permitting-related press releases are expected through the remainder of the year.

The goal is to break ground on an underground portal, and possibly begin bulk sampling/test mining in 2028. Logistically, it doesn’t get much easier. The Project is directly off a highway near power, workers, services & equipment. Another critically important factor is Tonopah West’s metallurgy.

The Project boasts high-grade, narrow-veins. Therefore, processing should be straightforward –-> crush only, no flotation or gravity separation, allowing for a potentially low-cost operation (sub US$20/oz AISC).

Importantly, ~88% of mining is planned as long-hole stoping (the cheapest conventional underground method). Tonopah West will produce Ag/Au (no zinc, lead, copper and associated deleterious materials) in a clean, high-grade concentrate. This is a low risk mine plan.

Blackrock Silver (TSX-v: BRC) (OTC: BKRRF ) seems undervalued given an impressive list of attributes including; high-grade, #1 mining jurisdiction, strong team, low technical risk (attractive metallurgy), expandable mine life (excellent exploration upside), and low estimated op-ex (AISC) & cap-ex.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Blackrock Silver, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Blackrock Silver are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Blackrock Silver was an advertiser on [ER]. Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.