Table of Contents Show

JPMorgan, Microsoft Back $210 Million Carbon Loan in Landmark Climate Finance Deal

JPMorgan Chase closed a landmark $210 million carbon loan to support Chestnut Carbon, a U.S.-based afforestation firm, in a move that could reshape how climate projects are financed. Microsoft also played a key role in this breakthrough. They committed to buying a large share of the high-quality carbon removal credits from the project.

The dual involvement of a leading global bank and a major tech firm shows rising trust in nature-based carbon removal. It is seen as a real, profitable asset class.

JPMorgan’s Climate Finance and Advisory team, ERM (an environmental consulting firm), and Chestnut Carbon formed a partnership that made the transaction possible. It shows a change in how carbon projects are financed. This is especially true for nature-based solutions, like afforestation.

Other major lenders include CoBank, Bank of Montreal, and East West Bank. So, what makes this funding different from existing climate financing models? Let’s find out.

How the Financing Structure Works

The deal marks the largest-ever non-recourse project financing in the voluntary carbon market (VCM). The program, funded by future carbon credit revenues, aims to plant forests and remove CO₂ across the U.S. for 30 years.

Microsoft’s purchase agreement made the deal less risky. This gave JPMorgan the confidence to structure and underwrite the loan.

This carbon loan is notable because it uses future carbon credit revenue as collateral. Chestnut Carbon expects to generate millions of tons of carbon credits over the life of the forests it’s planting. These credits will be verified and sold in the voluntary market.

Instead of waiting decades for the trees to grow and credits to be sold, Chestnut Carbon now has upfront capital to scale quickly. The loan will be repaid over time as credits are generated and sold.

This structure is common in renewable energy or infrastructure—but it’s new to carbon markets, especially in the U.S.

The design of the model aims to de-risk investment by separating project performance from broader market volatility. That makes it easier for pension funds, banks, and institutional investors to enter the carbon space.

Chestnut’s Chief Financial Officer, Greg Adams, remarked:

“Not only does this facility provide the capital to accelerate our afforestation and carbon removal initiatives, but it establishes a replicable model for sustainable finance in the voluntary carbon sector.”

Chestnut Carbon’s Afforestation Mission

Chestnut Carbon focuses on afforestation, which involves planting trees on land that hasn’t been forested for a long time. This differs from reforestation (which restores forests after logging or wildfires). It is especially useful in regions like the U.S., where marginal lands are convertible into carbon sinks.

Chestnut Carbon Projects

Source: Chestnut Carbon

Source: Chestnut Carbon

The company’s long-term goal is to plant trees across tens of thousands of acres, targeting carbon removal at scale. Their model includes:

- Rigorous monitoring and MRV (measurement, reporting, and verification) using satellite data and third-party audits

- Carbon credits certified under leading registries like Verra or ACR

- Partnerships with local landowners to secure access to suitable land

- Biodiversity and ecosystem restoration as co-benefits of the program

Chestnut Carbon’s credits aim to meet the growing need for trustworthy carbon removals. This is particularly important for big companies with net-zero targets. ERM, which advised on the deal, says this model is replicable in other places. It can help fund similar nature-based climate projects globally.

Wall Street Meets the Forest: A Signal to Carbon Investors

This financing is a game-changer for the voluntary carbon market. It has faced problems like low liquidity, verification issues, and a lack of investor trust. Here’s what this deal signals to the broader market:

- VCM Projects Are Bankable:

JPMorgan and partners created a non-recourse loan using carbon credits. This shows that institutional investors see high-quality carbon projects as financially viable, not just charitable.

The structure used in this deal can now serve as a blueprint. JPMorgan has signaled interest in scaling this model to other project developers and regions—especially those in Latin America, Southeast Asia, and Africa.

- Meeting Corporate Carbon Goals:

As demand for verified carbon removals grows—driven by new SEC and EU regulations—companies are scrambling to find high-quality offset credits. This creates a strong buyer base for the types of credits Chestnut Carbon will issue.

- Liquidity and Credibility Boost:

Third-party financing increases transparency and accountability. That helps solve two major problems in the carbon credit market: poor liquidity and doubts about credit quality.

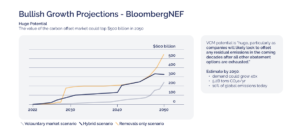

BloombergNEF reports that the VCM could jump from $2 billion in 2024 to $50 billion by 2030. This growth is likely as net-zero goals become real and reporting rules get stricter. In a more optimistic outlook, the market could reach up to $500 billion by 2050.

Chart from DGB Group

Chart from DGB Group

Carbon Credits and the Path to Net Zero

Carbon credits allow companies to offset emissions they can’t yet eliminate. But not all credits are created equal. There’s a growing interest in removal-based credits, such as afforestation, instead of avoidance methods, like stopping deforestation.

Chestnut Carbon’s model supports this shift. Each project removes CO₂ from the atmosphere by planting trees that sequester carbon over decades. These credits will qualify for science-based targets and corporate ESG reporting under frameworks like the GHG Protocol and SBTi.

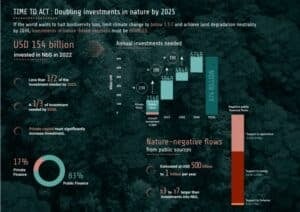

JPMorgan’s role shows that carbon markets are now central to finance, not just a side tool. Their deal helps close the financing gap for nature-based solutions. The United Nations estimates that $387 billion per year is necessary through 2030 to meet climate goals.

Source: United Nations Environment Programme

Source: United Nations Environment Programme

Vijnan Batchu, Global Head of Center for Carbon Transition at J.P. Morgan, echoed this thought, saying:

“Providing this kind of financing gives developers the runway they need to succeed at an attractive cost of capital, allowing them to focus on delivering significant carbon projects and fulfilling contracts…J.P. Morgan is extremely proud to be a part of this significant deal and contribute to the growth of the carbon markets at large.”

A Template for Future Climate Finance: What Comes After the Deal?

JPMorgan’s $210 million loan to Chestnut Carbon is more than a single transaction. It’s a financial innovation that connects capital markets to real carbon removal work on the ground. It offers investors a fresh way to join climate solutions. It also provides project developers with the resources to act quickly and increase their impact.

As VMCs grow, deals like this may lead to new financial tools linked to nature, emissions, and verified climate results. They may also pave the way for carbon credit securitization, green bonds linked to offsets, or public-private climate investment partnerships.

The Chestnut Carbon deal shows that big afforestation projects can draw in large investments. They lower risks and provide clear results in the battle against climate change.