Silver (“Ag“) has had a wild ride, along with gold, even more so. Year-to-date the near month futures contract price has ranged from $61 to $122, averaging ~$82.3/troy ounce.

We are in year six of a structural mined Ag supply deficit, with demand exceeding mined supply by ~160–200 million ounces. Industrial demand — solar panels, EVs, AI/data centers, clean energy plants, high-tech electronics — accounts for over half of global consumption.

Investment demand is strong, especially in Asia. Geopolitical tensions sustain safe-haven buying, but volatility remains high. Headwinds include a stronger U.S. dollar, delayed U.S. Fed rate cuts, and potential demand substitution.

Regarding substitution, it’s not realistic for the most critical high-tech & military applications where Ag’s superior electrical/thermal conductivity, strong resistance to oxidation, and unmatched optical reflectivity reign supreme.

Project development risks can’t be avoided, but some projects are riskier than others. In looking at the Top-10 Ag producing countries, 40% (China, Bolivia, Russia & Kazakhstan) are places with elevated risk profiles, especially for Western countries to rely on.

Readers are reminded that in January 1980 the inflation-adj. all-time-high for Ag was ~$210/oz., and that was long before ubiquitous solar power, EVs, smart phones, drones and other high-tech gadgetry.

Forecasts as of mid-April for 2H/26 remain bullish, clustering around $80–$125/oz, with select bull cases at or above $125/oz. For instance, BMO is calling for $160, and Bank of America $135 to $309!, Citi sees $150 in a possible, “physical supply squeeze.”

Fundamentals are clearly bullish, but most expect elevated volatility to continue. Readers often forget that Ag is +141% in the past year, instead focusing on it being -35% from late January.

Make no mistake, any price above $50/oz. is good for high-quality Ag-heavy prospects. If a junior cannot demonstrate strong potential at today’s pricing, even with an early-stage project, that junior should consider a new business model!

An early-stage junior worth a closer look is Magma Silver (TSX-v: MGMA) / (OTCQB: MAGMF) with 100% of the high-sulfidation Ag/Au Niñobamba project. Permitting & drilling programs are advancing, with a focus on resource expansion & NI 43-101 compliance.

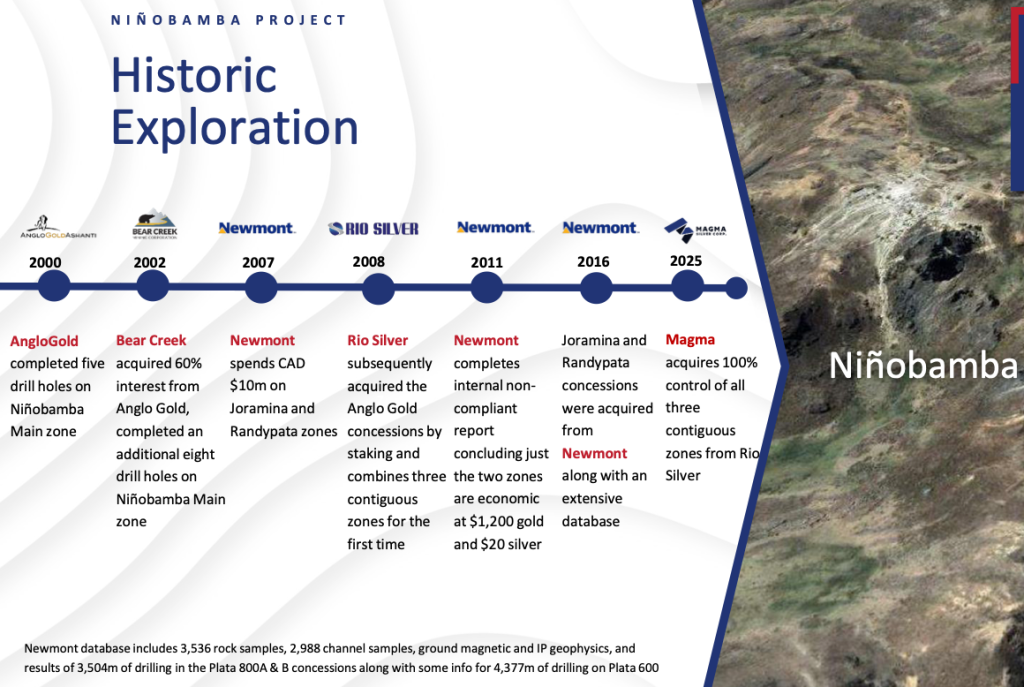

Randypata & Joramina are two of three contiguous concessions spanning an 8×2 km corridor in the mineral-rich Ayacucho region of Peru.

For the first time, this highly prospective land package is being developed under one roof. Management received a drill permit, and a US$1M, (up to 4,000 meters) drill campaign on the Joramina zone is planned for later this year.

Astute readers might note that the drill date has been pushed back, but that’s largely due to weather & logistical considerations. Roads in and around the area need to be properly maintained. Better safe than sorry. An experienced drill crew has been picked.

Magma’s enterprise value {market cap + debt – cash} is ~C$16M. Shares have fallen ~50% from their 52-week high (due to delays in the start of drilling and overall market volatility). Note, ~30 other Ag-heavy juniors are down 50% (or more) from their highs.

Niñobamba was exciting when Ag was $50/oz, it’s extraordinary at $79.4. Niñobamba is an hour from Ayacucho with daily flights to Lima. The 4,100 hectare Project is next to a highway, and 7 km from power.

The Randypata zone was re-staked during COVID-19. It was previously held by Newmont, and a 2% NSR lapsed. In today’s dollars, previous operators (Newmont, AngloGold Ashanti, Bear Creek, Rio Silver) invested a total of roughly C$20M across exploration activities.

Niñobamba includes multiple zones, the main deposit, Randypata (with a 2 km higher-grade Ag anomaly), and Joramina. The system is thought to be comparable to Pan American Silver’s former Alamo Dorado mine.

2025 field programs (trenching, sampling) confirmed, and in some cases exceeded, historical results, including multiple high-grade grab samples.

Niñobamba stands out as a relatively low-risk, high-reward, near-surface Ag/Au project with promising economics, solid financial backing, and imminent catalysts for drilling & surface exploration in the midst of an ongoing, albeit volatile, precious metals bull market.

A key attribute of Niñobamba is its anticipated (subject to further studies & drilling) amenability to low-cost, open-pit mining, and heap-leach mining methods.

Drilling highlights include; [72.3 m of 1.2 g/mt Au], [56.0 m of 1.0 g/mt Au + 99 g/mt Ag, [21.0 m of 1.32 g/mt Au + 102 g/mt Ag.

The Joramina zone has a higher-grade channel Au-only sample of 17.4 m of 3.1 g/mt Au. For a C$16M company, the mgmt. team, board & advisors are quite impressive. Three grams Au Eq. in a shallow setting is attractive.

Magma Silver has access to a dataset that includes drilling & samples records & assays, and internal (never made public) economic / fatal flaws studies done by Newmont when Au was a quarter and Ag a fifth of today’s levels.

This implies that metallurgical work and other critical mine plan metrics passed the test of reasonableness at that time. Notably, $1,200 Au was used vs. today’s price of $4,820.

Management believes there’s a significant amount of Ag & Au on the Project, but it’s NOT yet NI 43-101 compliant.

Given that Newmont did at least one economic study that did not kill the project at much lower precious metal prices, I presume it was thought to have had the potential to be a decent-sized resource.

Importantly, M&A in the precious metals space has barely just begun. Ag/Au producers are printing money. They need to bolster long-term pipelines with M&A of producers, but also development projects, including early-stage plays. Peru will remain a leading Ag/Cu/Au producer with companies including;

Grupo México/Southern Copper, BHP, Glencore, Freeport McMoran, Teck Resources, Anglo American, First Quantum, Buenaventura (BVN), MMG Limited, HudBay, Fortuna Mining & Hochschild Mining Plc leading the way.

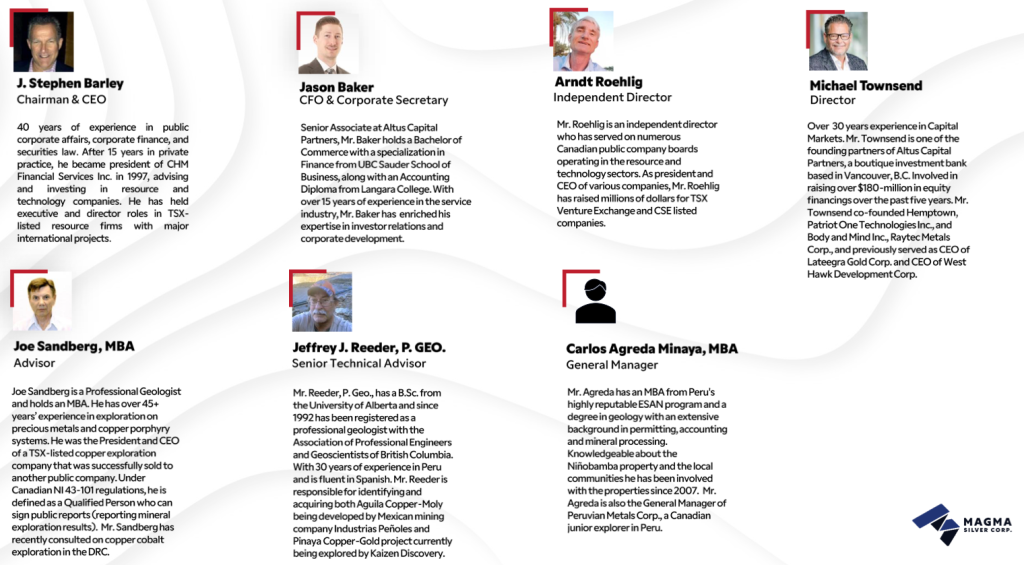

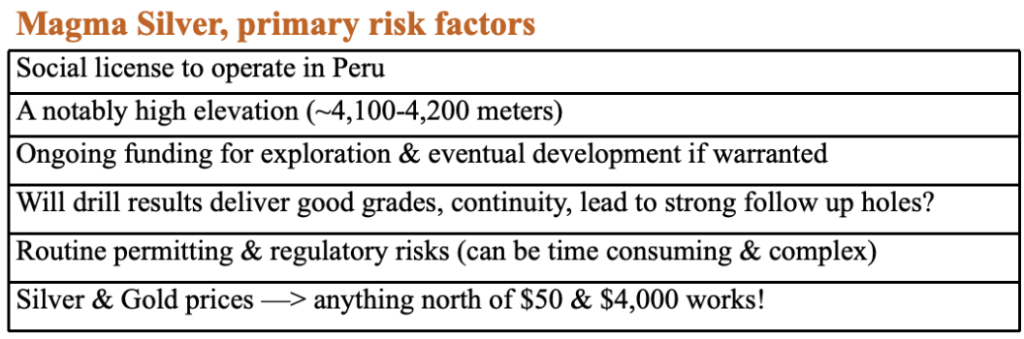

I truly believe these risks, while significant, are routine for early-stage projects around the world. Somewhat offsetting these challenges is the cheap company valuation and strong management team, board + advisors {see bios above}.

Primary risk factors, as I see them…

In addition to Chairman/CEO Stephen Barley & Dir. Michael Townsend who clearly have strong resumes, please take a moment to learn more about the technical backgrounds of Arndt Roehlig, Jeff Reeder, Carlos Agreda Minaya, and Joe Sandberg –> also impressive.

Please note that Mr. Reeder, General Manager Minaya and Senior Field Geo Edgar Leon Choque have extensive boots-on-the-ground experience (decades, not just years) working & living in Peru.

To reiterate, Magma Silver is a high risk junior, but it truly has blue-sky potential, especially if the Ag price remains above $70/oz, or climbs back above $80-$90-$100/oz… (Ag hit $81 intraday on April 15th). No, Magma doesn’t need $70+ an ounce, but it certainly doesn’t hurt!

Drilling for this C$16M company could be quite impactful. Readers should consider taking a closer look at Magma Silver (TSX-v: MGMA) / (OTCQB: MAGMF). Please see the Company’s latest corporate presentation.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about Magma Silver, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Magma Silver are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Magma Silver was an advertiser on [ER] and Peter Epstein owned shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.