Table of Contents Show

Midstream Oil And Gas Equipment Market Size

Report Overview

The Global Midstream Oil And Gas Equipment Market size is expected to be worth around USD 70.4 Bn by 2033, from USD 28.4 Bn in 2023, growing at a CAGR of 9.5% during the forecast period from 2024 to 2033.

Midstream Oil & Gas Equipment refers to the infrastructure and technology used to transport, store, and process oil and gas after they are extracted from the ground but before they are refined or distributed to consumers.

This sector plays a crucial role in the oil and gas industry, linking upstream production (extraction) with downstream activities (refining and distribution). Midstream equipment includes pipelines, storage tanks, compressors, pumping stations, and gas processing plants. These assets are responsible for the safe and efficient movement of oil, natural gas, and natural gas liquids from production sites to refineries or distribution points.

Governments worldwide have enacted regulations to ensure the safety and environmental sustainability of midstream oil and gas operations. In the United States, the Federal Energy Regulatory Commission (FERC) enforces regulations related to pipeline safety, and in 2023, they increased inspection requirements for aging infrastructure, allocating USD 200 million in funding to support these efforts.

Similarly, in Europe, the European Union’s Energy Union policy has set targets for reducing carbon emissions from fossil fuel transportation, pushing midstream companies to adopt cleaner technologies and optimize their equipment for energy efficiency. These regulations are influencing how midstream companies operate and invest in new technologies.

Private and government investments in midstream infrastructure are also playing a significant role in shaping the sector. In 2023, global investments in pipeline expansion and gas storage facilities reached over USD 25 billion, with major players such as Mitsui & Co., Ltd. and Enbridge Inc. securing multi-million-dollar contracts to build and upgrade pipelines across North America, Asia, and Europe. For instance, Enbridge announced a USD 4.5 billion investment in new pipelines and gas storage projects in Canada, expected to increase capacity by 15% by 2025.

Additionally, midstream companies are actively pursuing acquisitions and partnerships to expand their geographical reach and technological capabilities. In early 2024, Carlyle Group acquired a 50% stake in a major U.S. natural gas storage facility, worth USD 1.3 billion, with plans for further expansion. These mergers and acquisitions are seen as essential for consolidating market share in a competitive sector, while also fostering innovation in more efficient transportation systems.

Innovation in midstream oil and gas equipment is another key factor shaping the market. The adoption of digital technologies like Internet of Things (IoT) sensors, AI-driven predictive maintenance tools, and automated pipeline monitoring systems has grown significantly.

In 2023, the adoption of smart pipeline monitoring systems rose by 12%, with companies investing USD 3.4 billion in IoT solutions to reduce operational costs and improve safety. The integration of AI and machine learning is expected to further reduce operational downtime and enhance pipeline safety, with forecasts predicting that AI-based solutions will grow at a CAGR of 18% from 2024 to 2030.

Key Takeaways

Midstream Oil And Gas Equipment Market size is expected to be worth around USD 70.4 Bn by 2033, from USD 28.4 Bn in 2023, growing at a CAGR of 9.5%.

Actuator held a dominant market position, capturing more than a 28.2% share of the Midstream Oil & Gas Equipment Market.

Composite held a dominant market position, capturing more than a 28.1% share.

Flow Control held a dominant market position, capturing more than a 39.1% share.

Installation held a dominant market position, capturing more than a 39.1% share.

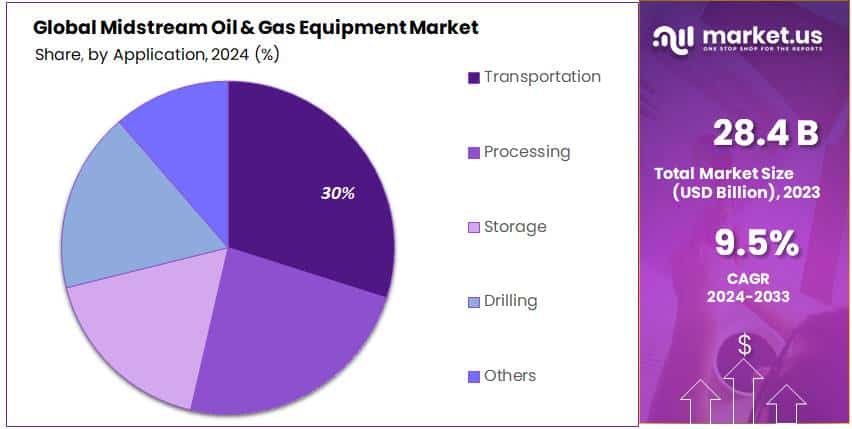

Transportation held a dominant market position, capturing more than a 29.1% share.

North America, the market is a dominant force, commanding a 38.4% share with a valuation of USD 10.9 billion.

By Type

In 2023, Actuator held a dominant market position, capturing more than a 28.2% share of the Midstream Oil & Gas Equipment Market. This growth can be attributed to the increasing demand for precision control systems in the transportation and processing of oil and gas. Actuators are critical in regulating the flow of oil and gas, which makes them essential for the smooth functioning of pipelines and processing facilities. Their versatility and ability to perform under high pressure conditions are key factors contributing to their market leadership.

The Compressor segment follows closely, holding a significant portion of the market. Compressors play an important role in transporting gas over long distances by maintaining pressure levels within pipelines. With the rise in global energy demand and the need for enhanced transportation infrastructure, the demand for compressors has grown steadily. In 2023, it captured a notable share, driven by its essential function in the industry.

Pipes also maintain a solid presence in the market. They are the backbone of midstream infrastructure, transporting crude oil and natural gas across vast distances. With the continued expansion of oil and gas networks, the demand for high-quality, durable pipelines has increased. As a result, the segment has been expanding, with growing investments in pipeline construction and maintenance.

The Pump segment, another key player in the midstream oil and gas equipment market, plays a pivotal role in moving liquids and gases throughout pipelines. The rising global consumption of oil and gas has driven growth in this segment, as pumps are critical for ensuring smooth and efficient operation.

Valves, crucial for controlling and directing the flow of fluids in pipelines and plants, also contribute significantly to the midstream sector. Valves’ reliability in high-pressure conditions, along with the expansion of oil and gas transportation networks, has helped them capture a substantial share of the market.

By Material

In 2023, Composite held a dominant market position, capturing more than a 28.1% share of the midstream oil & gas equipment market. The use of composite materials in midstream operations has been driven by their high strength-to-weight ratio, corrosion resistance, and ability to withstand extreme temperatures and pressures.

These properties make composites particularly suited for pipeline coatings, valves, and other critical equipment, where durability and long service life are essential. As the industry continues to prioritize efficiency and sustainability, composite materials are increasingly seen as a cost-effective solution for reducing maintenance needs and extending asset life. Additionally, the ability to integrate lightweight composite materials into infrastructure is seen as a major advantage in remote or offshore locations, where logistics and transportation can be challenging.

Plastic materials also play a significant role in the midstream oil & gas market, holding a substantial share in 2023. Plastic-based equipment, such as piping and fittings, are valued for their lightweight nature, corrosion resistance, and lower production costs compared to metals. Plastic materials like PVC, PE, and PTFE are commonly used in applications requiring resistance to chemicals, acids, and oils, making them ideal for transporting fluids and gases through pipelines.

The demand for plastic materials is expected to remain strong, driven by ongoing advancements in polymer technology, which allow for better performance in harsh environmental conditions. The cost-effective nature of plastic materials further solidifies their presence in the market, especially in regions with budget constraints or emerging markets.

Steel, a traditional material in the oil & gas industry, remains a key segment of the midstream market, though its share showed a decline in 2023. Steel’s strength, durability, and availability make it a preferred choice for many pipeline and storage tank applications, especially for long-distance transportation and high-pressure systems.

Despite facing competition from lighter, more corrosion-resistant materials, steel continues to be used extensively in the construction of infrastructure like transmission pipelines, pressure vessels, and storage tanks. Innovations in steel coatings and alloy compositions are helping the material maintain its place in the market, as it can now better withstand the corrosive environments typical of midstream oil and gas operations.

By Functionality

In 2023, Flow Control held a dominant market position, capturing more than a 39.1% share of the midstream oil & gas equipment market. Flow control systems, including valves, regulators, and meters, are critical in managing the movement of oil and gas through pipelines, storage tanks, and processing facilities.

The increased demand for flow control technologies is largely driven by the need for efficient resource management, safety, and maintaining optimal operating conditions in pipelines. As global oil and gas production ramps up, particularly in remote and offshore regions, the demand for advanced flow control systems is expected to continue growing. In 2024, the share of flow control is projected to maintain its lead, driven by innovations in automation and digitalization that further enhance operational efficiency and safety standards.

Pressure Management, the second-largest segment, accounted for a significant portion of the market in 2023. Pressure management equipment, such as regulators, relief valves, and blowout preventers, is essential for maintaining the integrity of pipelines and facilities by controlling the pressure levels of transported oil and gas.

With increasing regulatory focus on safety standards, particularly in high-pressure systems, the market for pressure management solutions is expected to see consistent growth. The pressure management segment is anticipated to grow at a steady pace through 2024, with demand surging in regions experiencing higher levels of exploration and production activities, including deepwater drilling and shale oil extraction.

Temperature Regulation systems, which include heaters, coolers, and thermal valves, are crucial in ensuring that oil and gas remain at the optimal temperatures for flow and processing. In 2023, temperature regulation held a smaller market share compared to flow control and pressure management, but its role is becoming more important as the industry shifts toward more complex infrastructure and deeper resource extraction methods.

With the rise in high-temperature and high-pressure environments in oil and gas fields, particularly in offshore and Arctic regions, the need for effective temperature regulation technologies is set to increase. The market share of this segment is projected to grow steadily in 2024, with advancements in materials and more efficient thermal management solutions supporting this trend.

Vibration Control, while a smaller segment in 2023, plays an increasingly vital role in the midstream market. Equipment such as dampers, vibration isolators, and supports are essential for maintaining the structural integrity of pipelines and preventing fatigue-related failures.

As pipelines and equipment are exposed to varying degrees of vibration from transportation and pressure fluctuations, the demand for vibration control technologies is growing, particularly in regions with seismic activity or in offshore platforms. This segment is expected to experience moderate growth through 2024, driven by ongoing efforts to improve the longevity and safety of pipeline infrastructure.

By Service

In 2023, Installation held a dominant market position, capturing more than a 39.1% share of the midstream oil & gas equipment services market. Installation services are essential for the setup and commissioning of new oil and gas infrastructure, including pipelines, compressors, and storage facilities. The growing demand for oil and gas, especially in emerging markets and offshore drilling projects, is driving the need for large-scale installation projects.

As exploration and production activities expand into new territories, especially deepwater and remote regions, the installation segment is expected to maintain its leadership position in 2024. This will be fueled by the increasing complexity of equipment and infrastructure, requiring specialized knowledge and resources for safe and efficient installation.

Maintenance services also represent a significant portion of the market, contributing to the long-term performance and reliability of midstream oil and gas systems. In 2023, the maintenance segment saw steady growth, holding a strong market share as operators focus on minimizing downtime and optimizing asset life.

Routine maintenance, including inspections, repairs, and system checks, is vital for preventing costly disruptions and ensuring compliance with industry standards. The need for maintenance services is expected to rise in 2024 as aging infrastructure requires more frequent attention and as new, more advanced equipment comes online, increasing the complexity of maintenance needs.

By Application

In 2023, Transportation held a dominant market position, capturing more than a 29.1% share of the midstream oil & gas equipment market. The transportation of oil and gas through pipelines, tankers, and rail is the backbone of the midstream sector, as it ensures that energy resources reach refineries, storage facilities, and end consumers efficiently. With the increasing demand for oil and gas globally, especially in Asia and North America, the need for robust and reliable transportation systems has only grown.

The ongoing expansion of pipeline networks, along with the rise of alternative transportation methods like rail and maritime shipping, has contributed to the segment’s strong performance. In 2024, transportation is expected to maintain its leadership, with further growth driven by the need to transport oil from newly discovered reserves and remote locations to key industrial hubs.

Processing, the second-largest segment, accounted for a significant share in 2023 as well. The processing of raw oil and gas into usable products, such as refined oil, natural gas liquids (NGLs), and liquefied natural gas (LNG), plays a vital role in the midstream value chain.

With technological advancements improving processing efficiency and enabling better separation and refinement of resources, the demand for processing equipment is forecast to rise steadily through 2024. As production ramps up, especially in unconventional plays and offshore fields, midstream players are increasingly investing in advanced processing technologies to handle the growing volumes of crude and gas.

Storage, which involves the safe and secure holding of oil and gas products before transportation or further processing, is another key area of focus. In 2023, the storage segment experienced steady demand due to fluctuations in global supply and demand, as well as the need for strategic reserves. Storage facilities, including tank farms and underground caverns, are critical for stabilizing the supply chain and mitigating disruptions. In 2024, storage is expected to see moderate growth, with investments being made in expanding capacity and improving storage efficiency in response to global supply chain challenges.

Drilling, though essential for the upstream oil and gas sector, contributes less to the midstream market but remains a key application area. In 2023, drilling-related equipment and services within the midstream sector accounted for a smaller portion of the market, mainly due to the fact that drilling is primarily a function of the upstream industry.

However, drilling equipment, such as wellhead systems and blowout preventers, is integral to the construction of wells and pipelines, which ultimately supports midstream operations. As exploration and production activities grow in challenging environments, particularly offshore and in deepwater locations, drilling-related equipment and services are expected to see gradual increases in demand in 2024.

Key Market Segments

By Type

Actuator

Compressor

Pipe

Pump

Valve

Others

By Material

Composite

Plastic

Steel

Others

By Functionality

Flow Control

Pressure Management

Temperature Regulation

Vibration Control

Others

By Service

Installation

Maintenance

Upgrades

By Application

Drilling

Processing

Storage

Transportation

Others

Drivers

Increasing Global Energy Demand

One of the major driving factors for the Midstream Oil & Gas Equipment market is the increasing global demand for energy. This demand is being propelled by population growth, urbanization, and industrialization, particularly in developing regions like Asia, Africa, and the Middle East.

According to the International Energy Agency (IEA), global energy demand is projected to increase by 12% between 2023 and 2028, reaching an estimated 692 exajoules by 2028, up from 617 exajoules in 2023. This increase in demand for energy directly correlates with the need for more efficient midstream infrastructure, including pipelines, storage tanks, and transportation systems.

In 2023, global oil demand reached approximately 102 million barrels per day (MMbpd), according to the IEA, with expectations to rise to 104.4 MMbpd in 2024. Similarly, the demand for natural gas is projected to increase by 2% per year between 2023 and 2024, driven by its use in electricity generation, heating, and industrial applications.

As a result, midstream oil and gas companies are investing heavily in expanding their infrastructure and upgrading existing systems to handle the growing volumes of oil, gas, and natural gas liquids (NGLs) being produced.

According to the U.S. Energy Information Administration (EIA), U.S. oil production in 2023 reached 12.4 million barrels per day (MMbpd) and is expected to reach 12.9 MMbpd in 2024, fueled by the continued growth of shale oil production.

The increasing focus on energy security, especially in Europe and Asia, has further highlighted the importance of reliable midstream infrastructure. Countries are diversifying their energy sources to reduce dependence on a single supplier, leading to higher investments in both domestic and international oil and gas transportation networks.

The European Union, for instance, has increased its investments in pipeline and LNG infrastructure, with the European Commission announcing a €10 billion budget for energy infrastructure development under the Connecting Europe Facility (CEF) program, aiming to ensure a more resilient and diversified energy supply.

Restraints

Environmental and Regulatory Challenges

One of the major restraining factors for the Midstream Oil & Gas Equipment market is the increasing pressure from environmental regulations and the growing concern over climate change. Governments worldwide are tightening regulations to reduce carbon emissions and minimize the environmental impact of oil and gas operations. As global awareness of climate change rises, stricter environmental standards are being imposed on oil and gas companies, leading to challenges in compliance and higher operational costs for midstream infrastructure.

According to the International Energy Agency (IEA), the oil and gas sector accounted for approximately 42% of global CO2 emissions in 2023, with midstream operations—such as transportation and storage—contributing significantly to these emissions. This has prompted governments to enforce stricter emission regulations, including the introduction of carbon pricing and emissions reduction targets.

In Europe, for example, the European Union’s Green Deal aims to reduce net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. This policy directly affects midstream oil and gas equipment manufacturers and operators, who must adopt new technologies to comply with emission reduction goals.

In the United States, the Environmental Protection Agency (EPA) has implemented regulations that limit methane emissions from oil and gas operations. These rules, introduced in 2023, require companies to upgrade their infrastructure, such as pipeline seals and pressure control devices, to prevent leaks.

According to the EPA, the U.S. oil and gas sector emitted 1.2 million metric tons of methane in 2022, and the new regulations aim to cut this by up to 75% by 2025. The compliance costs associated with upgrading midstream equipment to meet these regulations are expected to be significant, which could restrain market growth.

Additionally, environmental concerns around oil spills, water contamination, and habitat disruption are forcing midstream companies to invest in more expensive, eco-friendly solutions. In 2023, the total cost of oil spills globally reached $3 billion, according to the International Tanker Owners Pollution Federation (ITOPF). This has led to increased investment in advanced monitoring and leak detection systems, further adding to the financial burden of midstream infrastructure.

The shift toward renewable energy sources also poses a long-term challenge. As countries transition to cleaner energy alternatives like wind, solar, and hydrogen, demand for fossil fuels is expected to plateau or even decline in the coming decades.

According to the IEA’s World Energy Outlook 2023, the share of oil in the global energy mix is expected to fall from 31% in 2023 to 27% by 2040. This shift away from fossil fuels could lead to reduced investment in new midstream oil and gas infrastructure, particularly in regions with aggressive clean energy policies.

Opportunity

Expansion of LNG Infrastructure

A significant growth opportunity for the Midstream Oil & Gas Equipment market lies in the expansion of Liquefied Natural Gas (LNG) infrastructure. As countries around the world seek to diversify their energy sources and reduce carbon emissions, LNG has become a key alternative to coal and oil, due to its lower carbon footprint.

The International Gas Union (IGU) reported that global LNG demand increased by 6.5% in 2023, reaching 398 million tonnes (MT), up from 373 MT in 2022. This growth trend is expected to continue, with LNG demand projected to rise at a (CAGR) of 4.2% between 2023 and 2028, driven by demand from Europe, Asia, and emerging markets.

According to the IEA, global LNG export capacity is expected to increase by more than 25% between 2023 and 2026, with several new projects under development, particularly in the United States, Qatar, and Australia. In 2023, the U.S. alone became the largest exporter of LNG, surpassing Qatar, with exports reaching approximately 85 MT, a significant increase from 78 MT in 2022. By 2024, U.S. LNG exports are projected to surpass 90 MT, further driving demand for midstream equipment tailored for LNG transportation, storage, and liquefaction.

In addition to growth in export markets, LNG consumption is rising rapidly in regions like Europe, where nations are shifting from Russian gas to more reliable sources of supply. The European Union (EU) has aggressively pursued energy diversification strategies, with LNG playing a critical role in this transition. In 2023, the EU imported 78.5 MT of LNG, a 40% increase from the previous year, largely driven by reduced pipeline imports from Russia. This shift is expected to continue, as the EU aims to increase LNG imports by another 20% by 2025.

This rapid growth in LNG infrastructure presents significant opportunities for midstream oil and gas equipment manufacturers to provide specialized equipment such as cryogenic storage tanks, LNG pumps, and insulated pipelines, as well as advanced systems for the liquefaction and regasification processes. Moreover, technological advancements in liquefaction and regasification are enhancing the efficiency and environmental sustainability of LNG operations, further driving demand for new, more advanced midstream equipment.

Trends

Digitalization and Automation in Midstream Oil & Gas Equipment

A major trend shaping the midstream oil & gas equipment market is the increasing adoption of digitalization and automation technologies. The push towards digitizing midstream operations is largely driven by the need to improve efficiency, reduce costs, and enhance safety in an increasingly complex and regulated industry.

According to the International Energy Agency (IEA), digitalization in the oil and gas sector could generate up to $1.6 trillion in cumulative value between 2023 and 2025, driven by improvements in operational efficiency, asset performance, and predictive maintenance.

In 2023, the adoption of automation technologies such as advanced robotics, drones, and artificial intelligence (AI) has gained significant momentum in the midstream sector. These technologies are being integrated into key equipment systems, including pipeline monitoring, leak detection, and storage management.

For instance, smart pipeline systems equipped with sensors and real-time data analytics are being deployed to detect leaks and potential risks before they escalate into significant problems. This shift towards automated systems has led to reduced downtime, lower operational costs, and improved safety performance, which are crucial in the high-risk oil and gas industry.

In 2024, the trend of automation is expected to intensify, especially with the rise of digital twins and predictive maintenance systems. Digital twins, which create virtual replicas of physical assets, are becoming widely used for real-time monitoring and optimization of midstream equipment. This growth is driven by the increased need for predictive insights and real-time operational data to reduce risks and optimize asset utilization.

Furthermore, the integration of AI and machine learning (ML) into midstream operations has enabled companies to forecast demand, optimize resource distribution, and improve pipeline maintenance schedules. These technologies not only enhance operational efficiency but also significantly reduce costs by minimizing the need for manual inspections and maintenance checks.

The trend toward digitalization is also bolstered by the growing demand for environmental sustainability. As governments and regulatory bodies impose stricter environmental guidelines, digital tools that enable better monitoring of emissions and energy consumption are becoming essential. In 2023, global spending on digital solutions aimed at improving sustainability in the oil and gas sector reached approximately $5.6 billion, with the trend expected to rise further in 2024. This focus on sustainable operations is expected to drive the adoption of more advanced digital solutions that monitor emissions, manage energy consumption, and optimize environmental compliance.

Regional Analysis

In North America, the market is a dominant force, commanding a 38.4% share with a valuation of USD 10.9 billion. This region benefits from advanced extraction technologies, extensive pipeline infrastructure, and robust investments in both conventional and unconventional energy sources. The U.S. and Canada are pivotal in driving innovation and efficiency in equipment standards due to their mature oil and gas sectors and stringent environmental regulations.

Europe, while a smaller market, focuses on the modernization of aging infrastructure and the integration of greener technologies. The emphasis is on compliance with increasingly strict regulations on emissions and environmental protection, driving demand for updated and efficient equipment. Key markets such as Norway, the UK, and Russia are spearheading these advancements, with significant investments in the North Sea and Eastern Europe.

The Asia Pacific region is witnessing rapid growth, fueled by increasing energy consumption and infrastructural developments. Emerging economies like China, India, and Southeast Asia are prioritizing the expansion of their gas pipeline networks and LNG import facilities, making this region highly lucrative for equipment suppliers. Technological advancements and strategic partnerships are pivotal in leveraging the burgeoning demand.

The Middle East and Africa, rich in conventional oil reserves, are focusing on optimizing existing frameworks and expanding capacities. The Middle Eastern market is leveraging its strategic geographic positioning to enhance its export capabilities, with significant investments in pipeline and storage facilities. Africa is gradually moving towards stabilizing its infrastructure with international investments and technological transfer, though it remains a smaller player in the global arena.

Latin America, led by countries like Brazil and Mexico, is exploring deep-water reserves and unconventional resources, necessitating advanced equipment and technology. This region is poised for growth, contingent on political stability and regulatory reforms to attract foreign investments and technical expertise.

Key Regions and Countries

North America

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Key Players Analysis

In the midstream oil and gas equipment market, a diverse array of key players demonstrates the sector’s extensive scope, ranging from equipment manufacturers to service providers and multinational energy corporations.

Among them, industry giants like ABB Ltd. and General Electric Company stand out for their broad portfolios encompassing advanced automation, control systems, and innovative solutions that enhance operational efficiency and safety across midstream operations. Similarly, Emerson Electric Co. and Flowserve Corporation contribute significantly with their expertise in flow control equipment and services, vital for the effective management of oil and gas flows in pipelines and storage facilities.

Companies such as Baker Hughes Company and Caterpillar Inc. are pivotal in providing specialized machinery and technology for gas compression and power generation, which are crucial for ensuring the reliability and efficiency of midstream operations.

Ariel Corporation, a leader in gas compressors, directly supports the sector’s need for high-performance compression solutions. On the service side, firms like Akin Gump Strauss Hauer & Feld LLP provide legal and regulatory insights that help navigate the complex landscape of the oil and gas industry, ensuring compliance and facilitating smooth operations.

Energy majors like BP PLC, Chevron Corporation, and Royal Dutch Shell PLC not only play crucial roles in the upstream sector but also significantly impact midstream activities through their investments in infrastructure and technology aimed at improving the efficiency and sustainability of transportation and storage operations.

Enbridge Inc. and EnLink Midstream LLC, primarily focused on midstream operations, manage extensive networks of pipelines and storage solutions, demonstrating the critical role of specialized infrastructure operators in the market.

These key players, together with firms like Sulzer Management Ltd. and Swagelok Company, which supply essential components and maintenance services, illustrate the interconnected nature of the midstream sector, underscoring its reliance on a wide range of technical and professional expertise to maintain and enhance the global supply chain of oil and gas.

Top Key Players

ABB Ltd.

Akin Gump Strauss Hauer & Feld LLP

Ariel Corporation

Baker Hughes Company

BP PLC

Caterpillar Inc.

Chevron Corporation

Elliott Group

Emerson Electric Co.

Enbridge Inc.

EnLink Midstream LLC

Flowserve Corporation

General Electric Company

Intertek Group PLC

Kimray, Inc

Royal Dutch Shell PLC

Sulzer Management Ltd.

Swagelok Company

Recent Developments

ABB focused on expanding its offerings in automation and real-time data monitoring systems for pipelines, which are crucial for optimizing performance and ensuring safety in midstream operations.

In 2023, Ariel Corporation continued to enhance its offerings in the midstream sector, focusing on providing equipment essential for the processing, transportation, and storage of natural gas.