Since 2021, two dozen economic studies have used Lithium (“Li“) carbonate prices ranging from US$18,000-$30,513/tonne, with a median of ~$23,500, driving a median post-tax IRR of ~26%. This does not include hard rock Li spodumene-only projects.

Many, if not most, projects now need $25,000+/t due to meaningful cost inflation from PEA/PFS/BFS studies dating back 1.5+ years. The world urgently needs all technically, logistically, environmentally sound projects, even higher cost ones.

Some are calling for up to US$42,500/t by next year, but who knows. Still, the writing’s on the wall — stationary battery storage demand for Li-ion batteries has meaningfully surprised to the upside.

Note, this is even before a massive roll-out of AI data centers, where power redundancy & back-up are routinely being delayed in an effort to become operational as quickly as possible.

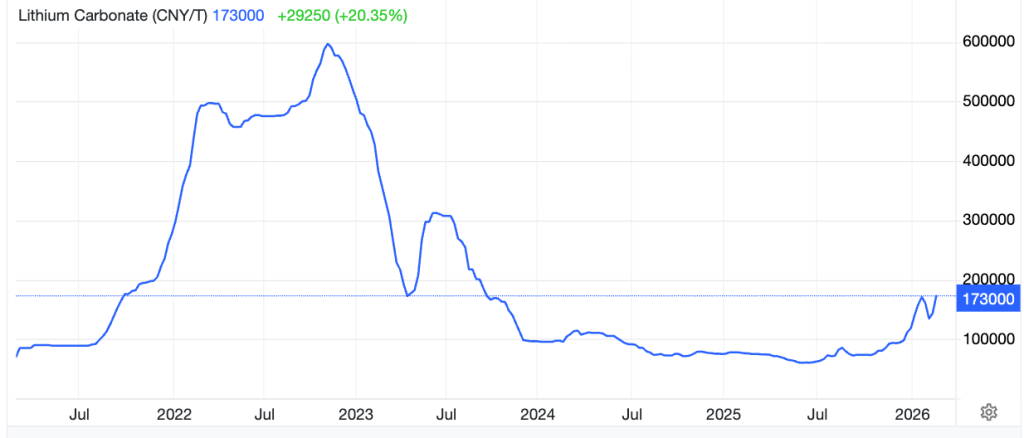

The battery-quality Li carbonate price in China is +189% from the low in July, 2025. The good news is that the current price is ~$25.0K/t (it touched ~$26.0K on Jan. 26th, and was $80K+ in 4th qtr. 2022!).

No, we’re not headed back to $80K, but $30-$35K could be a sweet spot, a level that’s possibly a bit higher than customers want, but clearly affordable for most end uses.

Lithium prices have staged a dramatic recovery, surging from under $9.0K/t in mid-2025 to ~$25.0K/t, reflecting a cyclical shift from moderate, and unsettling oversupply, to a tightening supply-demand balance and possibly shortfalls as soon as this year.

Supply is increasingly uncertain as situations like this pop up around the world…

FEB. 25th, Zimbabwe has suspended exports of all raw minerals & lithium concentrates with immediate effect, after the government alleged malpractices. The ban on exports will remain in place until further notice, and be applied to all minerals currently in transit.

Key drivers include,

Inventory drawdowns & policy momentum — Chinese converter & cathode inventories dropped to critically low levels after prolonged lean operations, catching the industry off-guard, and sparking aggressive restocking.

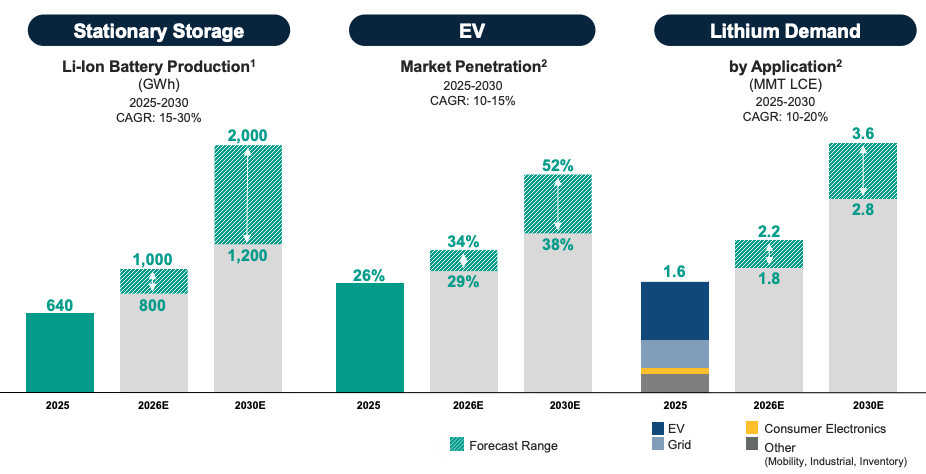

Demand rebound & product mix shift — Grid-scale Battery Energy Storage Systems (“BESS“) overtook EVs as the main growth driver. BESS is benefiting from rapid increases in Li commitments from tech giants for AI data centers.

Regarding demand growth from EVs vs. BESS, Albemarle Corp reported earnings on Feb. 11th, saying that demand from Li-ion batteries in EVs could grow +15%/yr through 2030, and BEES +25%-30%/yr. {see above from Albemarle}.

Some Li consultant groups like RK Equity see BESS growing faster than +40%/yr this year. If BESS is 30% of total LCE consumption in 2030, that could lead to demand for 3.8M tonnes of LCE, triple that of 2024.

Supply-side correction — The 2023-25 Li price crash prompted widespread cuts. High-cost mines & expansions were idled, major players like CATL suspended unprofitable output, Western projects faced delays, and Chinese regulators cracked down on inefficient mines.

Andy Leland of SC Insights predicts an average structural deficit of 80–85,000 tonnes/yr. through 2028. He believes prices could average $42.5K/t in this period.

A few years ago pundits expected sodium-ion, sodium-sulfur, vanadium flow, zinc-air, etc. to capture meaningful market share in BESS. Yet, very low Li prices allowed Li-ion to win the race, currently commanding ~90% market share.

A company I continue to like very much is Nevada Lithium Resources (“NLR”). Unlike many low-to-ultra-low grade brine/DLE projects in western Canada / U.S., it does not need $42.5K to thrive.

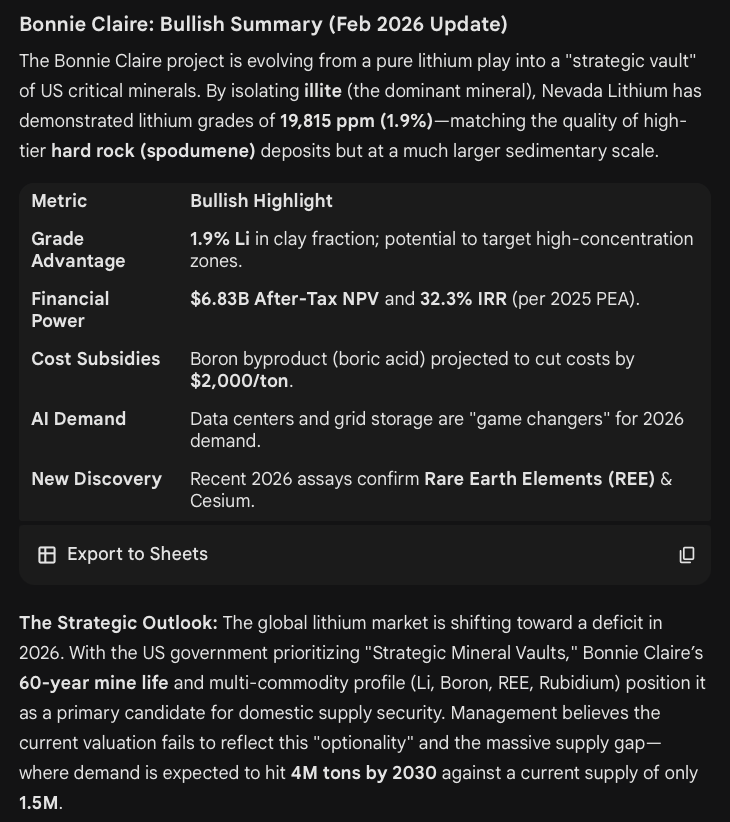

Last week, CEO Stephen Rentschler was featured on a webinar (summarized below). The update on isolating Li in illite is technical, (pockets of much higher grade suggest potential to selectively mine). Taken together with other news since the PEA was released the picture emerging is very attractive.

The Feb 18th PR reported on core analysis at Bonnie Claire showing Li hosted predominantly in illite clay, with grades up to ~19,800 ppm. This validates the high‑grade profile and enhances geological understanding.

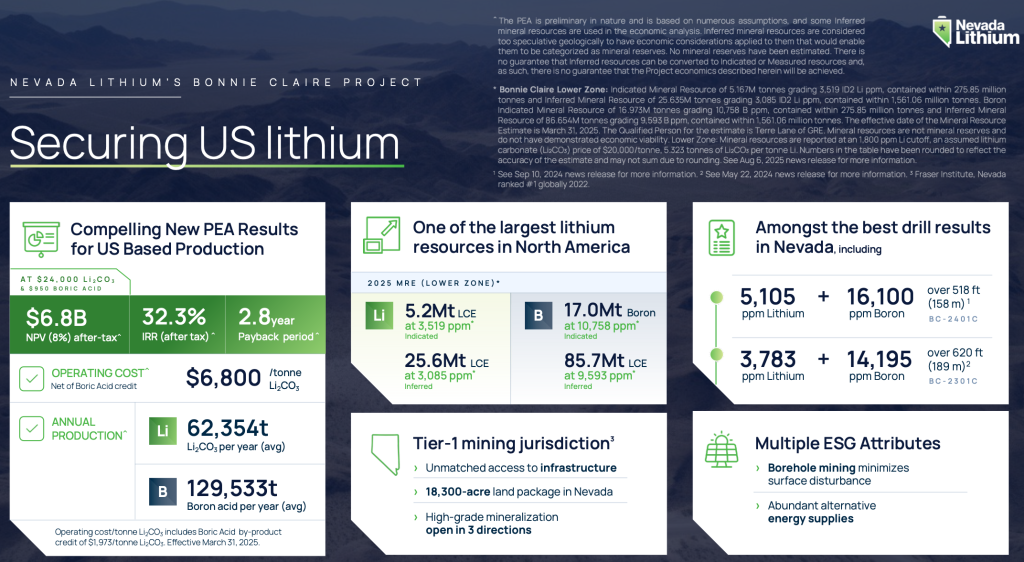

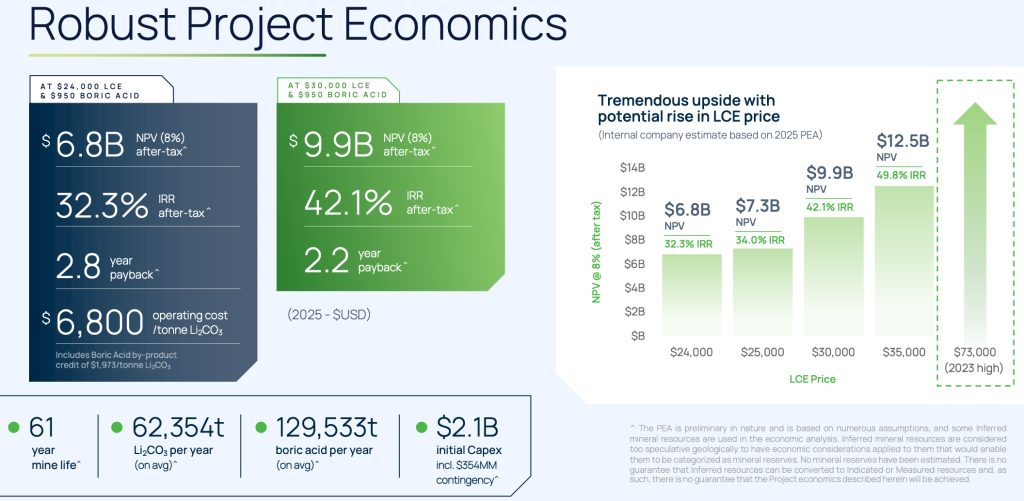

The Company’s operating cost in the recent PEA is $6,800/t (net of boric acid credits, but not cesium, rubidium or REEs, which are being studied). At a long-term assumed Li carbonate price of $24K/t, post-tax IRR is +32.3%.

The op-ex figure will likely climb in the coming years, but increases could be mitigated by additional by-product credits (more on that later). To avoid hundreds of words of Project description, please see the following image and review the latest corp. presentation.

A lot of eyes are on Lithium Americas’ Thacker Pass (“TP“) project in Nevada, expected to reach initial production within two years. Construction is well underway.

LAC, along with Albemarle, Standard Lithium & ioneer ltd, are poster boys for the future of U.S. Li production. After months of no news, ioneer recently raised US$50M to advance its Nevada Li/boron project.

ioneer expects to announce a strategic partner next quarter, attracting attention to Nevada Lithium. Production at ioneer is expected in 2029. Progress by LAC & ioneer is especially important as both have unconventional clay-hosted, (sedimentary) Li projects in Nevada.

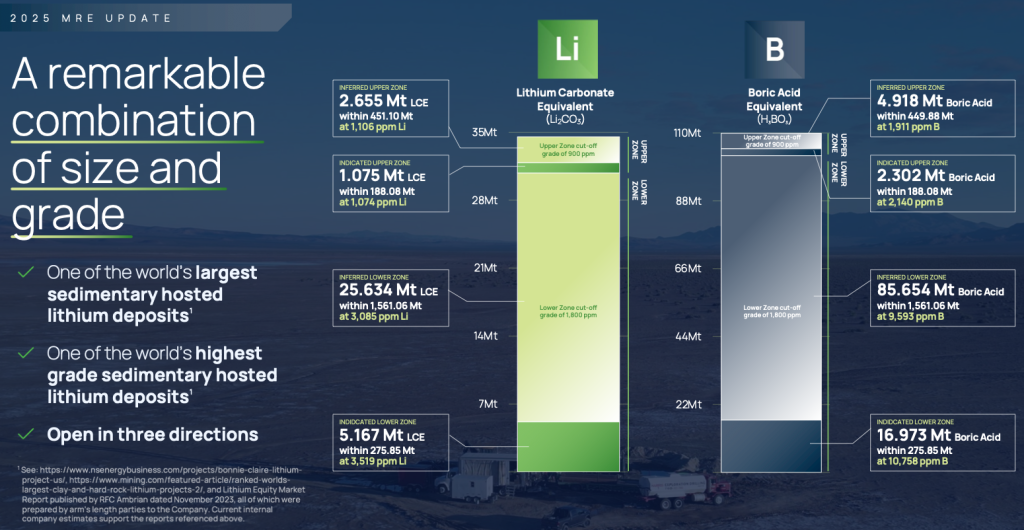

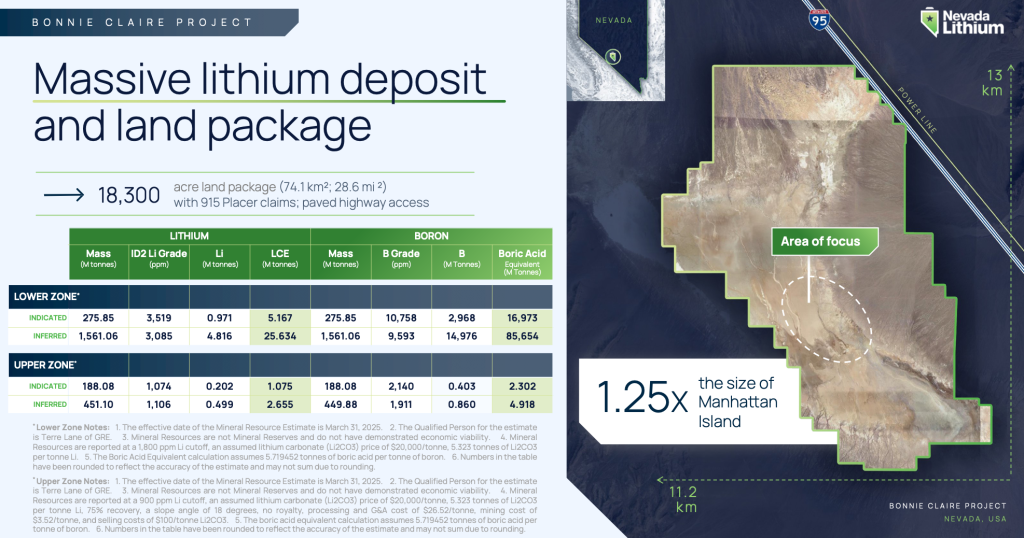

A defining characteristic of Nevada Lithium’s resource is its combination of high grade (3,150 ppm Li) for the lower portion of Bonnie Claire + massive endowment of 30.8M tonnes LCE (lower portion only).

How high a grade is that? By comparison, roughly a dozen western Canadian wastewater brine/DLE projects have grades in the 50-250 ppm Li range.

Note: 3,150 ppm is equal to a Li2O grade of ~0.68%, which would be very low for a hard rock project. However, Bonnie Claire is 10x-15x larger than most hard rock projects! And, compared to S. American brines, 3,150 ppm is 5x higher…

NLR is an asymmetric moonshot within the emerging U.S. sedimentary-lithium corridor. Bonnie Claire hosts one of the largest lithium resources in N. America. The strategic importance of critical materials like Li and boric acid produced domestically is high!

A large, relatively high-grade domestic Li deposit in Nevada is increasingly important and valuable to OEMs & policymakers who are laser-focused on securing a U.S.-centric battery supply chains.

Please note, this opportunity comes with significant risk, but risks are meaningfully lower at $25K Li than they were are sub-$9K. Clay-hosted Li extraction & processing are not yet plug-and-play at commercial scale, but neither are brine/DLE plays.

Both approaches are high risk, but the challenges are not insurmountable for either. I think the technical & regulatory hurdles facing dozens of much needed Li projects around the world will support a long-term price above $25K/t, with periods above $35K/t.

An important investment catalyst for NLR is Lithium Americas’ TP project targeting Phase 1 production in late 2027. TP will be the first large-scale commercial producer of battery-quality Li carbonate from Nevada clay-stone. ioneer could follow in 2029, and Nevada Lithium in the early 2030s.

If LAC is successful, which seems increasingly likely, it will serve as a proof-of-concept for the region. LAC’s doing the heavy lifting –> validating flowsheets, establishing permitting precedents, building out regional infrastructure & chemical processing.

Notably, TP & ioneer’s Rhyolite Ridge demonstrate financing pathways, including DOE loans, OEM partnerships, and strategic equity, that are templates for other Nevada developers. As roads, power, and supply chains are built, neighboring projects like Nevada Lithium’s will be de-risked.

If TP proves that Nevada clay-stone can play on a global scale, Bonnie Claire could be re-rated from speculative exploration to strategic acquisition target. Beyond Li & boron, Bonnie Claire shows potential for incremental value from cesium, rubidium, and select Rare Earth Elements (“REEs“).

Make no mistake, the REE grades are low by N. American (primary)-REE project standards, but *potentially* meaningful as by-products.

However, the key here is that there would be no additional mining costs because Nevada Lithium will be removing the same ore either way. Importantly, the race is on to improve REE separation technology globally, which will greatly benefit NLR.

Even modest recoveries, if deemed viable, could meaningfully improve project economics. Management, led by CEO/Dir. Stephen Rentschler, points out that prospective by-products remain in solution after lab test processing –> quite promising.

The presence of REEs, cesium & rubidium increases the odds of NLR obtaining U.S. gov’t grants, low-cost loans, research collaborations, tax breaks, etc.

Although not a sure thing — (gov’t financial assistance) — one thing is certain. $10s of billions in free-money grants will flow to U.S. mining, recycling, waste remediation and ore processing/refining initiatives. Will NLR be a recipient? Why not?

By the time the Company needs to secure the lion’s share of financing, LAC and ioneer will be in production, proving that Nevada clay-stone hosted Li (and other materials tied to the Li) is exploitable. That will make Nevada Lithium’s path far less uncertain.

In my view, gov’t/commercial debt funding for up to 75%-80% of Bonnie Claire could be available. If true, a free-money grant of just 5-10% of cap-ex would go a long way.

Then, selling a 10%-20% stake at the project level to a strategic investor could virtually guarantee that equity dilution would be manageable, especially on top of potentially obtaining partially pre-paid off-take agreements.

Note, these events are not expected in the near-term. Finally, a direct equity investment into NLR by the U.S. gov’t can’t be ruled out.

Admittedly, a lot has to go right for Nevada Lithium Resources, {see risk factors below) but I believe it’s a question of when, not if, (as long as the Li carb. price is north of $25K/t). Please revisit this prior article for a lot more commentary on risks.

In my view, the technical aspects and bore hole mining methods are more a question of costs than of scientific viability. The higher the Li price, the lower the risk that challenges are unsolvable with more time & investment dollars.

Bottom line? NLR is high risk, but carries substantial, commensurate, upside potential bolstered by the tailwinds of a strengthening Li price, and two much larger juniors entering production — IN NEVADA — in 2-3 years.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about Nevada Lithium Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Nevada Lithium are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Nevada Lithium was an advertiser on [ER] and Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.