Bullion has gained nearly 35% since January. Shares in gold miners are up by around the same amount. Despite their recent run, the miners appear a more attractive inflation hedge than the lustrous metal they produce.

Anyone acquainted with the industry might find that hard to believe. Historically, gold miners have offered remarkably poor protection against rising prices.

Over the past three decades the index of US consumer prices more than doubled and the price of gold rose sixfold. Over the same period, the Philadelphia Gold and Silver Index of listed miners climbed by about 40%. The mining benchmark remains well below its peak in 2011. Since that date US prices and bullion have risen by 33% and 55%, respectively.

Few industries have a more dismal record of allocating capital.

After the gold price took off in the early 2000s, miners pursued growth at any cost. They borrowed freely, splurged on new developments, and pushed up costs by extracting gold from low quality mines – what’s known in the business as low-grading. Debt levels at the four senior miners – Newmont, Barrick Gold, Agnico Eagle Mines and Kinross Gold – rose to an average 50% of net assets.

After the gold price dropped in 2011, the miners were left stranded. Barrick, the world’s largest miner at the time, announced some $23 billion of asset writedowns between 2012 and 2015.

Over the past decade the miners have put their problems behind them, says Caesar Bryan, portfolio manager of the Gabelli Gold Fund. They brought in new management teams who ran the companies to generate cash rather than maximise output. They restricted capital spending and strengthened their balance sheets.

Currently, average debt for the largest miners stands at 14% of net assets. Unfortunately, however, they hit a rough patch during the pandemic when labour shortages and difficulties in sourcing mining equipment pushed up costs. Once again, their stock prices dropped sharply.

Having underperformed since time immemorial, gold miners are viewed with distrust – even by industry insiders. Therein, lies the opportunity, suggests Bryan, quoting an astute epithet from investment strategist Don Coxe: “The most exciting returns are to be had from an asset class where those who know it best, love it least, because they have been hurt the most.”

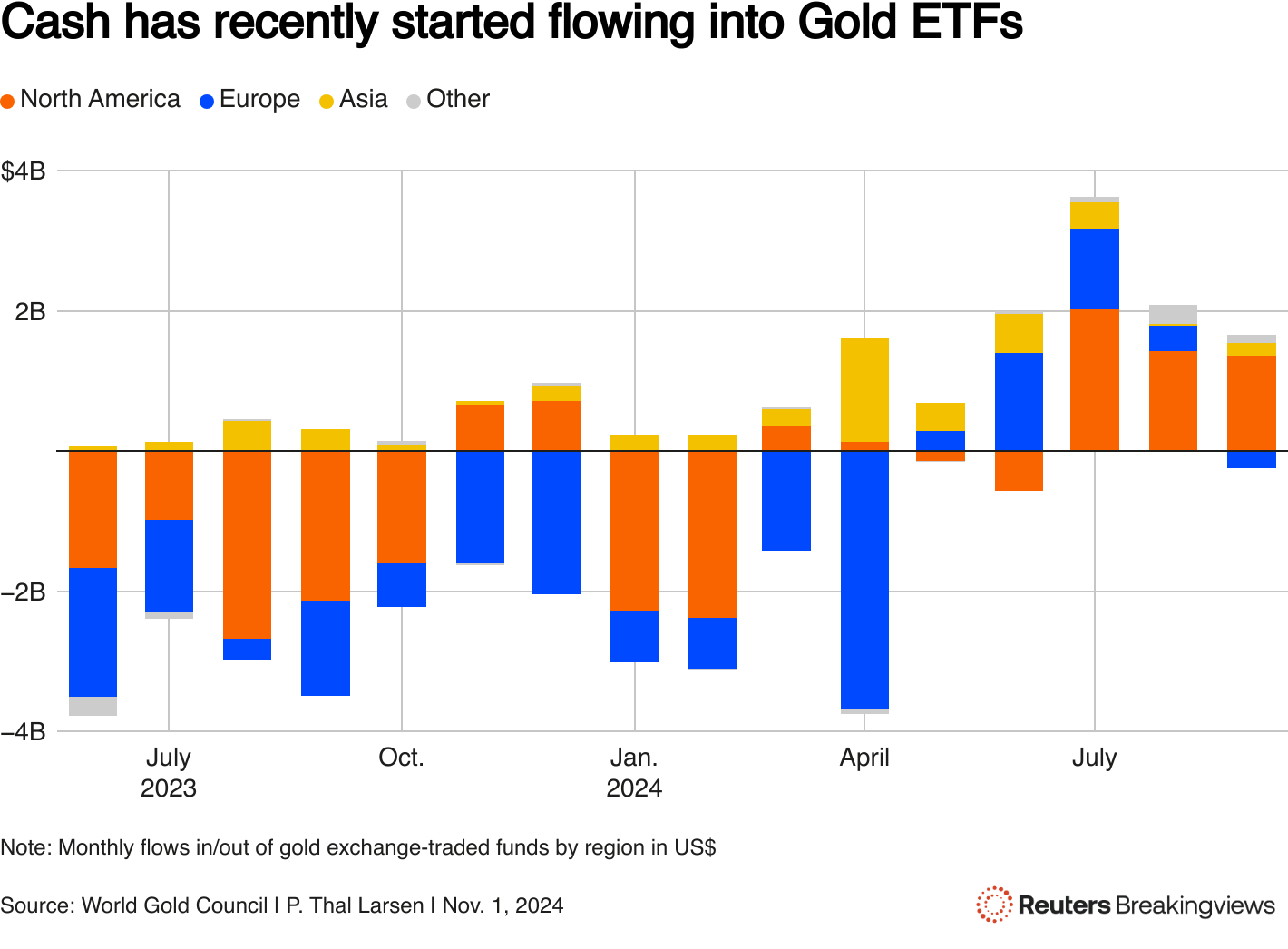

Gold miners may be doing well now but it does not feel like a genuine bull market to Bryan, who has been covering them since 1987. Exchange-traded funds tracking gold, and the VanEck Gold Miners ETF, have experienced regular outflows.

The mood of attendees at the Gold Forum Americas, the world’s largest gathering of precious metals investors, held this September in Denver, Colorado, was subdued. They were clearly frustrated by the continued underperformance of gold mining shares relative to bullion – though the equities have since caught up.

A column chart showing monthly flows in/out of gold exchange-traded funds by region in USD

A column chart showing monthly flows in/out of gold exchange-traded funds by region in USD

Gold miners are generating cash, boosting dividends and announcing plans to buy back shares. But they still look cheap on most valuation metrics, Bryan maintains. Assuming the current spot price holds, he expects several intermediate gold miners – including Toronto-listed Endeavour Mining and Dundee Precious Metals – to generate free cash flow equivalent to 20% or more of their current market value.

Gold equities are also trading at historically depressed levels relative to their net asset values. This metric is arrived at by taking estimated reserves, subtracting mining costs and applying a 5% discount rate to the resulting cash flows. The calculation involves many questionable assumptions, but the key input – the forecast gold price – is conservative.

Mining analysts at investment banks are predicting that gold will fall back below $2,000 an ounce by 2028, according to Beacon Securities – a drop of nearly 30%. The gap between the spot price and the analysts’ forecast has never been larger.

What this means is that the miners’ net asset values are understated, says Stefan Rehder, founder and managing director of Value Intelligence Advisors, a Munich-based investment firm.

That’s not all. The miners’ reported reserves are also depressed by the bearish gold forecast used in the NAV calculation, since assets that cannot be profitably mined at or below the forecast price are excluded from reserves. At the end of 2023, Newmont assumed a price of $1,400 an ounce for calculating reserves. The company estimated that a $100 increase in the gold price would boost its reported reserves by 5%.

Having been burned so badly a decade ago, miners have maintained their capital discipline. The industry’s pessimistic gold prognosis discourages them from extracting lower grade ores.

“Whilst we are clearly in a phase of the capital cycle where miners are investing again, they are doing it in a very controlled and muted way compared to last time,” says Paul Kennedy, portfolio manager of the WS Ruffer Gold Fund.

The reason, Kennedy argues, is that “management teams are scarred by the experience of the last cycle and still try to define ‘growth’ broadly as ‘growth in cash flow’ rather than as growth in volume of ounces produced.”

Given that the stock market places such a low value on the miners’ reserves, it makes more sense for them to acquire competitors than develop new projects. Merger activity has picked up. Last year, Newmont acquired the large Australian miner Newcrest. In September, AngloGold Ashanti made a $2.5 billion offer for Centamin.

Gold mining deals can be fraught. Newmont’s 2019 takeover of Goldcorp did not turn out well. Last week, Newmont’s stock dropped after the company reported problems with some recently acquired Newcrest assets. Still, acquisitions are less risky than developing new mines.

Investor sentiment towards the barbarous relic may finally be turning. Gold bars are flying off the shelves at Costco. The World Gold Council reports that inflows into gold ETFs turned positive in the third quarter after twelve months of outflows.

The soaring gold price is feeding through into miners’ earnings. The fact that miners are available on handsome prospective cash flow yields provides investors with a margin of safety. If the bullion price holds up, shares in gold miners should be a lot higher.

(By Edward Chancellor; Editing by Peter Thal Larsen and Katrina Hamlin)