Stock image.

Silver ranks amongst one of the top-performing commodities on the market, with renewed investor interest and strong fundamentals driving prices up to their highest in 14 years.

Despite having recorded impressive gains of 28% this year and 21% the year prior, some analysts predict that the rally is only getting started, and the precious metal remains an attractive investment opportunity.

Citigroup recently upgraded its near-term silver price forecast to beyond $40 an ounce, citing a tightening supply and strengthening demand.

Sprott, in its mid-year outlook for silver, highlighted the years-long structural deficit and intensifying industrial demand as major factors to propel prices even higher.

Continued deficit

The firm, citing data from The Silver Institute and Metals Focus, says that 2025 will likely be the seventh consecutive year of global silver market deficit, which would maintain an upward pressure on prices.

Meanwhile, demand, especially from the energy sectors, is not slowing down. The metal is crucial to the technology needed to meet rising global electricity demand, including solar power, electric vehicles and electronics. Solar demand alone accounted for 17% of last year’s total, a threefold increase over the 5.6% from a decade ago.

Silver demand continues to outpace supply growth (2016-2025). Credit: Sprott

Exacerbating the problem is a shrinking mine supply. Industry data shows that global mine supply has declined by 7% since 2016, contributing to the prolonged structural deficit. It is estimated that the cumulative shortfall during 2021-2025 is almost 800 million oz., Sprott said.

A wild card for the silver market balance, according to Sprott, is a robust investment demand. The rise of silver exchange-traded products (ETPs) continues to impact silver demand significantly, as many silver ETPs are backed by actual silver stored in vaults, rendering it unavailable for industrial users, it noted.

In the first half of 2025, global silver-backed ETPs experienced significant net inflows, reaching 95 million

oz. According to the Silver Institute, since 2019, more than 1.1 billion oz. (market balance plus ETPs) have been drawn from “available mobile inventory.”

Favoured to gold

The Sprott report also emphasized silver’s rising prominence as a “safe haven” like gold during periods of high geopolitical tensions. However, in comparison to the yellow metal, silver presents a much more affordable, and potentially higher-growth, option to investors, it says.

According to Sprott analyst Maria Smirnova, silver remains “undervalued” relative to gold.

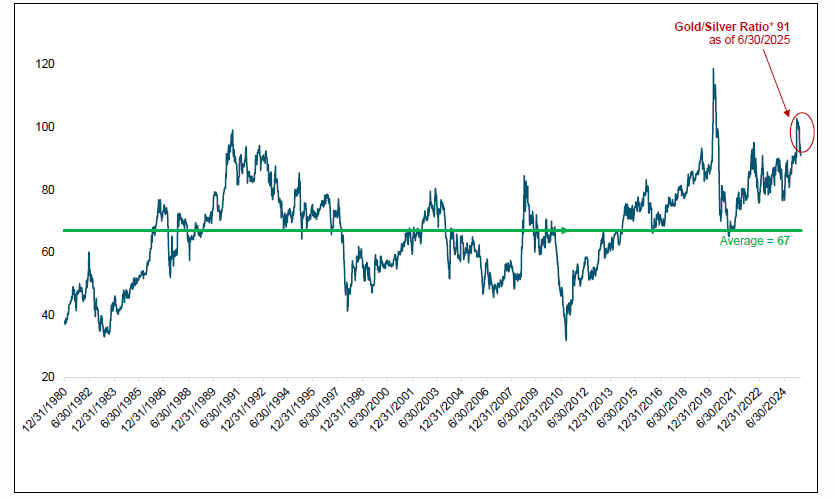

“On average, gold has historically been priced at 67x the price of silver. With the current ratio at 91, silver is selling at a strong discount to gold,” she said, adding that silver is mined at only 7:1 compared to gold.

Silver may be undervalued compared to gold (1980-2025). Credit: Sprott

Silver may be undervalued compared to gold (1980-2025). Credit: Sprott

Smirnova also points out that silver is primarily influenced by retail investment demand, while gold is controlled by central banks and sovereign entities.

“The available inventory of freely traded silver has been heavily diminished, making the metal more sensitive to incremental buying. Small increases in demand could now lead to disproportionately large increases in price,” she wrote.

“With less silver available for open-market trading, investor positioning has become a more decisive force

in price movements.” The current situation, she says, may be setting the stage for a possible “silver squeeze”.

In past precious metals bull markets, silver’s rally has been about 2x as large as gold, on average, Sprott’s report said.