The following views are that of Epstein Research, not necessarily those of the

management team or board of Silver Storm Mining.

Silver Storm Mining (TSX-v: SVRS) / (OTCQB: SVRSF) is a near-term producer (within a few months) in a prolific jurisdiction (Durango State, Mexico). Mexico is by far the largest silver (“Ag“) producing country, and Durango is one of the best jurisdictions (infrastructure, safety, mining history/culture, etc.).

In a meaningful vote of confidence, Samsung C&T signed a 2-yr concentrate off-take agreement with Silver Storm. Readers should note that several firms did extensive due diligence looking to partner with Silver Storm on the off-take.

This is a Company valued cheaply vs. peers on next year’s anticipated cash flow, AND, it has a second crown jewel asset, also in Durango, the giant, 100%-owned, early-stage San Diego project. First Majestic owns 19%, and Eric Sprott 12% of Silver Storm.

In late 2020, when the Ag price was a third of today’s $78/oz, San Diego was valued at up to C$100M as a single project in a predecessor company. I see no reason why San Diego alone isn’t worth at least C$304M now (keep reading to learn about that C$304M figure).

Yet, Silver Storm’s enterprise value {market cap + debt – cash} is ~C$406M. In my view, that means investors get the soon to be restarted La Parrilla complex at a large discount.

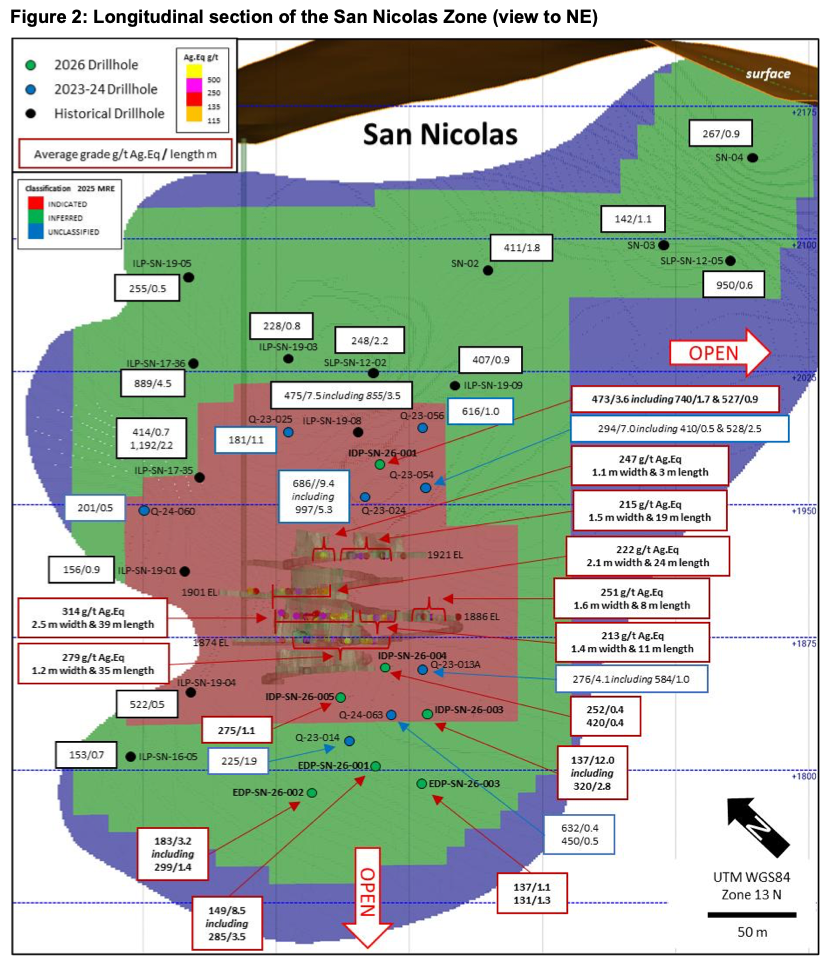

On April 21st management, led by CEO/Dir. Greg McKenzie, reported strong drill results, (see image above) extending mineralization both above/below the last producing stopes at the 100%-owned La Parrilla mining complex. La Parrilla is being restarted later this quarter.

How often have readers heard a narrative about near-term operations funding other company initiatives? See the new (excellent) corporate presentation.

With Ag at $78, the restart of the 100%-owned La Parrilla complex could truly move the needle in terms of providing investment capital to advance San Diego next year.

La Parrilla is a significant past producer (34M Ag Eq. ounces in total) with a mill that delivered (mostly) Ag, + zinc & lead from 2006 until 2019. When placed on care & maintenance, Ag was under $19/oz.

In its prime, production averaged ~3.5M Ag Eq. ounces/yr, with a high above 4.5M. Although profitable, the margin was never more than US$10/oz, at least not for extended periods.

At today’s levels, the margin next year could be > $55/oz. Think about that, Silver Storm could have the same or higher profitability than the average 46% EBIT margin of Microsoft, Nvidia, Google & Meta. Is Metals/Mining the new Tech?

With blockbuster drill results incl.; 14.6 m of 1,810 Ag Eq., and 13.1 m of 911 Ag Eq., La Parrilla’s resource was upgraded & expanded to ~27M Indicated (40%) & Inferred ounces (60%), at an average grade of ~265 g/t Ag Eq., which would be ~4.4 g/t Au Eq.

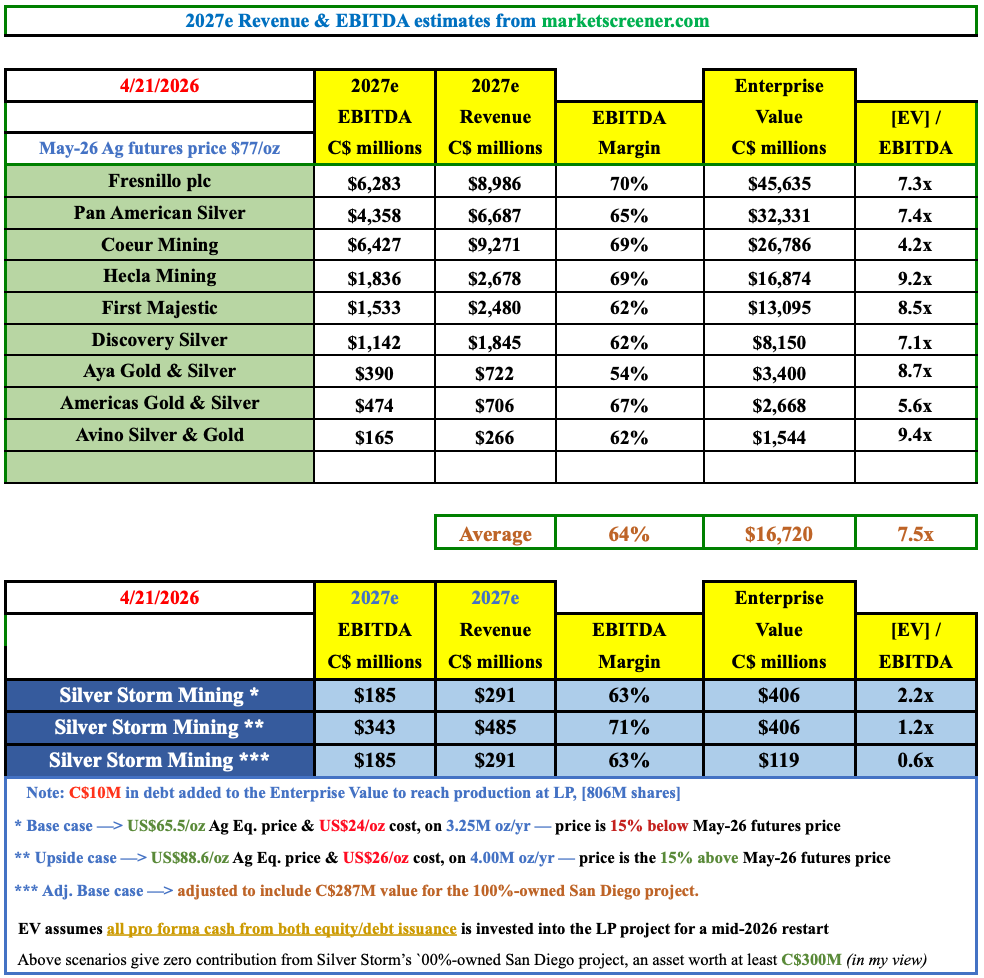

In the following chart, one can see producers valued at an average 7.5x 2027e EBITDA multiple. By comparison, Silver Storm is valued at just 2.2x, with zero credit for the San Diego asset.

Note: This undervaluation is substantial… Please take a moment to read the assumptions at bottom of table.

Assuming San Diego is worth C$304M, the adjusted EV/EBITDA metric is under 1. Granted, Silver Storm faces start-up (commissioning) & ramp-up risks, but *if* the restart goes reasonably as planned, there’s room for shares to run.

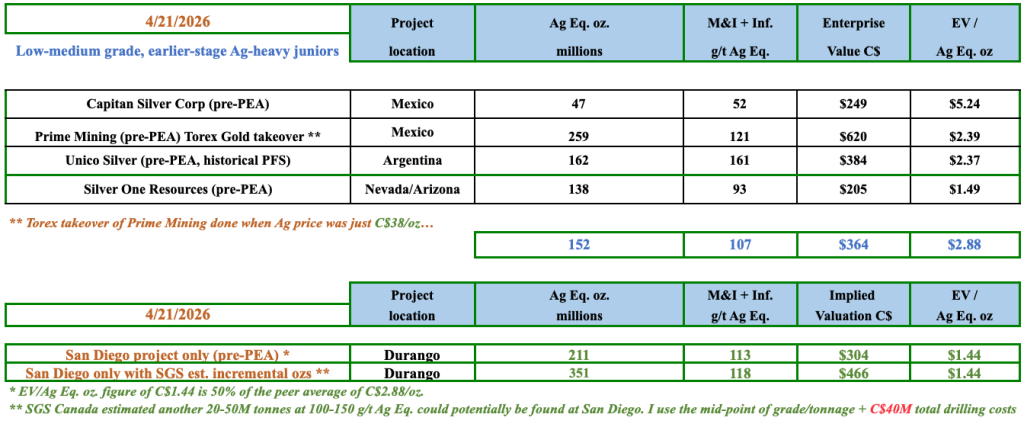

Where does that C$304M figure come from? I take 50% of the peer (early-stage, bulk tonnage, low-to-medium grade) average EV/Ag Eq. oz [C$2.88/oz], and apply it to San Diego’s 211M Ag Eq. ounces, see table below.

The stock traded as high as C$0.80 in January, vs. just C$0.51 today. Management recently reiterated a restart for this quarter. Management, led by CEO McKenzie, has prudently amassed a sizable cash cushion, with a prepaid off-take facility with Samsung, to de-risk La Parrilla.

Even if one thinks the valuation discount should be large due to pre-production risks, that reasoning ignores an important factor… San Diego is worth (in my opinion) ~C$300M. Why do I say that? Look at the following table (please read footnotes to table).

If one includes SGS Canada’s exploration target of 20-50M tonnes @ 100-150 g/t Ag Eq., (not a sure thing, timing unknown) the implied valuation would jump to C$466M (net of an estimated C$40M in exploration/drilling costs to find an incremental ~141M Ag Eq. ounces).

When SGS reported the 20-50M tonnes @ 100-150 g/t Ag Eq. in 2013, Ag was in the low $20s, so it was ignored. At $78/oz, it’s a different story… San Diego is early-stage, but has booked 211M Ag Eq. ounces (so far). At spot prices, over 80% of its economic value would come from Ag.

As mentioned, I estimate it might cost a total of C$40M in exploration & drilling expenses over several years to potentially delineate the midpoint of that SGS Canada exploration target. That is NOT a large sum assuming that La Parrilla is successfully ramped up in 2027.

La Parrilla’s mine life is ~7 years, which is pretty good, and it could reasonably be extended with further internally-funded drilling. CEO McKenzie’s drill campaigns at La Parrilla have been huge successes –> low-cost, highly efficient, blockbuster grades.

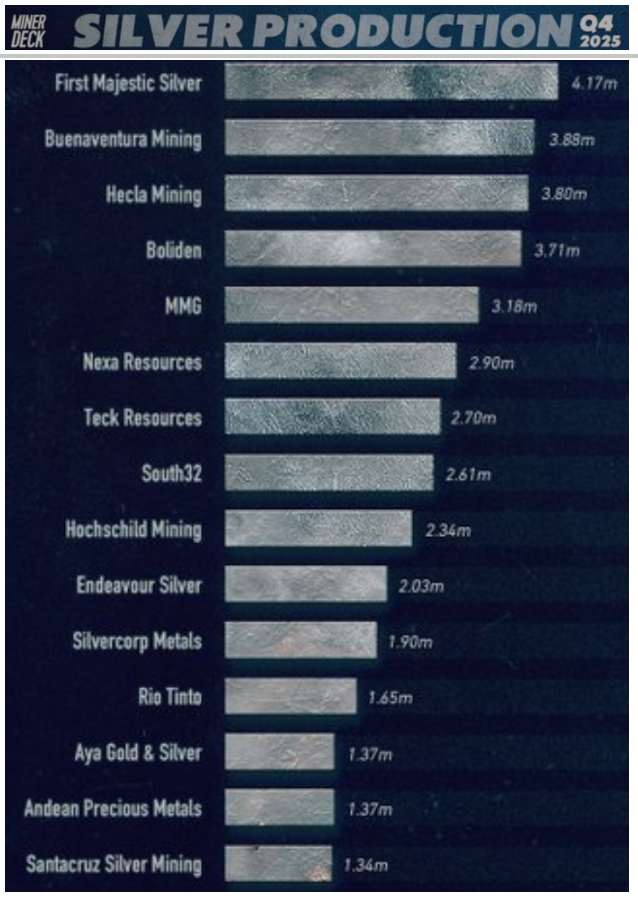

How significant a mine is La Parrilla vs. global peers? Fairly small, but significant. In the following table are 4th qtr 2025 production levels. I cut out the bigger names… La Parrilla’s production could approach a quarter of First Majestic’s or Hecla Mining’s.

It could be half Endeavour Silver’s or Silvercorp Metals’. It could be roughly 2/3’s of Aya Gold & Silver, Andean Precious Metals or Santacruz Silver Mining. Not in the table is fellow Durango Mexico player Avino Silver & Gold.

Avino has a market cap of C$1.6B, yet is guiding to 2.0M Ag Eq. ounces in 2026. Being in production, vs. near production, can make a big difference!

Imagine if a much larger precious metals company were to sign a JV on San Diego, perhaps paying Silver Storm C$100M for a 40% interest, and free-carrying them to commercial production?

Who might be interested in doing that? How about one the following… In my view, over a dozen producers should care. Note, this list is just Mexican-heavy names, U.S., Canadian & Australian focused producers would double or triple the number of prospective suitors.

To be clear, management does not necessarily need a partner for San Diego if it can largely self-fund development from 2027 on, a nice position to be in.

On a final note, although possibly not this year’s business, as these things take time, I imagine Silver Storm will one day be listed in the U.S. on the NYSE American or NASDAQ.

Metals/mining companies, including numerous Ag names like; First Majestic, Pan American Silver, Avino Silver & Gold, Americas Gold & Silver, Vizsla, Fortuna Mining, Endeavour Silver, and Contango Silver & Gold are dual-listed in Canada + the U.S.

Many newsletter writers like me say that a company they are championing could “re-rate” in the near future. With Silver Storm Mining there is a clear catalyst for this to happen… The restart of La Parrilla. CEO McKenzie said earlier this month that the restart is on track.

Therefore, in terms of events that can cause any given junior miner to re-rate, the risk around La Parrilla seems quite reasonable vs. the potential reward.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about Silver Storm Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Silver Storm Mining are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Silver Storm Mining was an advertiser on [ER] and Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.