Table of Contents Show

In our 2025 Market Outlook, we noted that the market was priced to perfection, trading at a relatively rare premium to fair value, and asked “Will it last?” We noted that positioning had become increasingly important and recommended investors to overweight value stocks as they were attractively valued. Growth stocks were significantly overvalued, trading at their highest premiums since the peak of the disruptive tech bubble in early 2021, and should be underweighted.

Since then, quarter to date through March 24, the Morningstar US Market Index has dropped 1.74%. Losses have been concentrated among those stocks that are most highly correlated with artificial intelligence. AI stocks are generally contained in the growth and core categories, which have sold off 3.79% and 3.52%, respectively. Conversely, undervalued value stocks have not only held their ground but also have risen 4.59%.

Dowload the Report: US Stock Market Outlook for Q2 2025

Valuations Drop to Bottom of Range We Consider Fairly Valued

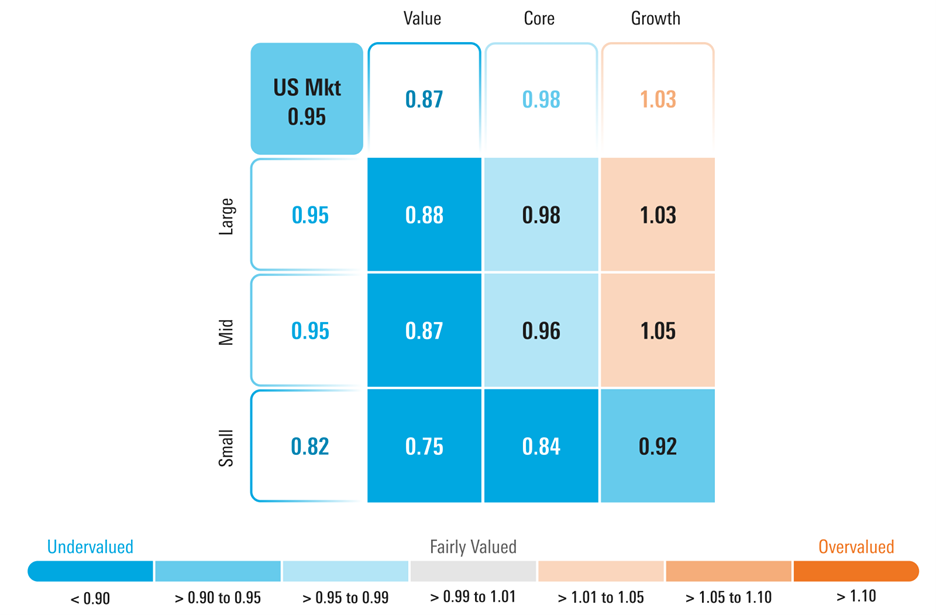

Based on a composite of our intrinsic valuations of the more than 700 stocks we cover that trade on US exchanges, as of March 24, 2025, we calculated that the US equity market was trading at a price/fair value estimate of 0.95. This represents a 5% discount to our fair value estimates. This places the market near the bottom of the range that we consider to be fairly valued.

Even After Outperforming, Value Remains Most Attractive

Over the course of the quarter, the rout across overvalued and overextended AI stocks has led to a swift downward reduction in our price/fair value metric for the growth category. Growth is now only trading at a 3% premium, whereas it was at 24% at the beginning of the year. While value stocks have posted a gain thus far, the category has become even more undervalued now, trading at a 13% discount to fair value. Over the course of the first quarter, our analyst team has increased our fair values on a wide swath of value stocks.

In our 2025 Outlook, we expected little price appreciation at the broad market index level. We noted that earnings needed to catch up to valuations, which we didn’t expect to occur until the second half of the year. With the market now trading at a discount, we now see some upside appreciation potential at the market level, yet, based on our valuations, by style we continue to advocate investors to—

Overweight: Value stocks, which trade at a 13% discount to fair value.Market weight: Core stocks, which trade at a 2% discount to fair value.Underweight: Growth stocks, which trade at a 3% premium to fair value.

By capitalization, we advocate for investors to—

Overweight: Small-cap stocks, which trade at an 18% discount to fair value.Underweight: Large-cap and mid-cap stocks, both of which trade at the same discount as the overall market.

Historically, small-cap stocks have performed best when the Fed is easing monetary policy, long-term interest rates are falling, and the economy is poised to begin rebounding. That does not appear to be the case in the near term, and while these stocks are undervalued, it may not be until later this year that they start to work. From a monetary policy point of view, the economics team from Morningstar Wealth Management expects the Fed will cut the federal-funds rate three times this year. While they forecast the rate of growth will slow sequentially through the end of the year, they forecast the economy will start to reaccelerate in early 2026. Long-term interest rates are currently trading at their 2025 projection level but should begin a multiyear downward trend later this year.

Rout Across AI Stocks Drives Downturn, Not Tariffs

Many media outlets have reported that tariffs are a main contributor to the market selloff, yet Morningstar’s John Rekenthaler writes Tariffs Aren’t the True Cause of the Markets’ Selloff and describes why he doesn’t see it that way. Our valuations and market action back up his assertion.

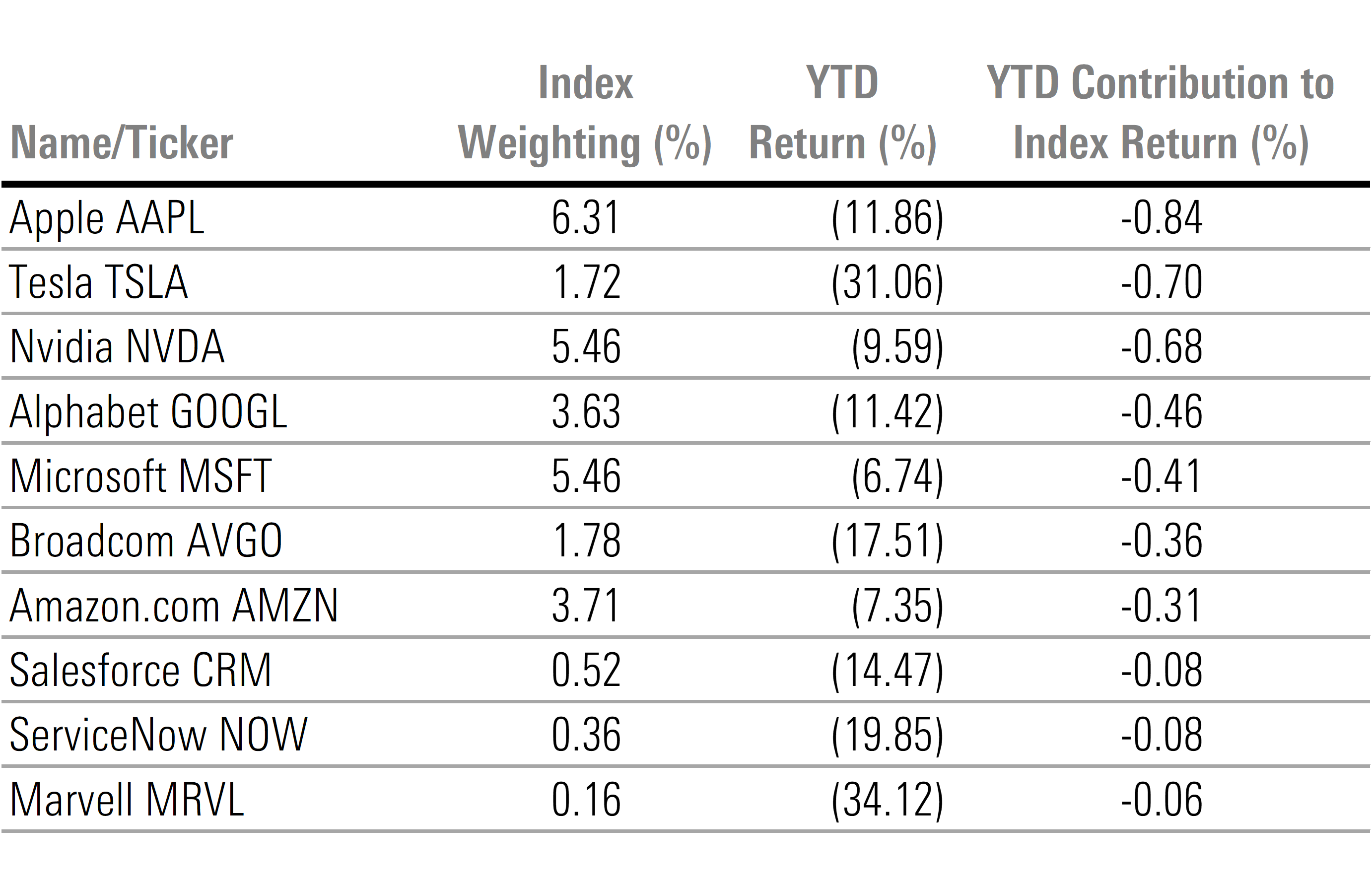

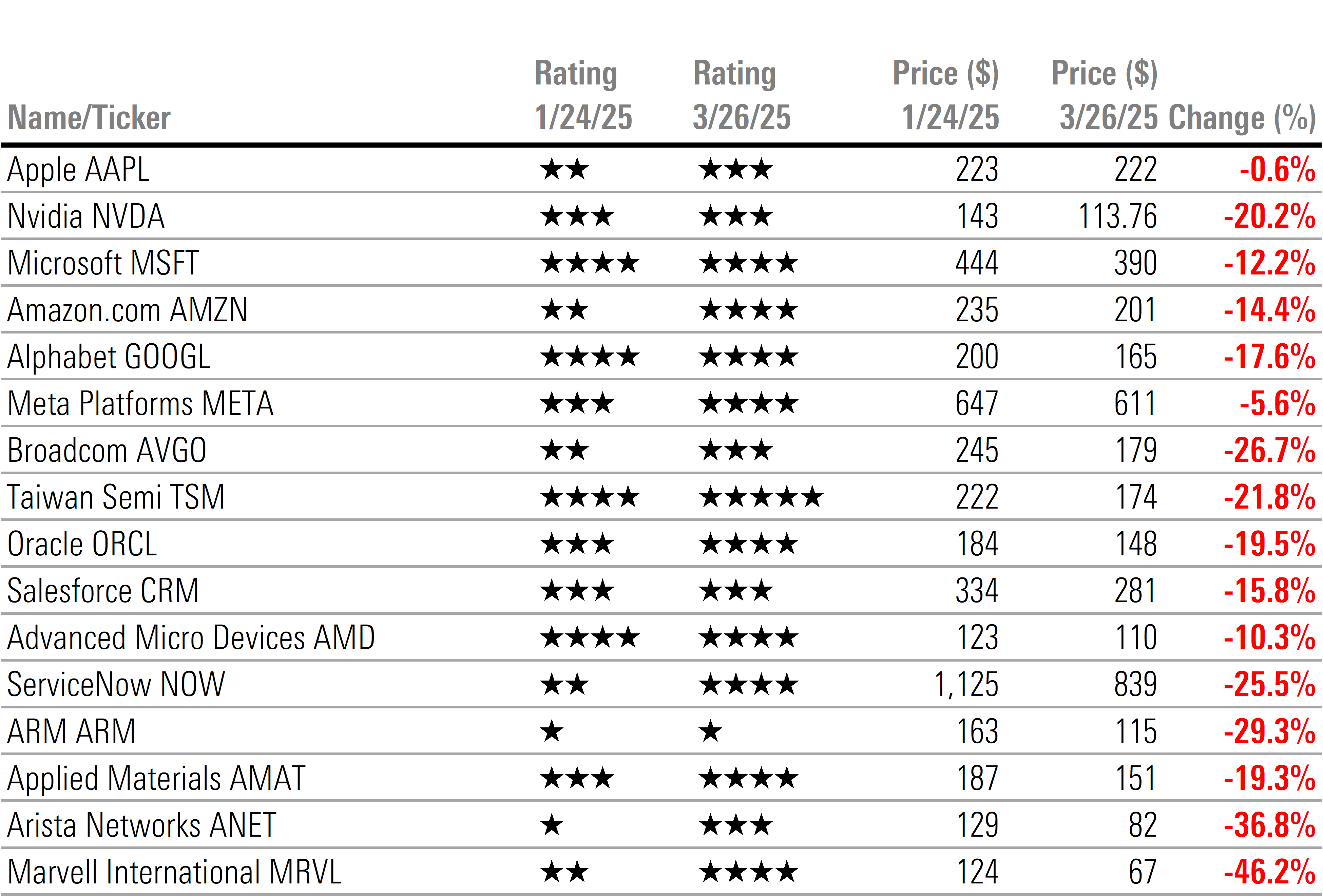

According to an attribution analysis of the Morningstar US Market Index, the negative return contribution from just 10 stocks is greater than the overall market selloff. Essentially, this means there were enough gains across the rest of the market to offset much of the losses on these stocks. Of these 10 stocks, seven of them were among the top 10 positive return contributions in 2024. Each in some fashion is correlated with the rapid development, growth, and utilization of artificial intelligence. The other three (Salesforce CRM, ServiceNow NOW, and Marvell MRVL) were also tied to the AI trade.

Are AI Stocks in a Bear Market?

The rout in AI stocks was not just limited to these 10, but a wide swath of stocks associated with artificial intelligence has been hit hard. Most AI stocks peaked just prior to DeepSeek hitting the headlines. Since that day, AI stocks have generally been on a downward trend.

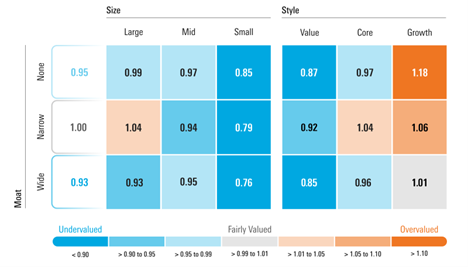

Wide-Moat Stocks Look Attractive for First Time in a While

Some of the largest mega-cap stocks that we rate with a wide moat such as Apple AAPL, Alphabet GOOGL, Amazon.com AMZN, Microsoft MSFT, and Nvidia NVDA have all sold off so far this year. As such, it has brought the overall category down to a 7% discount after starting the year at a 5% premium. Wide-moat stocks are now the most attractively valued. The last time they traded at this much of a discount or more was in fall 2023 as the markets were continuing to rebound off the 2022 bear market.

We see value across almost the entire range of wide-moat-rated stocks, except for growth. Even there, growth now trades at only a 1% premium, whereas it had traded at a 17% premium at the beginning of the year.

Now is a good time to scour your portfolio and increase the quality of your stock holdings by swapping into the stocks of companies with wide economic moats. Not only are wide-moat stocks trading at attractive margins of safety below their intrinsic valuation, but we think they also have less downside risk. Morningstar’s economics team is forecasting the rate of economic growth to slow each quarter sequentially over the course of this year, which in turn would lead to slower earnings growth. In such an environment, we expect companies that do not have long-term, durable competitive advantages would be more adversely affected to the downside.

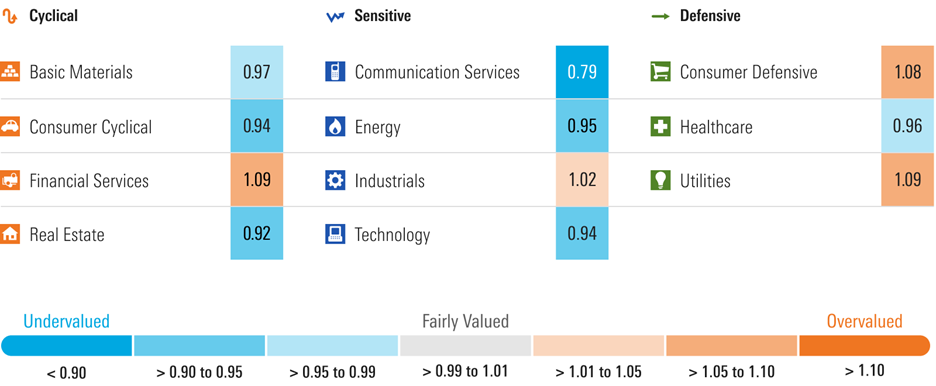

Notable Sector Valuation Changes: Communications Further Undervalued, Remaining Sectors Converging Toward Fair Value

Sector valuations tended to converge toward our fair values during the first quarter. The exception to this rule is the communications sector, which became further undervalued as both Alphabet and Meta META stock traded down, whereas we raised our fair value on both. Communications is now, once again, the most undervalued sector.

The greatest sector valuation change occurred in consumer cyclical, where the price/fair value fell to 0.94 from 1.19. The 31% decline in Tesla TSLA stock accounted for the preponderance of the change, followed by the 7% decline in Amazon. Tesla and Amazon were rated as 1 star and 2 stars, respectively, at the beginning of the year. The second-greatest valuation change occurred in the technology sector. The price/fair value fell to 0.94 from 1.07, with the bulk of the valuation changes resulting from the decline in AI stock prices.

Among the undervalued sectors that traded up, the price/fair value of the energy sector rose to 0.95 from 0.90 as stock prices rose across the sector. The price/fair value of the healthcare sector rose to 0.96 from 0.92. Eli Lilly LLY played a large part of the change, but stock prices generally rose across the sector.

Lastly, the utility sector became further overvalued, rising to 1.09 from 1.07. While we agree with the market that AI usage will lead to greater electricity demand, we think the market is pricing in too much growth, too fast.

Q2 2025 Market Outlook Webinar

Join me and Chief US Economist Preston Caldwell from Morningstar Investment Management on Tuesday, April 8, 2025, at 11 a.m. Central/Noon Eastern as we:

Break down our valuations and identify undervalued opportunities across categories, sectors, and stocks.Highlight investable long-term secular growth themes.Provide our forecasts for real US gross domestic product, inflation, and interest rates.Answer live audience questions.

Register here.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.