Table of Contents Show

The Stock Market Is Doing Something Witnessed Just Once Ever Before — and History Has a Clear Answer on What Happens Next

Key Points

-

The S&P 500 and Nasdaq Composite indexes have produced outstanding returns for investors over the last five years.

-

A huge portion of those gains has stemmed from expanding valuation multiples.

-

Investors need to look at additional context to understand what to expect.

-

10 stocks we like better than S&P 500 Index ›

Despite several ups and downs, the last five years have been nothing short of spectacular for stock investors. Since midyear 2020, the S&P 500 (SNPINDEX: ^GSPC) has produced a compound average total return of 17% per year, well above its historic average. The tech-heavy Nasdaq Composite (NASDAQINDEX: ^IXIC) has performed nearly as well, with a 16.5% average return.

Those returns come in spite of two massive declines of 19% or more in the S&P 500 and 23% or more in the Nasdaq, in 2022 and 2025. Today, both stock indices trade at new all-time highs.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

But one stock-market indicator suggests the indices could be in store for another substantial decline in price in the not-too-distant future. It just reached a level seen only once before in history, and it has a flawless track record of predicting significant downside in stock prices.

Image source: Getty Images.

The stock market looks historically expensive

The sticker price of a stock doesn’t tell you very much about whether or not it’s a good value. In order to judge whether a stock is expensive, most investors will look at its price-to-earnings (P/E) ratio. The P/E takes the share price and divides it by the earnings per share for the company. All things being equal, investors prefer to buy stocks when their P/E ratios are low.

But earnings for companies generally don’t grow in a straight line. Recessions, inflation, and all sorts of other economic pressures can impact earnings per share. And usually they affect the entire stock market, not just individual companies. That’s why economist Robert Shiller developed the cyclically adjusted price-to-earnings (CAPE) ratio.

The CAPE ratio takes into account the last ten years of earnings and adjusts each year for inflation. The standard P/E ratio only looks at one year of earnings. Looking at a much longer period evens out the impact of economic shocks like recessions.

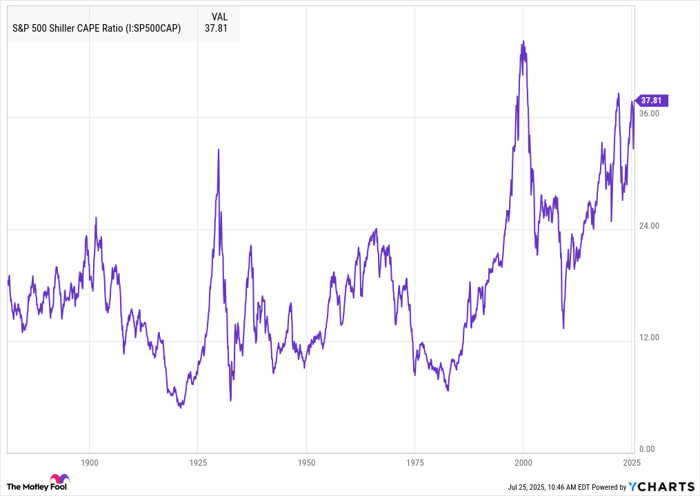

As of this writing, the S&P 500’s CAPE ratio has climbed to 38.8. That’s above the month-end peak from 2001, and the highest level we’ve ever seen outside of the dot-com bubble, when the ratio climbed above 40.

To give that valuation some more context, the S&P 500 (along with its earlier equivalents) has traded at an average CAPE ratio of 17.6 based on data going back to 1871. That multiple has climbed considerably in the modern era, though. Still, the average CAPE ratio for the index since the start of the century (which includes the peak of the dot-com bubble) is 27.6. The current valuation is 40% higher than that.

S&P 500 Shiller CAPE Ratio data by YCharts. Month-end numbers. Current CAPE Ratio is 38.8 as of market close on July 24, 2025.

Here’s what’s happened every time stocks have been this expensive

There have only been a handful of times when the S&P 500 traded at a CAPE ratio above 30. Two of the most notable instances were in 1929, just ahead of the Great Depression, and between 1997 and 2001, the height of the dot-com bubble.

Note that the CAPE ratio only exceeded 30 for a couple of months in 1929 before the stock market crashed, kicking off the Great Depression. By comparison, the S&P 500 continued to climb higher for years after breaching the threshold in June of 1997. Eventually, however, there was a massive decline in stock values, with the Nasdaq Composite falling 77% from its peak.

In the three other recent periods when the S&P 500 CAPE ratio exceeded 30, the index went on to drop 20% or more each time: in 2018, 2020, and 2022. With the CAPE ratio pushing toward record territory, it looks like another 20% decline may be on its way.

Are stocks truly expensive right now, or is it different this time?

It’s worth noting that higher valuations have become the norm. And there’s a key factor to consider when determining whether the S&P 500 has become overpriced: interest rates.

Warren Buffett once wrote: “In economics, interest rates act as gravity behaves in the physical world. At all times, in all markets, in all parts of the world, the tiniest change in rates changes the value of every financial asset.”

One handy metric for comparing expected returns for stocks to fixed-income vehicles like bonds is the earnings yield. That’s simply the inverse of the P/E ratio. Investors can compare the earnings yield to the yield on debt instruments like government bonds to see if they’re getting good value.

Researchers Victor Haghani and James White prefer to compare the earnings yield to the yield on inflation-protected government bonds (also known as TIPS) as the best way to determine how much extra return someone can expect for taking on the risk of investing in equities.

They point out that the last time we saw the CAPE ratio climb nearly this high in 2021, TIPS yielded negative 0.7%. As a result, stocks still offered considerable excess expected returns. That didn’t stop the index from falling more than 20% in 2022, though, as interest rates climbed. When valuations rose during the dot-com bubble in 2000, TIPS actually offered a higher yield than the earnings yield on stocks. And sure enough, the S&P 500 produced negative real returns over the next decade.

Today, the earnings yield for the S&P 500 with a CAPE ratio of 38.8 is around 2.6%. Investors can get about 2% from 10-year TIPS right now. That puts the excess return for stocks at about 0.6%, which is relatively low.

So stocks do indeed look extremely expensive right now. Investors aren’t getting much excess return for the risk they’re taking on with equities, compared to “risk-free” government bonds that automatically factor in inflation.

That doesn’t mean investors should sell their stocks entirely and put all their money into bonds. A shift in asset allocation may be warranted, especially for those focused more on capital preservation. But most investors may simply want to focus on finding good values in the stock market. Despite the historically high CAPE ratio, there still remain plenty of great values in the universe of investable stocks.

Should you invest $1,000 in S&P 500 Index right now?

Before you buy stock in S&P 500 Index, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and S&P 500 Index wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $636,628!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,063,471!*

Now, it’s worth noting Stock Advisor’s total average return is 1,041% — a market-crushing outperformance compared to 183% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

See the 10 stocks »

*Stock Advisor returns as of July 28, 2025

The Motley Fool has a disclosure policy.

Disclaimer: For information purposes only. Past performance is not indicative of future results.