On Feb. 19th Thesis Gold (TSX-v: TAU) / (OTCQX: THSGF) delivered exciting news, following an excellent Pre-Feasibility Study (“PFS”). A second cornerstone investor is coming on board. AngloGold Ashanti is acquiring a 5% equity stake (with no warrants!).

In addition, Centerra Gold will top up its holdings to maintain its ownership percentage. Combined, the investment totals C$44M. In my view, this is much more than just a meaningful cash infusion, (did I mention no warrants?).

This is AngloGold’s second investment in a junior miner in Canada, it has no other projects or mines. The other junior stake was acquired three weeks ago (that stock is +40% on the news). To say that AngloGold picking Thesis Gold is a strong vote of confidence would be an understatement.

AngloGold is a C$76B company, 18 times the size of Centerra. It has a team of experts looking at Au projects around the world. The team presumably has looked at dozens if not 100+ opportunities in the past few years. It has pounced on just two.

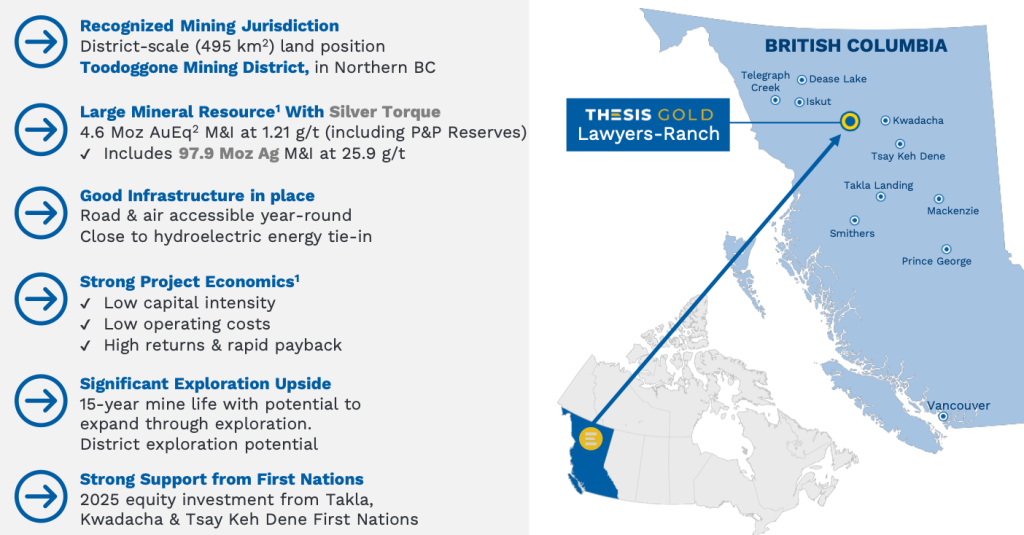

This is a strong technical & financial endorsement. A C$76B major committing capital validates the tier-one scale, geology, and development potential of the Lawyers-Ranch district, while signaling a deliberate shift toward stable, top-tier jurisdictions like Canada.

AngloGold’s involvement further de-risks Lawyers-Ranch and provides a notable stamp of approval, which could unlock broader institutional interest in Thesis. Equally important, the odds of B.C.’s Toodoggone district becoming a robust gold/silver mining hub just went up.

Until now, I imagined that Freeport McMoRan would eventually acquire Centerra and roll-up other companies/projects in the camp. Now, either Freeport OR AngloGold could be a consolidator. Why did AngloGold decide to jump in now?

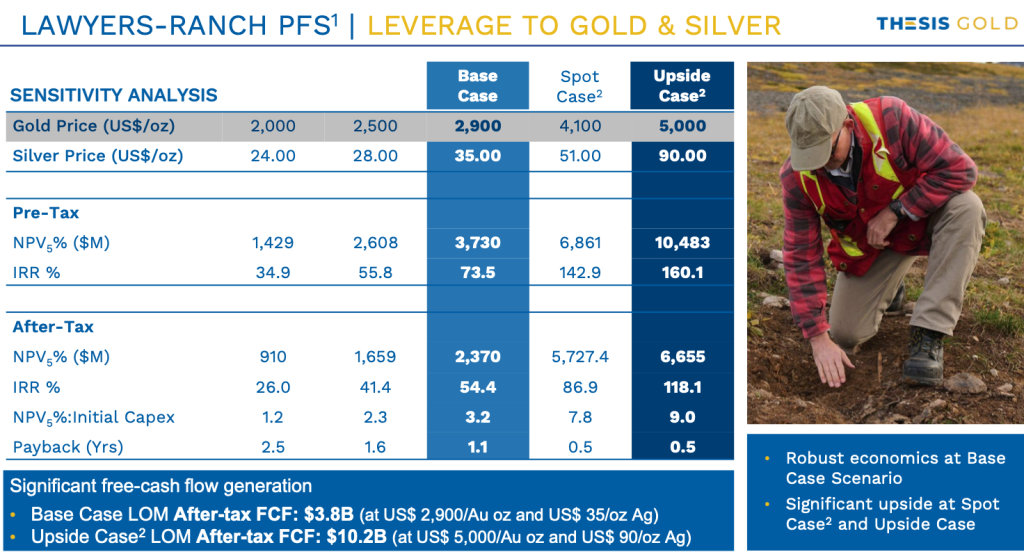

Clearly, the PFS economics attracted its interest. In the following image, using prices of $5,000 Au & $90 Ag, the post-tax NPV(5%) would be ~C$6.7B, with an IRR of ~118%. The payback period is well under a year. Note, Ag is now $78/oz.

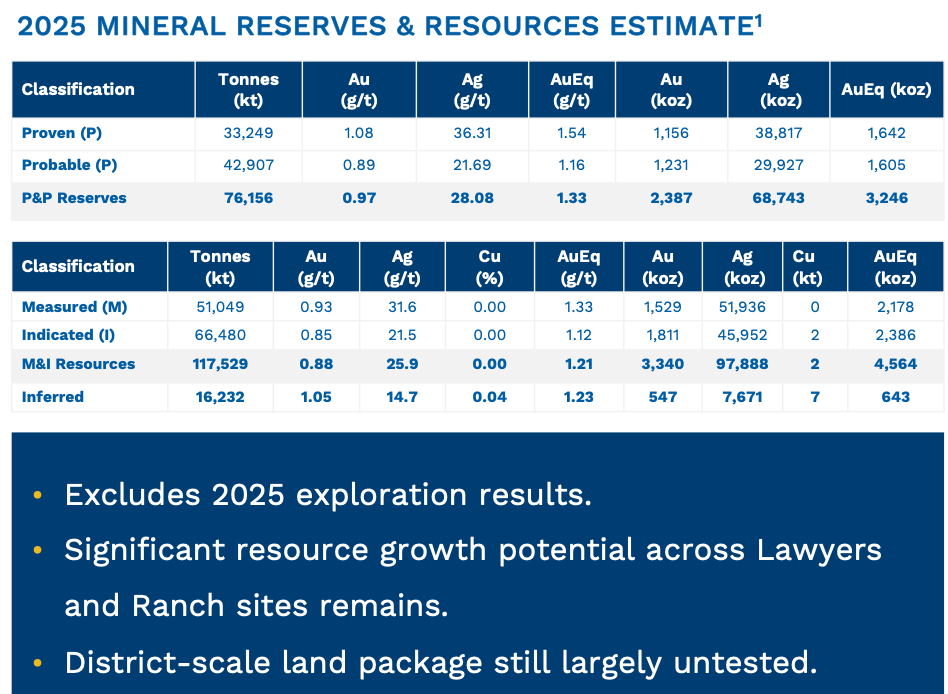

Importantly, at spot prices roughly 25% of revenue would come from Ag as there are ~105.5M ounces in the Measured + Indicated + Inferred resource categories. This is why the Company is rebranding with a new name –> Thesis Gold & Silver Inc.

At spot, the first full year of production (nearly 300,000 Au Eq. ounces) would generate post-tax free cash flow of ~C$1.2 billion. Yet, Thesis Gold’s fully-diluted enterprise value {market cap + debt – cash} is ~C$730M. Think about that… Wow.

These are tremendous economics, but are they only due to much higher precious metals? By far the largest contributor is pricing, but the mine life in the PFS was extended modestly, and annual throughput increased +9%.

Improved mine sequencing strengthened the economics. Optimization work pulled high-margin ore forward, and boosted mill throughput. The importance of the Ranch portion, prioritizing higher-grade underground feed, and stockpiling ore was established.

As a result, Ranch ore was moved into the first three years of production, and the underground cut-off grade was raised to 2.2 g/t Au Eq. to maximize margins.

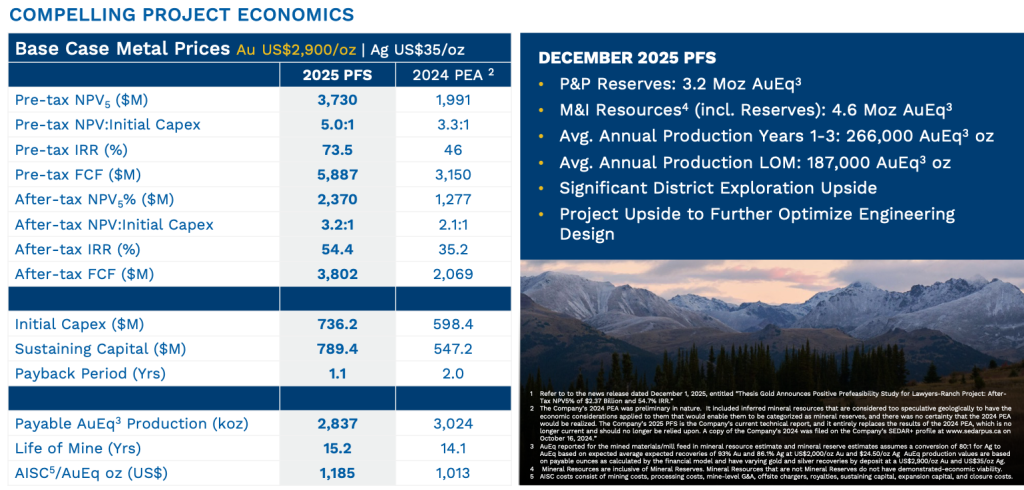

Operating costs, as measured by All-in-Sustaining-Costs (“AISC“) came in at a bottom quartile level of US$1,185/Au Eq. ounce, -27% below the industry median (f3q/25) of US$1,630/oz.

Op-ex & cap-ex are up from the PEA, but not that much, and a meaningful portion of the increases were due to enhancements in the mine plan. From the PEA the Au/Ag price assumptions are +50%/+52%, yet post-tax NPV was +86%.

I’m comforted by the fact that even if AISC rises to say $1,600/oz. in the coming years, project economics at $5,000/$78 would remain spectacular. I’m not suggesting it will rise by that much, but many producers are experiencing 5%-10% increases.

Interestingly, the day the PEA was announced in Sept. 2024, the Au base case was -23% below the prevailing Au level. On Dec. 1st 2025, the base case in the PFS was -32% below that day’s Au price, and now it’s -42% lower.

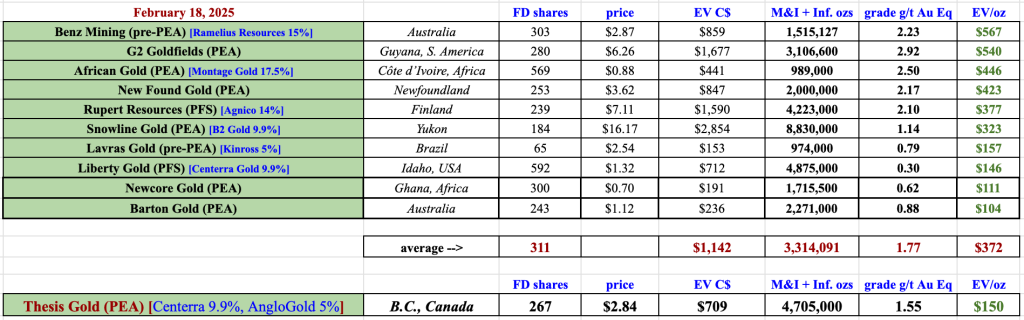

The ratio of NPV/upfront cap-ex came in strong at 3.2x, and at current prices, that ratio is ~8x! This is a highly attractive and comfortably affordable project that, (in my view), could be developed by any company valued north of C$5-$6B.

I count three dozen (mostly gold, some silver) producers that could pay a over a billion dollars to acquire Thesis, plus invest C$736M (cap-ex in PFS) over the subsequent 3-4 years.

The list of potential suitors is long, and almost certainly includes surprises. For example, Mexico’s Ag-heavy Fresnillo made an unexpected move into Canada by acquiring Quebec’s PEA-stage Probe Mining.

Of course, all of this may be a moot point now that Freeport, AngloGold & Centerra are front-runners to acquire Thesis Gold & Silver, but only on favorable terms to Thesis shareholders as we’re in the middle of an EPIC bull market for precious metals!

Centerra enjoys the best synergy opportunities, and would make itself meaningfully more attractive to Freeport, AngloGold or Newmont if it were to acquire Thesis and a few other juniors in the Toodoggone region.

Newmont dominates B.C.’s Golden Triangle. It could care about the Toodoggone district, there could be regional operating synergies to be gained.

Circling back to the PFS, a 15-yr. mine life that could be extended upon further drilling as the resource remains open along strike and at depth. Management is being careful about spending too much cash on delineating ounces that would only be added to years 16-20+.

Instead, they continue to look for exciting new discoveries & higher grade, near-surface mineralization that could be exploited in the initial quarter or third of the mine life. If a much larger player wanted to drill more aggressively, there’s plenty to be found.

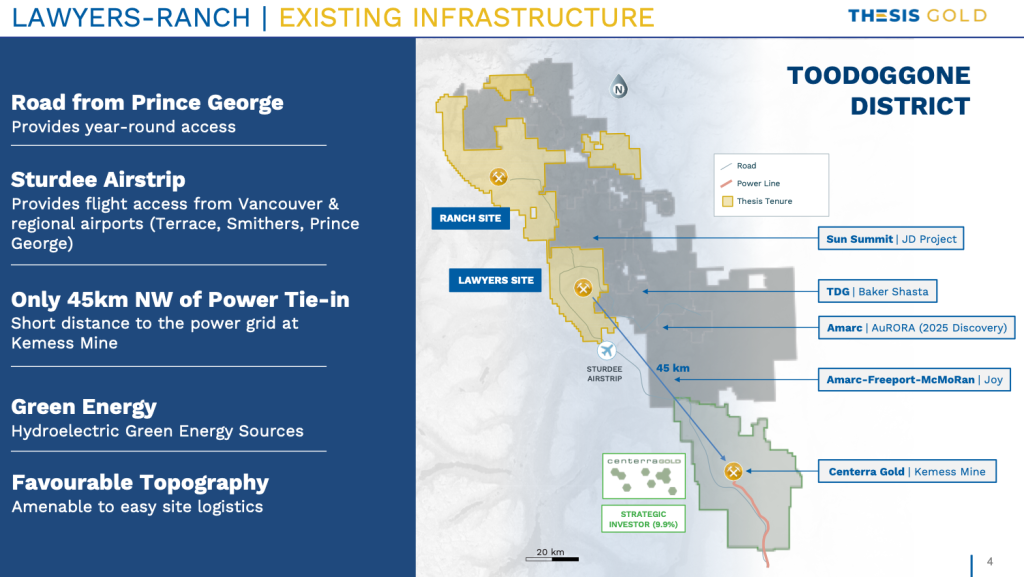

Expanding resource ounces on the Lawyers portion of Lawyers-Ranch has been compelling because there’s only a 0.5% NSR royalty on that property vs. a 2.0% NSR on Ranch. The vast majority of the current resource resides at Lawyers.

Numerous near-surface high-grade opportunities exist at Ranch. In the Project Upside section of the detailed Dec. 1st press release, other opportunities besides growing the resource size/grade exist between now and next year’s Bank Feasibility Study (“BFS“).

For instance, ore sorting at Ranch seems promising, (potentially enabling higher-grade concentrate to be trucked to a mill). The technical team is also exploring options to steepen portions of the open pit at Ranch.

Steepening pit walls reduces waste rock, (lowering the strip ratio, cap-ex & op-ex). More of the ore becomes economic, boosting NPV & IRR. As Inferred resource ounces are upgraded to Indicated, that will enable a mine life extension beyond 15 years.

Centerra’s experience in the district will be very useful, not to mention its ability to possibly help fund the BFS (C$5.1Bmarket cap, over C$1Bin net current assets at 12/31/25).

A key takeaway from the PFS is that ~300,000 Au Eq. ounces/yr is logistically feasible. Nearly that amount is slated for year 1.

If so, a potential acquirer could presumably (over time) expand to 20+ years at that level, making it a significant Canadian mine.

In a bull market for Au/Ag, and Canada anxious to fortify its economic/trade interests away from the U.S. due to the Trump Administration’s threats & bullying, I believe Centerra, Freeport, AngloGold and/or Newmont could potentially fast-track Lawyers-Ranch into production this decade.

Fast-tracking metals/mining projects is not unique to Thesis, other Canadian precious, base & battery metal plays could also be fast-tracked. However, Thesis Gold’s flagship asset has stronger metrics than many PEA/PFS-stage peers.

Thesis Gold & Silver meaningfully undervalued…

B.C.’s Skeena Gold & Silver, also Ag-heavy, is several years ahead of Thesis, and is fully-funded. Yet, it’s valued at C$681/oz in the ground vs. Thesis at C$109/oz.

The high-quality PFS meaningfully de-risks Lawyers-Ranch and Thesis Gold, yet the fully-diluted enterprise is just 12% of post-tax NPV(spot). A great project in a great jurisdiction, being advanced by a strong team and backed by Centerra Gold. It doesn’t get much better than that!

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Thesis Gold & Silver, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Thesis Gold & Silver are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Thesis Gold & Silver was an advertiser on [ER] and Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.