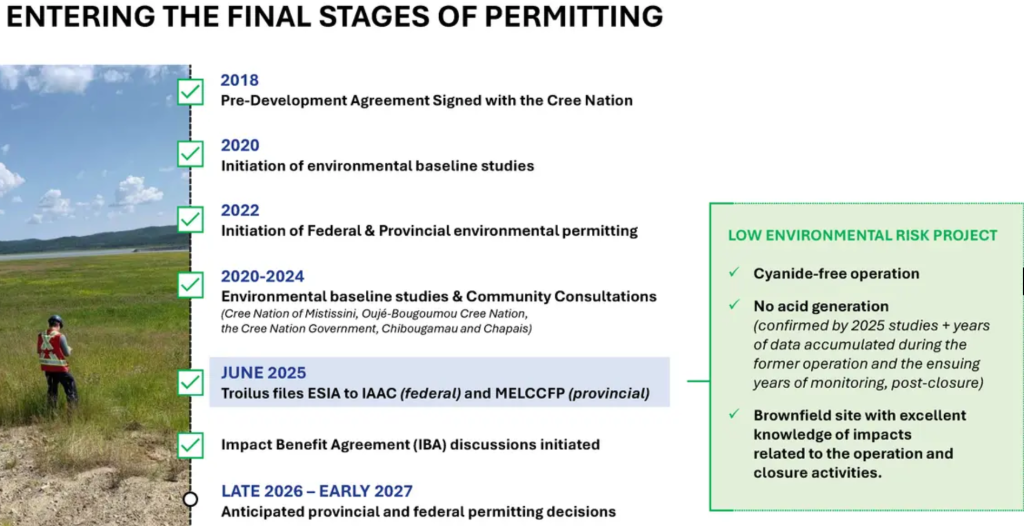

Troilus Mining (TSX: TLG) / (OTCQX: CHXMF) is an Au/copper (“Cu“) developer with a 13.0M Au Eq. ounce resource that expects to begin meaningful construction activities in Quebec within a year. Key permitting (federal + provincial) remains largely on track.

Troilus has a strong management team led by CEO Justin Reid. The share price has soared +268% from its 52-week low. Is the Company now fully-valued? In my view, it all comes down to peer valuation. Many peers have seen much greater share price gains.

Fuerte Metals, Cambria Gold Mines, Nevgold Corp., Banyan Gold, Hycroft Mining, Omai Gold Mines, White Gold, Belo Sun, Doubleview Gold, Benz Mining and Liberty Gold are up an average of +755%. These are not micro-caps, they have an average market cap of ~C$900M.

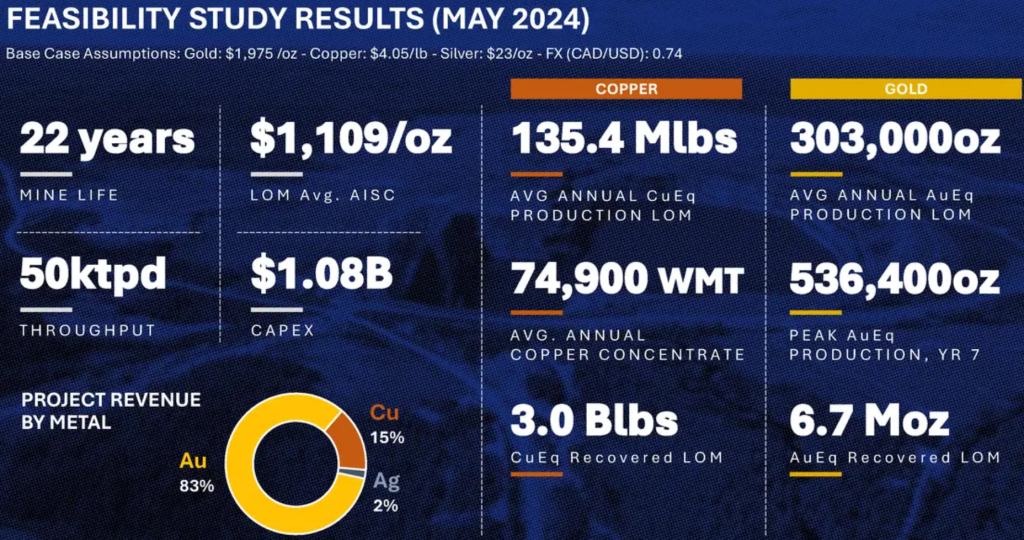

Backed by strong exploration results, ~C$140M in cash, recently completed plus upcoming engineering & permitting milestones, advanced-stage funding negotiations, and a strengthened leadership team, the 100%-owned, 435 km² Troilus Project in north-central Quebec is a globally significant asset that could enter production within ~3.5 years.

A construction permit is expected by 1Q/2027, and various permits/approvals are incoming. For example, on June 2nd Troilus announced approval of the Company’s request for a 70 megawatt power allocation. This is not SEXY news, but important.

Management is focusing on first pour in 2029 by advancing Troilus in parallel across technical, regulatory, organizational, and financial realms.

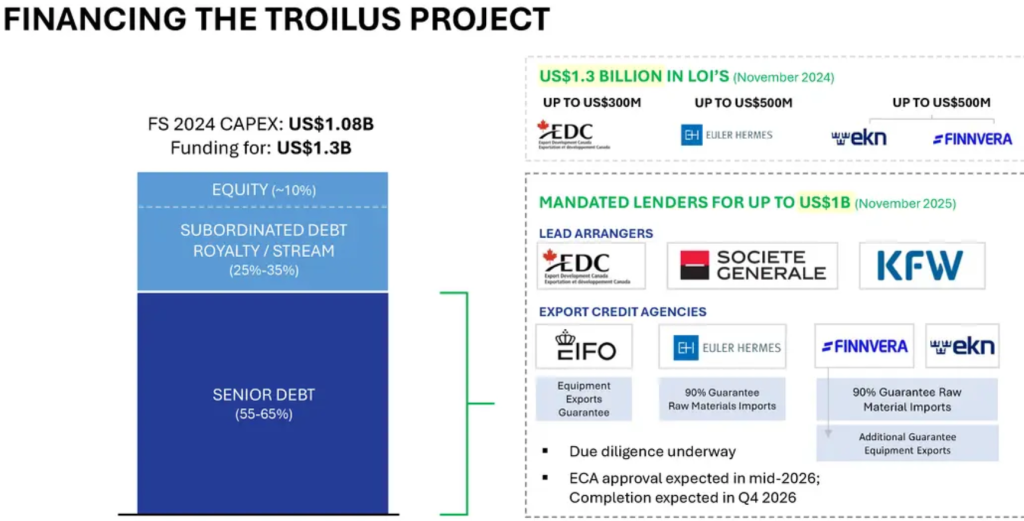

The Company has a signed mandate with three international banks plus EDC (Export Development Canada) for up to US$1.2B (recently upsized from US$1.0B) in senior secured debt, led by leading financial institutions, including; Societe Generale, KfW IPEX-Bank, and Export Development Canada.

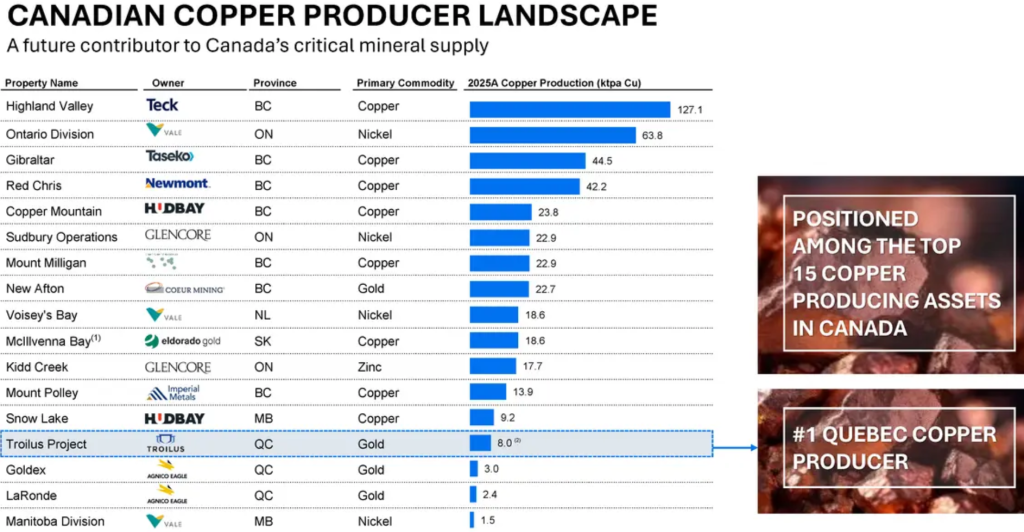

Interest from European smelters for Troilus Mining’s clean copper concentrate is strong and growing. The proposed mine, if operating today, would be the largest producer of copper in Quebec, see table below.

It’s important to recognize the substantial de-risking that has occurred in the past two years since the Feasibility Study was released. Troilus is a brownfield project that operated for 14 years. Management believes that existing infrastructure in place is worth more than US$500M.

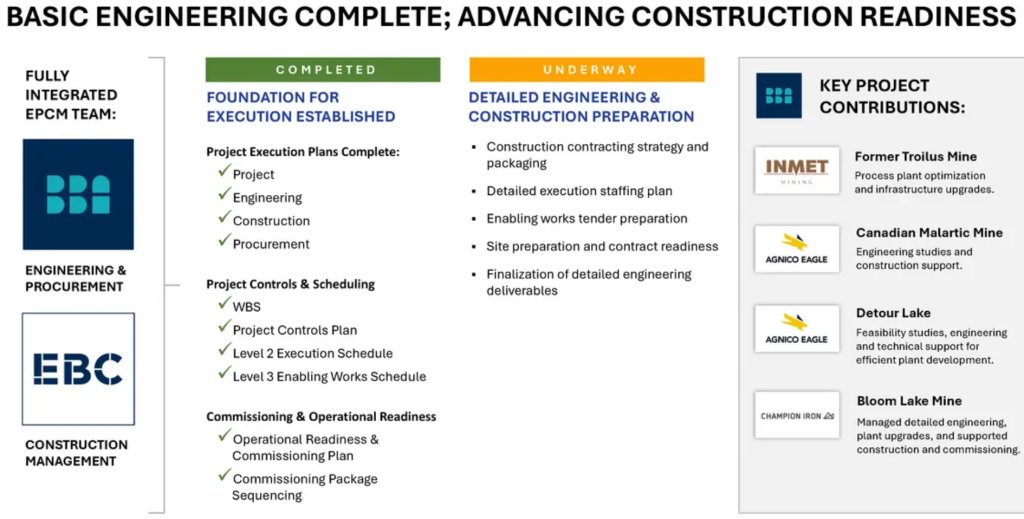

Basic engineering is complete, there were no negative surprises or red flags. Detailed engineering is well underway, tightening cost estimates from +/- 35% to +/- 10%. Long-lead items are now being ordered.

Importantly, the team is not waiting for final permits to advance this major Canadian Project. It has dozens of workers onsite full-time, including numerous engineers.

CEO Reid points out that higher fuel prices and mine cost inflation more generally will likely increase cap-ex & op-ex, but that’s true for every mine & development project on earth. He also noted good progress on mine optimization plans.

In an article I wrote last month, I detailed a few of the mine optimization / cost containing initiatives underway. The team continues to be optimistic, (subject to more work), about the potential outcomes. Ongoing efforts, like pulling forward higher-grade ounces, could lead to improvements in project economics to offset some of the cost pressures.

It seems likely to me that meaningful funding news is coming this quarter. That could be debt package finalization or a streaming deal, or both. Completing basic engineering was an important step for lenders/streamers… Note, Troilus might not need a streaming deal given the upsized debt package news, but it continues to weigh alternatives.

While some investors wish final debt & streaming transactions would move faster, the longer the wait, the higher the trailing 3-yr average Au/Cu/Ag price. The 3-yr trailing Au price is $2,984/oz. A year ago it was $2,196.The trailing 3-yr avg. for Cu is $4.60/lb. vs. $4.05 a year ago.

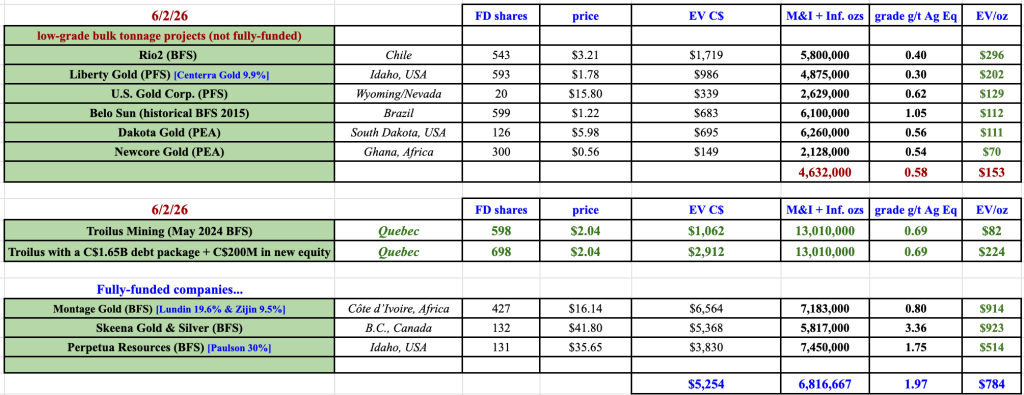

The following table shows Troilus Mining valued at a 45% discount to peer low-grade, bulk tonnage developers at C$82/oz. vs. $153/oz. However, 4 of the 5 peers are earlier-stage, (PFS or PEA). They face longer times to production and more equity dilution than Troilus.

As Troilus approaches funded status, note the bottom portion of the table. Assuming C$1.65B in debt and an additional C$200M in equity, (but no meaningful equity issuance before 2027), the pro forma valuation is C$224/oz compared to peer funded companies at an average of C$784/oz.

Granted, Skeena Gold & Silver & Perpetua Resources have higher grades, and Skeena will reach production perhaps 2 years ahead of Troilus, but the substantially discounted valuation of C$224/oz vs. C$784/oz is noteworthy. Notice Montage Gold’s jurisdiction… I prefer Quebec.

Recent evidence of a robust M&A environment, that I believe will only strengthen from here, can be found in the acquisitions of G2 Goldfields and Rupert Resources. Both are earlier-stage than Troilus, but each acquired by G Mining Ventures & Agnico Eagle, respectively, for more than C$550/oz in the ground.

Compare that C$550+ to Troilus at C$84/oz. G2’s (PEA-stage) & Rupert’s (PFS) flagship assets are in Guyana, S. America and Finland… I prefer Quebec.

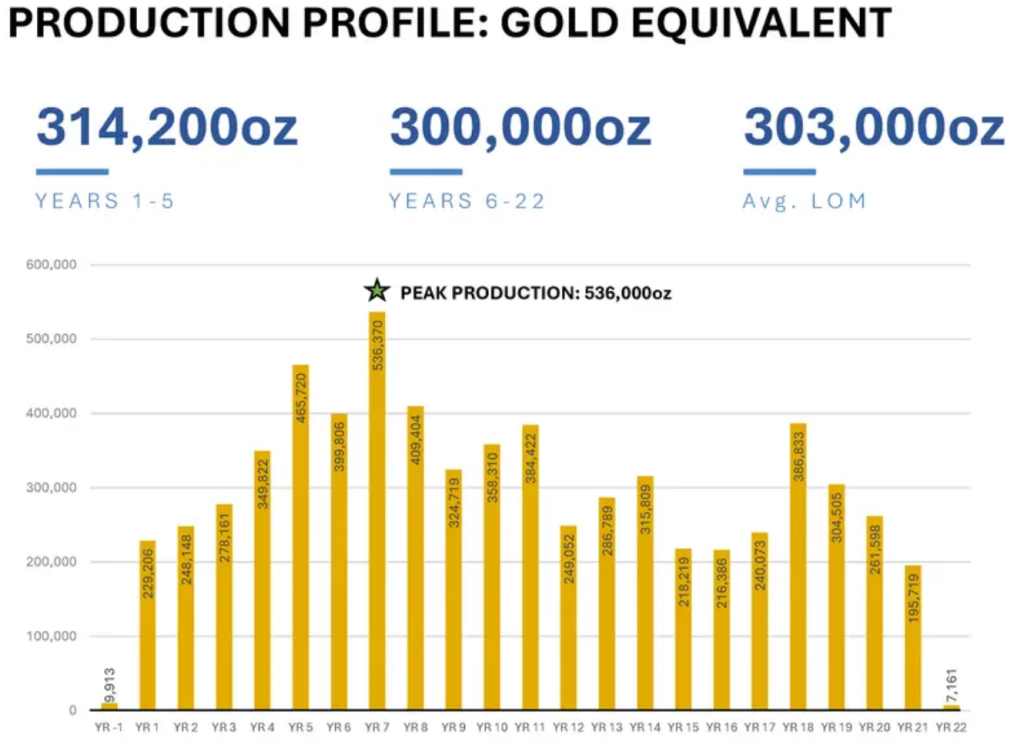

Assuming 300,000 Au Eq. oz/yr for Troilus (expected to be meaningfully higher in the initial years), $4,500/oz Au and an all-in-sustaining-cost of $1,500 (vs. $1,109 in the May-2024 Feasibility Study), EBITDA would be C$1.24B.

If a producer is looking to acquire Troilus, it could presumably increase production well above 300,000 oz/yr. As it stands, maximum production in year 7 of the mine plan is 536K Au Eq. At 400,000 oz/yr, EBITDA would be C$1.7B. How much might an acquirer be willing to pay for strong cash flow like that for 20+ years?

How many new mines, anywhere in the world, that could commence production this decade, have 20+ years of 400,000 oz/yr potential? Collectively, Au producers are now generating tens of billions/yr in free cash flow. There will be a tsunami of M&A. It may have already started. Troilus should be of keen interest to, Majors and larger producers like,

Agnico, Newmont, Barrick, AngloGold Ashanti, Gold Fields, Kinross, Lundin Gold, and Alamos Gold, but also a few dozen smaller, but financially strong, producers with market caps of C$6B+.

As we await news on permitting and funding, readers are reminded that Troilus has already secured preliminary long-term off-take terms with leading European smelters including Aurubis AG & Boliden Commercial AB. This is an advanced-stage project. In my opinion, the chance of the Troilus project failing to become a mine is negligible.

In my view, ongoing progress in 2025 and 2026 distinguishes Troilus among many junior peers facing somewhat greater challenges in terms of jurisdiction, logistics, environment, social license to operate, and earlier-stage profiles.

Troilus Mining (TSX: TLG) / (OTCQX: CHXMF) is significantly undervalued to peer bulk tonnage companies, and very substantially valued to funded companies like Skeena & Montage and to the recent takeouts of G2 Goldfields & Rupert Resources.

I believe we’re weeks/months away from the start of major funding/permitting news that could prove to be key investment catalysts for the share price. Look at the comps table again, Troilus at just C$82/oz. Earlier-to-much-earlier stage Rupert Resources and G2 Goldfields recently acquired for over C$550/oz.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Troilus Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Troilus Mining are highly speculative and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. Readers assume and agree that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Troilus Mining was an advertiser on [ER], and Peter Epstein owned shares in the Company bought in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors, including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.