Trump ups the Ante—AND Systemic Risk—in His Fed Prosecution

Greetings, Investors. It’s certainly been a jam- and surprise-packed first year of Trump 2.0!

You need an intricate scorecard to keep up with it all: From tariffs, to conquering Venezuela, to bombing Iran (and threatening it anew), to dealing with a leftist insurrection in Minnesota (chiefly, among other hot spots) and much more, President Donald J. (“Thank You For Your Attention To This Matter”) Trump isn’t letting any grass grow under his feet.

This week will be especially interesting (or comical?) Having “attended” last year’s event remotely, The Orange Wonder will be present in Davos, Switzerland to mark his one-year anniversary and hold forth at the World Economic Forum.

Everyone is on pins and needles already, as you likely know, over Greenland.

Most recently, Trump (dressed specially for the occasion above) has made it known again that he believes that big, strategic and natural resources-rich island should be controlled or outright owned by the U.S.A. And his belligerence here is ramping up especially quickly, immediately including threatened, added economic tariffs and other actions against European nations who are balking at this for their own reasons.

I’ve explained how Trump’s various moves of late to prosecute his “Donroe Doctrine” vision aren’t as simple as just an impulsive crackpot and would-be dictator roiling the global “chessboard” just for the sake of doing so. As I shared along with my own recent Your Money Today podcast over Venezuela, Greenland, Cuba and the whole Trump approach, the BEST analyst on geopolitics I know—George Friedman of Geopolitical Futures—has likewise done a great job explaining what are far more complex issues than most understand.

Check out THIS YMT LINK and GEORGE’S PODCAST, respectively, if you want a SOBER and impartial analysis of all this (and ones NOT tainted by either “strain” of T.D.S.!!)

___________________________

Of all the battles Trump is waging, though, another that’s bubbled up anew is one we necessarily must look at uniquely: the nascent criminal investigation of The Federal Reserve and its Chairman Jerome Powell.

And I say that because none of these other things have the “money”—outright or implicitly—to move forward without the Federal Reserve being the de facto enabler of all the associated borrowing and spending.

Simply put, if Trump loses the markets–especially the bond market–everything else will be called into question, weakened, or rendered mathematically impossible.

To date, Trump has waged on-and-off rhetorical battle with Powell: often childish name-calling and more over Trump’s insistence that Powell has not cut rates quickly enough let alone to the magnitude he thinks they should be cut. The president as you already know has made no secret of the fact that he wants interest rates pushed all the way down to one percent or so; something he says the U.S. “deserves” for having the greatest economy (and president, lest you forget!) in the history of the solar system.

That such a strong economy, if the official numbers are to be believed, doesn’t need lower interest rates is lost on him.

That Trump has been carping for “help” from the Fed and/or setting Powell up as the scapegoat in the event the economy’s weakness suddenly broadens (he’s far from the first president to behave that way) is not unusual. What is unusual is the news that came out recently that the U.S. Attorney for the D.C. Circuit (former Faux News pundit and Trump ally Jeanine Pirro) is investigating Powell for, ostensibly, alleged lies he told Congress last year over the cost to refurbish the Fed’s Eccles Building H.Q., the cost overruns thereon and such.

Now, first off, this explanation at least as far as it includes the president’s own views on the matter is laughable: not because nobody should be allowed to lie to Congress, but because it shows how selective Trump is about who wastes what.

Most notably, consider that the U.S. Department of Defense (er…WAR) has NEVER PASSED AN AUDIT. The money gone through by the Military-Industrial Complex dwarfs anything Jerome Powell and his reconstruction project ever contemplated.

Yet Trump wants to reward–not have prosecuted–all these types by massively increasingly the already-obscene $1 trillion annual (rounding it off) war/trouble-making budget by 50% next year to $1.5 trillion all in one fell swoop!

So “wasting money” as always in The Swamp counts for some but not for others.

Let’s all be real about what IS at stake with this pressure on the central bank, together with Trump’s (limited to date) efforts to so “stack” the central bank that he’s more likely to get his way:

—> Whether the economy needs it or not, the Treasury is facing an imminent crisis—together with the global payments system—due to the level of interest rates against already-choking debt levels.

Sometimes, Trump beats around the bush a little on this, admitting that the Fed is “costing” the U.S. many billions more than necessary in interest on the nearly $39 trillion national debt now. That of course is technically true, at least to a point.

But The Orange Wonder should also look in the mirror, as he has utterly failed in his first year to rein in the cost of government and its deficits for the most part, allowing Congress to continue spending at Biden era “emergency” levels…and throwing Elon Musk and his worthwhile DOGE efforts away.

The issue is FAR more dire and immediate than even Trump understands (or seems to) in his diatribes. This year alone, an outsized $8+ trillion of that $39 trillion comes due and needs to be rolled over; and at considerably higher interest rates even on the present short end of the yield curve. Having not that long ago cracked the $1 trillion mark (annualized), the annual interest payments on the national debt are set to reach at least $1.5 trillion THIS YEAR.

It is an untenable situation.

One of my favorite experts on monetary policy and related matters said this recently in addressing the dire nature of the PRESENT fiscal and funding crisis:

“Even when you remove Powell from the picture entirely, the Fed’s influence was already on a glide path lower. In an era of fiscal dominance, the Fed’s influence shrinks almost automatically. Once debt gets large enough and deficits stop being cyclical and become permanent, monetary policy can’t operate freely anymore. Rates stop being a clean policy lever and start getting boxed in by the need to keep government financing manageable and the financial system from breaking. Push rates too high and you risk detonating debt service costs, stressing banks, breaking markets, or forcing Congress and Treasury to step in. At that point, fiscal reality quietly sets the boundaries, no matter how independent the Fed sounds on paper.

“That trajectory didn’t depend on Powell, and it won’t change when he’s gone. Aging demographics, entitlement math, defense spending, and chronic deficits all point in the same direction..policy has to accommodate financing needs. You can already see it playing out..cuts will come onto the table sooner, price pressures are allowed to run longer, balance sheet tools do more of the heavy lifting than rate moves, and working hand in hand with Treasury stops being optional. The Fed doesn’t suddenly lose its authority; it loses flexibility. And once markets understand that, monetary policy becomes less about credibility and more about managing constraints. That’s fiscal dominance in real time.” (Emphasis added.)

Noting especially the italicized portions of that above sobering, meaty yet succinct reality check, it helps you understand why the Fed in December only grudgingly gave us the last (for the time being) 25 bp rate cut while at the same time resurrecting Q.E. and removing the limits to its open market operations. (NOTE: I addressed that among other things with Michael Fox on The Prospector Podcast right after that Fed meeting; LISTEN HERE.)

—> Here, my friends, is a major irony that suggests Trump might have really screwed up in reverse this time: and that is, he’s made it MORE, not less, likely that 1. The Fed stays reluctant to lower the federal funds rate much further and 2. Powell not only stays at the central bank but remains chair beyond that term’s expiration in May.

There are few things the Uniparty on Capitol Hill agree on these days: but one of them is the “independence” of the Fed and the sacrosanct nature of the fractional reserve system that has enriched most all of them, their campaign donors, etc. So, FAR beyond the questionable fight President Trump has picked anew with an ossified Europe and N.A.T.O. over Greenland (and on which, I.M.O., he has the upper hand more so than not) he’s thrown down against a much more considerable opponent in “attacking” the Fed and threatening its “independence.”

This comes at a perilous time on a few fronts.

First, as mentioned above, the gargantuan refinancing and financing (for the present year’s $1.5-$2 trillion deficit to boot on the latter) needs for the Treasury are keeping upward market pressure on interest rates. Trump makes that worse when his actions here suggest to potential buyers of Treasury paper that the credit/event/inflation risk of the I.O.U.’s of the world’s reserve currency are getting worse rather than better.

This only emboldens the Bond Market Vigilantes as they keep upward pressure on long-term Treasury yields in particular, correctly demanding higher returns for the added Trumpian risks.

Indeed, as you see below, as of this writing the Treasury market seems to be breaking out to the upside on the interest rate for the bellwether 10-year Note (last Friday’s close north of the key 4.2% level I’ve been pointing out.) I expect this to continue, as I have been warning for the past few months now especially; and if it does, pretty much everything else is going to start coming under some pressure.

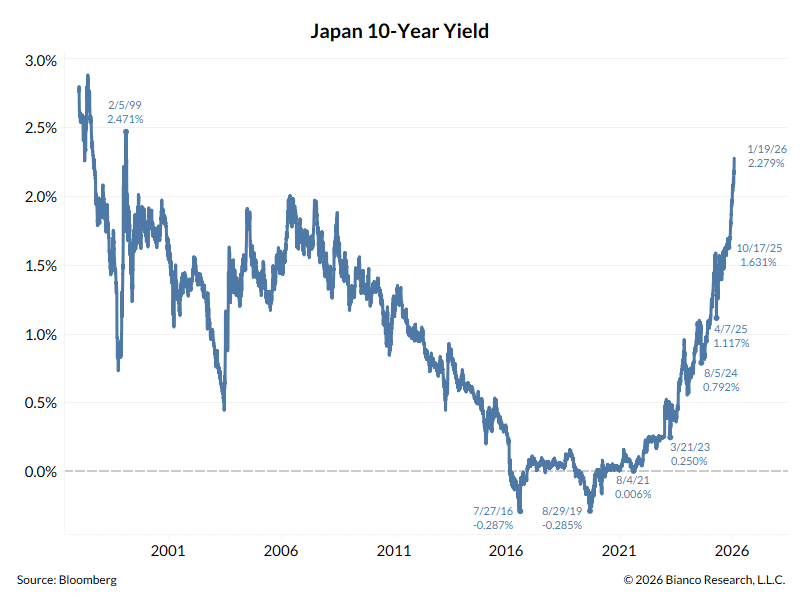

AND…I’ve pointed out since last spring, if you recall, that Japan–in even more dire straits on this front–has been the proverbial canary in the coal mine as the global game of financial repression since 2008 nears the end of its effective life.

Below is the latest from there:

Market yields in Japan continue to surge as the jig is REALLY up in that nation. This has already caused the Bank of Japan to start RAISING short term interest rates to prevent an uncontrollable currency crisis and soften the unfolding debt one.

President Trump was already fated with having the similar dynamic creep up on him. Now, he’s accelerating it.

Simply as a matter of optics—all else being equal—the central bank is going to want to prove (by continuing to sit on its hands for a while) that it’s not giving in to Trump’s pressure.

Politically, Trump has created a huge, added problem for himself ahead of nominating his desired successor to Powell. Key members of the Senate Financial Services Committee have said that they won’t vote for ANYONE to replace Powell until this lawsuit/associated threats have gone away. One of them is Sen. Thom Tillis (R-NC) who 1. Dislikes Trump and 2. Decided not to run again this year and is thus a lame duck and not able to be coerced.

All this means that if Trump and his Administration go forward with this “attack on the Fed’s independence,” NOBODY is going to be confirmed to replace Powell as chairman.

And in such an event, you’ll see a majority of his comrades vote to keep him as chairman until a replacement is duly confirmed. So far, save for the beginning of a breakout in Treasury yields and precious metals remaining near their highs even as they looked ready to correct more prior to the Fed news from Trump, markets have reacted little to this. Don’t count on that continuing.

For those who want a much deeper dive into all this—and the reasons why you might be seeing a Fed rate HIKE this year, something just about NOBODY has on their Bingo Card for 2026—listen in HERE to my most recent podcast if you missed it prior.

All the best,

Chris Temple

Editor/Publisher

From the desk of Chris Temple — Monday, Jan. 19, 2026

Don’t forget that you can follow my thoughts, focus and all pretty much daily ! ! !

* On Twitter, at https://twitter.com/NatInvestor

* On Facebook at https://www.facebook.com/TheNationalInvestor

* On Linked In at https://www.linkedin.com/in/chris-temple-1a482020/

* On my You Tube channel, at https://www.youtube.com/c/ChrisTemple (MAKE SURE TO SUBSCRIBE!)