Table of Contents Show

Markets Weekly Outlook – Central Bank Focus as US Inflation Looms

Read More: EUR/USD: Additional accommodative monetary policy guidance from the ECB may be forthcoming

Week in Review: Jobs Data All but Confirms a December Rate Cut

A week that saw a lot of choppy price action as markets awaited the US jobs report on Friday. A stellar jobs print of 227k and a slight uptick in the unemployment rate to 4.2% appear to have sealed a December rate cut.

Source: LSEG

Barring any crazy inflation surprise in the week ahead, markets appear fairly certain that the Fed will deliver a 25 bps cut in December. Federal Reserve policymakers will enter a media blackout that kicks in on Saturday, in the run-up to the central bank’s Dec. 17-18 policy meeting.

US Equities have been the talk of the town once more, as Wall Street Indexes continued their impressive YTD performance. The S&P 500 and the Nasdaq hit intraday record highs on Friday while the Dow struggled following a drop in UnitedHealth shares.

The ‘Santa rally’ appears to be here with the S&P making its way above the 6100 handle and the Nasdaq eyeing consolidation above the 21500 handle. Following the day’s move the S&P and Nasdaq are on course for a third consecutive week of gains with the Dow on course for a minor setback.

Oil prices struggled this week despite OPEC + continuing their current production cut schedule into 2025. The Organization of the Petroleum Exporting Countries (OPEC)+, pushed back the start of oil output rises by three months until April and extended the full unwinding of cuts by a year until the end of 2026

Following a choppy week, Oil was trading down around 1% on Friday and on course to finish the week down around the same. Bank of America forecasts that increasing oil surpluses will drive the price of Brent to average $65 a barrel in 2025, while expecting oil demand growth to rebound to 1 million barrels per day (bpd) next year, the bank said in a note on Friday.

Gold remained rangebound for the majority of the week, as the precious metal coiled in a $40 range between 2612-2660. Not even Friday’s jobs data was enough to shake the precious metal into a breakout.

The DXY had a mixed week with a strong start and end to the week followed by a soft middle leaving the DXY on course for marginal gains of about 0.35%. This was reflected in the choppy price action by major pairs this week with the Euro and the GBP unable to hold onto gains against the Greenback.

The DXY will be worth monitoring given the US Dollar has a track record of poor performance in the Month of December. An uptick in US inflation however could aid the Dollar in its bid to reclaim the 107.00 handle next week.

The Week Ahead: US Jobs Data to Dominate

Asia Pacific Markets

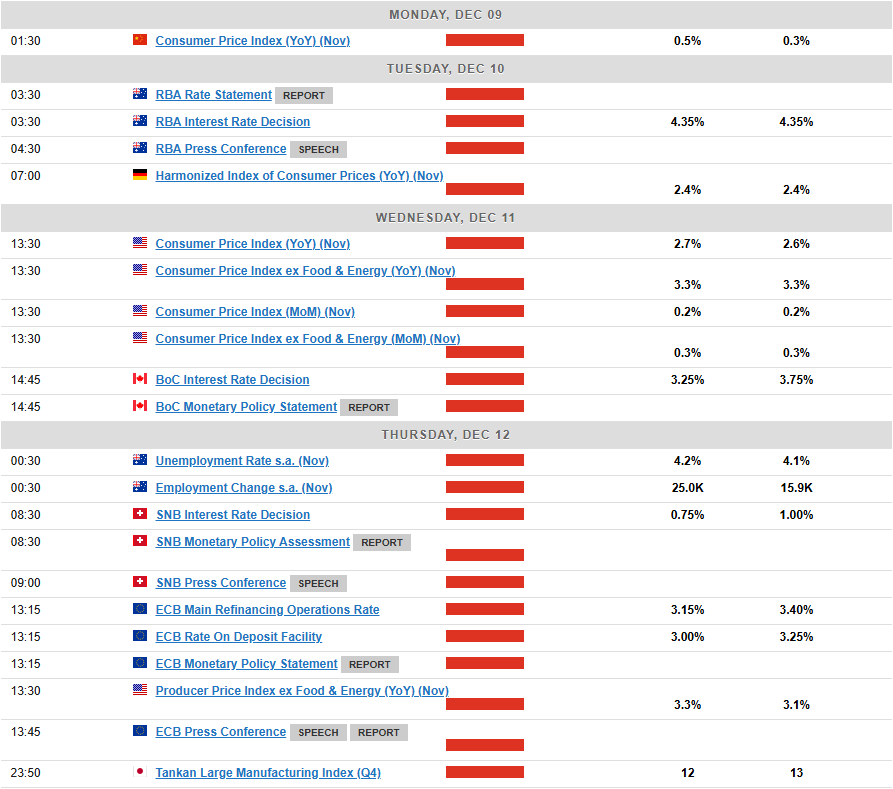

The week ahead in the Asia Pacific region sees some key economic data releases and events.

In China, the big event next week is the annual Central Economic Work Conference. While it won’t focus on exact numerical targets (those are usually set during the Two Sessions), it will give clues about how policymakers are planning for next year. This could have an impact on emerging market currencies and currencies like the Australian Dollar as well.

The better question would be whether there’s any change in their approach to fiscal policy or monetary policy.

China will release its November inflation data on Tuesday and trade numbers on Wednesday. Inflation could very well rise to 0.6%, from the previous 0.3%. Imports are likely to stay weak due to low domestic demand, growing only around 1.2%.

In Australia, the RBA is expected to keep rates on hold this week at 4.35%. The uptick in October core inflation coupled with stronger economic growth in the third quarter suggest the RBA isn’t in a hurry to lower rates.

In Japan, the Tankan Business Survey will be out this week. This comes as speculation continues to grow that the BoJ will deliver a rate hike of 25bps at its upcoming meeting. Something else to pay attention to may be the manufacturing sector, which may face challenges due to growing uncertainty around global trade policies, especially in the auto industry.

Europe + UK + US

In developed markets, the focus moves back to the US and CPI inflation data as speculation grows around a December rate cut.

Core CPI is expected to rise by 0.3% month-on-month again, which could complicate the December decision for the Federal Reserve despite the probability of a rate cut lingering around the 80% mark.

Policymakers agree that policy remains restrictive and the sticking point seems to be over the pace of cuts. I do still think the idea of Trump assuming office will play in the minds of policymakers who will likely cut in December and take a pause in January.

In Europe the ECB decision is due this week with any doubt around the size of a cut seemingly evaporated. A recent bout of data and comments from policymakers have seemingly ruled out the possibility of a 50 bps cut with 25 bps the most likely outcome.

To show they remain committed to managing rates effectively, the ECB is likely to signal that it plans to keep moving rates towards neutral levels and is open to lowering them further into easing territory if needed.

The Bank of Canada has lowered its policy rate by 125 basis points since June, and there’s a strong chance it will cut another 50 bps next week. This would bring the rate down to 3.25%, as the central bank tries to reach a neutral level quickly.

The cuts are needed as Canada struggles with slow economic growth and low inflation. There are other challenges as well while the looming threat of a Trump Presidency and tariffs when he takes office also weighs on the minds of BoC officials.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

Chart of the Week

This week’s focus is now on the Nasdaq 100, following another stellar showing by US equities. The ‘santa rally they say’, looking good so far.

The Nasdaq 100 is now within 400 points of the 22000 handle following a strong end to the week as US jobs data seemed to confirm a December rate cut.

The Nasdaq is currently in a channel and the top of the channel is around the 22000 handle which would make that a key area of resistance. Before that level however the 21750 handle may also present challenge. The Nasdaq monthly open was around 20930 with the index already rising around 700 points this month.

Any pullback may be viewed as a potential opportunity for buyers to get involved. The historical performance of the index in December coupled with the current fundamentals suggest we may see more upside before the month comes to a close.

My bias remains bullish for the Nasdaq but getting involved now would pose the risk of a correction before the next leg to the upside.

Nasdaq 100 Daily Chart – December 6, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

Resistance

Follow Zain on Twitter/X for Additional Market News and Insights @zvawda

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

")

")

:max_bytes(150000):strip_icc()/GettyImages-2181015208-73d683d5f5ab4b35a8c0f0de12d23b47.jpg?w=332&resize=332,0&ssl=1 "Analysts Anticipate ‘Strong’ Costco Could Announce Stock Split Ahead of Earnings Report")

:max_bytes(150000):strip_icc()/GettyImages-2181015208-73d683d5f5ab4b35a8c0f0de12d23b47.jpg?w=664&resize=664,372&ssl=1 "Analysts Anticipate ‘Strong’ Costco Could Announce Stock Split Ahead of Earnings Report")

Targets ,700 Amid Anticipated Fed Rate Cuts and Geopolitical Tensions")

Targets ,700 Amid Anticipated Fed Rate Cuts and Geopolitical Tensions")