Table of Contents Show

- Fed policymakers maintain a dovish stance, and market participants are pricing in a potential 50 basis point rate cut in November.

- The US dollar hit a fresh YTD low, while Gold and Silver continued to advance.

- The week ahead features key data releases, including Eurozone inflation and US nonfarm payrolls, which could shape central bank policies and market sentiment.

Read More: US Dollar Index (DXY) Slides to Fresh Lows Post PCE Data

Week in Review: Fed Policymakers Deliver Dovish Rhetoric

As the week wraps up, US data continues its downward trend, with the Fed’s preferred inflation measure maintaining pressure for a potential 50 basis point rate cut in November. Market participants are increasingly factoring in this cut, with the probability now exceeding 50%.

Source: CME FedWatch Tool (click to enlarge)

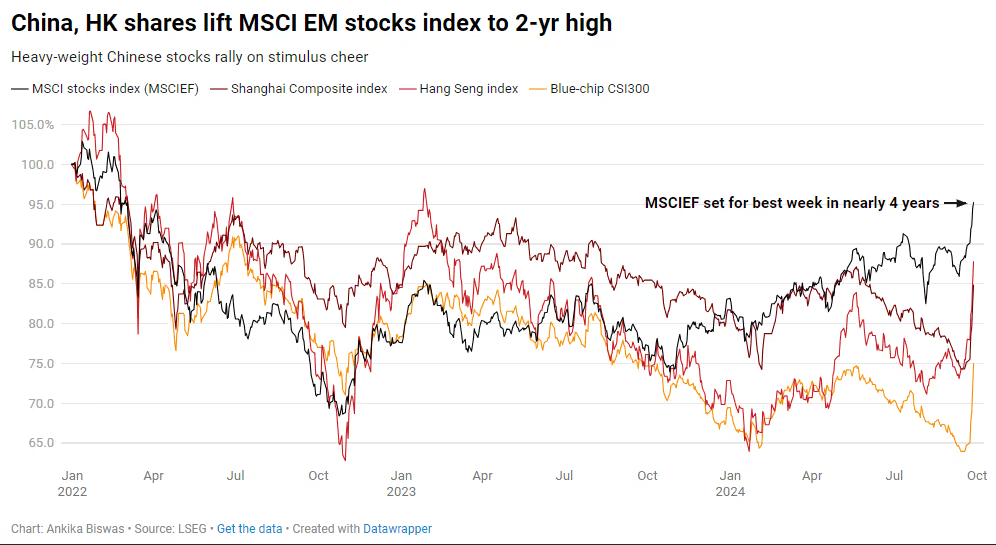

The week started with a stimulus package from China which helped propel Emerging Market (EM) stock indexes on track for their best week in 4 years. From South Africa to India emerging markets and EM currencies have done well and the Shanghai composite index logged its biggest weekly gain since 2008.

Source: LSEG Workspace (click to enlarge)

Comments from Fed Policymakers have struck a rather dovish chord of late which has emboldened market participants. The softer data from the US and uncertain geopolitical risks and tensions are also playing a key role in the current market dynamic.

No surprise that the precious metals arena continues to rise with both Gold and Silver rising this past week to fresh highs. Gold reaching a high of $2685/oz this week before a pullback has it languishing in the mid 2650’s at the time of writing.

Oil prices struggled to hold onto early week gains despite OPEC + updating its longer term outlook. The cartel says it sees peak oil demand to only be reached in 2050 as a result of emerging market demand. Brent traded at a low of around 71.00 on Thursday before a modest bounce ahead of the weekend.

On the FX front the US Dollar hit a fresh YTD low on Friday and struggled for the majority of the week. As things stand markets are now more dovish on the Fed than the ECB and BoE which have helped both currencies eke out impressive gains to the greenback.

This sets up an interesting week for Global Markets with the Euro Area inflation release and the US jobs report. Both events could be key in shaping the respective policies of each of the Central Banks with market participants fully pricing in a rate cut from the ECB in October. Will the Euro Area inflation report and US jobs report confirm such moves?

The Week Ahead: EU Inflation and US Jobs Data

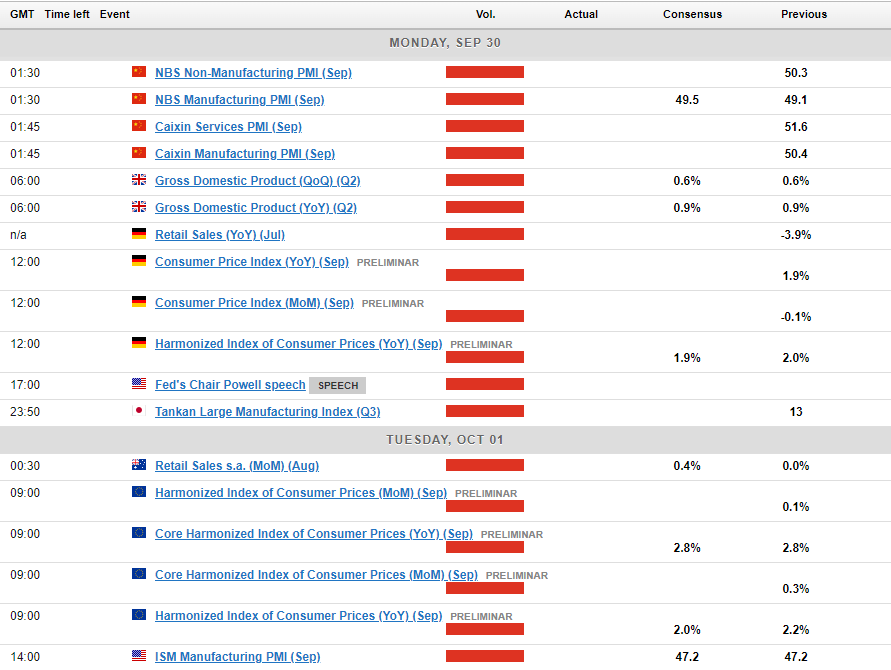

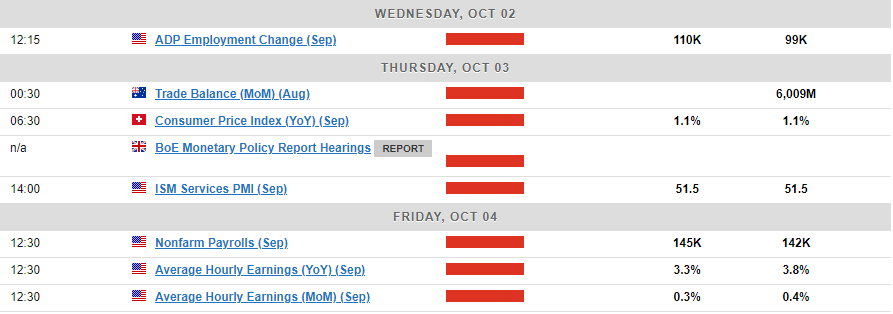

The week ahead is packed with high impact data releases in both developed and emerging markets. Next week, investors will have the chance to hear from numerous Fed members, including Fed Chair Powell on Monday. However, since the dot plot already provides a clear indication of the Fed’s future plans, upcoming data, particularly Friday’s non-farm payrolls, might garner more attention.

Asia Pacific Markets

In Asia, On Monday, China will release the official PMIs for September. In August, the composite PMI was at 50.1, barely above the 50 threshold that distinguishes expansion from contraction. It remains to be seen if business activity improved this month or slipped into contractionary territory. Of course it’s way too early to see if the stimulus will have an impact on actual production numbers as that will take some time to filter through to the data but the print will be an intriguing one nonetheless and could set the early risk tone for the week.

Japan has a new Prime Minister who is seen as someone who will support policy normalization by the BoJ and support Governor Ueda in his endeavor. The week ahead brings the release of the BoJ summary of opinions from the most recent Central Bank meeting. Governor Ueda stated that the BoJ will continue to raise rates if the economy aligns with their outlook. Consequently, investors might scrutinize the summary for clues about the likelihood of another rate hike before year-end.

Japan’s employment data for August, set to be released during the Asian session on Tuesday, along with the Tankan survey on Thursday, could also influence investors’ perspectives.

Europe + UK + US

In developed markets, Eurozone inflation numbers will be in focus as markets expect to see a further slowdown in inflationary pressure. This has ramped up bets of another rate cut from the ECB at its October meeting.

Unemployment figures are due next week and have remained at historically low levels for some time. While no immediate changes are expected, the labor market outlook appears to be softening, with labor shortages becoming slightly less of an issue.

In the UK, it’s a relatively quiet week with GDP data on Monday the only highlight. As cable holds the high ground, the week ahead could see a potential pullback ahead of the NFP release.

US markets are the most intriguing with ISM services and manufacturing data coming out before the all important NFP report. When it comes to the job market, recent benchmark revisions have shaken confidence in the data, while leading surveys on hiring demand are declining. Additionally, consumer confidence readings indicate that households are beginning to feel the effects of a cooling economy. A significant downside miss could weigh heavily on the US Dollar and thus reignite recessionary fears.

Unemployment rate at or below 4.4% would be ideal. Any uptick could further complicate matters going forward for the Federal Reserve and may have a massive impact on the size of the rate cut the Central Bank deliver in November.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

Chart of the Week

This week’s focus is on the S&P 500 given the recent rally and technical patterns at play.

The S&P is on course for its third consecutive week of gains and could face some form of correction next week. However the overall trend remains extremely bullish with the recent triangle pattern breakout hinting at a bullish target around the 6170 area.

The index may retest the top of the triangle pattern which rests around the 5650 handle before a potential move higher. This would be ideal for would be longs looking to get involved.

Immediate resistance on the upside rests around the 5910 handle before the psychological 6000 handle comes into focus.

S&P 500 Daily Chart – September 27, 2024

Source: TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

Resistance:

Follow Zain on Twitter/X for Additional Market News and Insights @zvawda

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

.jpg?w=332&resize=332,0&ssl=1 "What Are the Potential Rate Cuts by the Bank of Canada?")

.jpg?w=664&resize=664,372&ssl=1 "What Are the Potential Rate Cuts by the Bank of Canada?")