Are we in a super cycle for commodities like we saw in the mid-2000s? I don’t know, but many commodity prices have soared in the past year. Twenty years ago, it was all about Chinese demand. Now, in addition to China, it’s about security of supply and growth in India & Africa.

Security of supply is front and center as the West and East continue to diverge. China/Russia/Iran + other BRICs are exiting US$ investments and snapping gold. Largely shut out of N. America, Europe & Australia, they’re aggressively buying assets in Africa & S. America.

In a bull market, junior miners can offer attractive investment opportunities. A company that looks particularly promising is MetalQuest Mining (TSX-v: MQM) / (OTCQB: MQMIF). Founder/Dir./CEO Harry Barr has deep roots in Ontario (fourth-generation farming family since 1866).

Mr. Barr strongly believes in the improving geopolitical advantages of Canadian mining and the world being in a commodities super cycle. Mr. Barr personally holds ~28% of MetalQuest.

MetalQuest’s sister company, also founded by Harry Barr, is New Age Metals, a critical metals champion in lithium, gold, & antimony, with one of North America’s largest undeveloped palladium projects, located in northern Ontario. New Age is a 10% shareholder in MetalQuest.

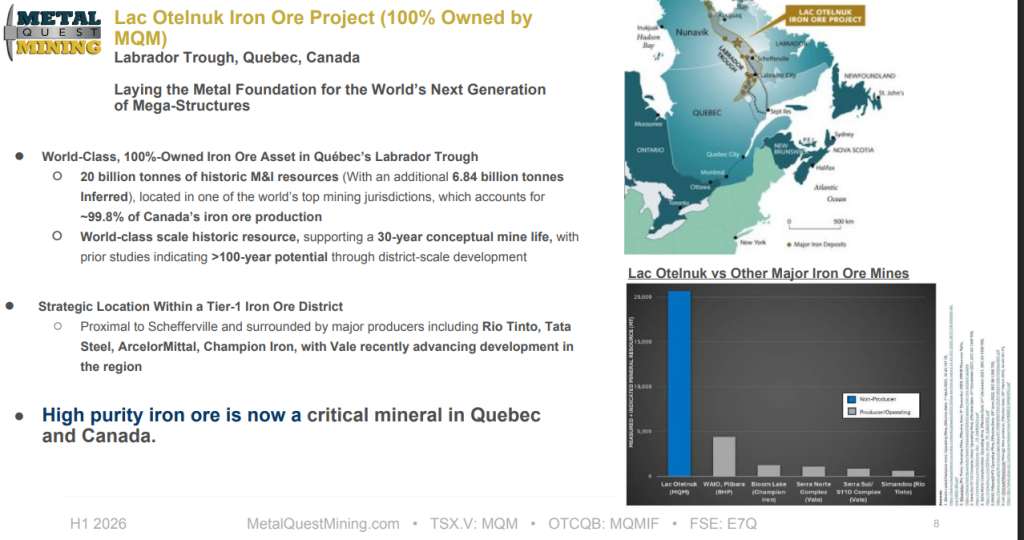

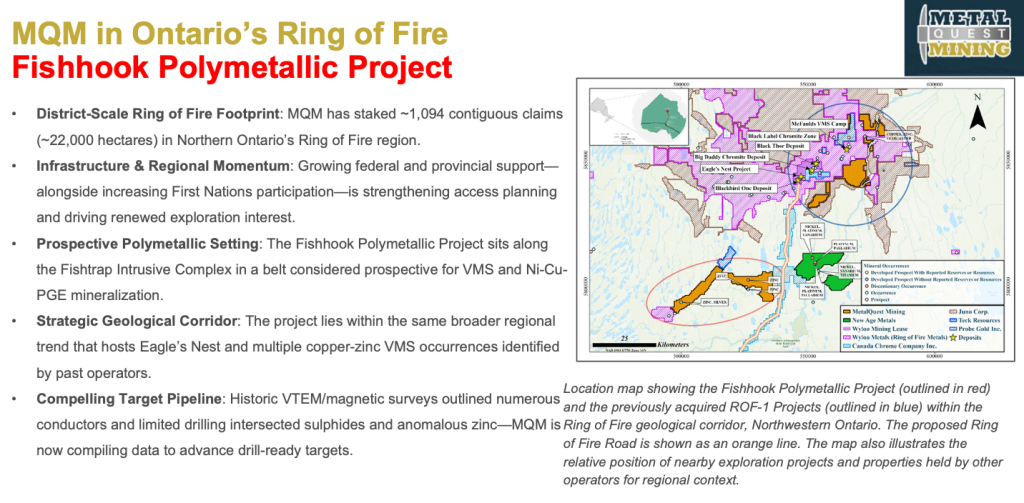

This article is about MetalQuest, owner of 100% of the Lac Otelnuk and Superior iron ore projects in northern Quebec, plus significant land holdings in Ontario’s world famous Ring of Fire.

The Company has a tight share structure, just 49M shares outstanding, and is cashed up with C$2.5M, including shares & warrants (deeply in-the-money) in Canadian Copper Inc, giving MetalQuest robust indirect exposure to copper & zinc. The Company’s enterprise value {market cap + debt – cash/securities} is ~C$9M (C$0.23/shr.).

Lac Otelnuk is North America’s largest iron ore project, and second largest on earth. It’s in the northern Labrador Trough (readers should note, most iron ore in Canada comes from the southern, infrastructure-rich part).

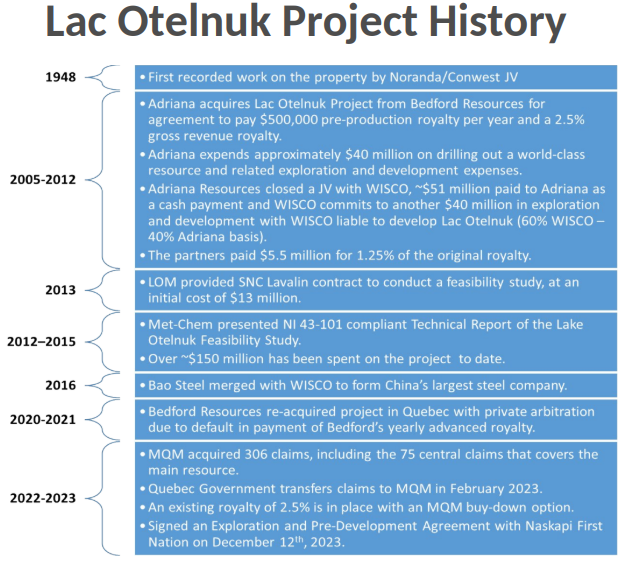

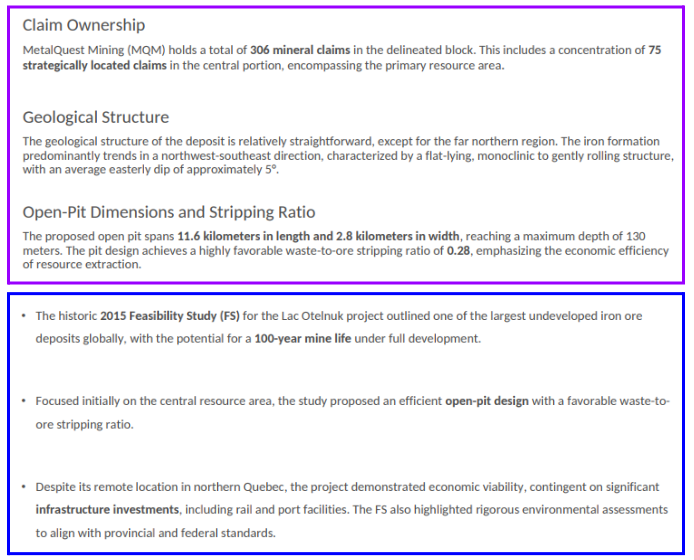

Mr. Barr believes that ~$170M has been spent on Lac Otelnuk to date. There’s an historic, but reasonably recent (2015) Bankable Feasibility Study (“BFS“) showing a 30-year of mine life (vs. a 100+ year total resource).

The Project was considered feasible using 2015 iron ore prices. Post-tax NPV(8%) was C$7.2B, and the IRR 13%. The iron ore price in that BFS was US$110/tonne.

Today, that same quality ore would be closer to $155/t. Does that mean the NPV & IRR would be meaningfully better? It depends on how much op-ex & cap-ex have increased, and to what extent the mine plan can be optimized.

Note, the US$/C$ exchange rate is 15% weaker since 2015, a meaningful tailwind for project economics as iron ore is priced in US$.

The same firm that completed the 2015 BFS, (AtkinsRéalis), conducted a gap analysis to show what’s needed for an updated BFS. Fourteen action items were identified. The results are being shared with prospective strategic partners, several of which are from Japan.

Over the years, including this year, there have been multiple management trips to Japan. Japanese firms including giant trading houses like Mitsubishi Corp, Mitsui & Co., Marubeni Corp., Itochu Corp., Sumitomo Corp., and Sojitz Corp. are interested in iron ore.

Japan is 100% import reliant and the third largest steel making country on earth. Therefore, it’s major steelmakers, including; Nippon Steel, JFE Steel, Kobe Steel, need millions of tonnes of high-quality iron ore.

Mitsubishi, Itochu, ArcelorMittal, Franco-Nevada, and Tata Steel have direct stakes in Canadian iron ore assets. Glencore, privately-held Gerald Group, Rio Tinto, Vale S.A., BHP, Fortescue Ltd., POSCO are also active in iron ore.

The considerable knock on Lac Otelnuk is a nearly C$20B cap-ex hurdle, (due in part to it being quite remote), and a long timeline until first production, probably the mid-2030s. However, this is only a problem for MetalQuest if it cannot secure a strategic partner.

Importantly, I believe a surprisingly large number of partners could step in for three reasons. First, Japanese commodity traders have grown substantially since 2015 (3x-6x larger), second, cap-ex would be deployed over 5-7 years, not all at once, and third, major groups have huge debt capacity (if needed).

And, it need not be just one strategic partner signing on. For example, of the numerous Japanese groups mentioned above, 2 or more could form a consortium to take on Lac Otelnuk.

Since 2015, high-purity iron from western-friendly countries has become increasingly prized for “green-steel,” (steel made with hydrogen or renewables to reduce steel’s substantial carbon footprint). Only high-purity iron like that from Lac Otelnuk is amenable.

I strongly believe CEO Barr will find a partner this year or next. Imagine if the Company could sell a meaningful stake in the Project and get free-carried through commercial production? Barr has made 43 deals with larger companies in his long career.

In my view, the net present value of the free-carry could be north of $100 million, and the residual minority interest might eventually be worth $100s of millions. Yet, MetalQuest has an enterprise value {market cap + debt – cash} of just C$9M.

A LOT (but certainly not all) of the Project’s risk profile could be mitigated by a strong partner with deep pockets, a long-term horizon, and iron ore experience.

I don’t mean to downplay the remoteness of Lac Otelnuk, but numerous major projects are remote, many are in Africa or Russia. All else equal, I prefer Quebec, Canada.

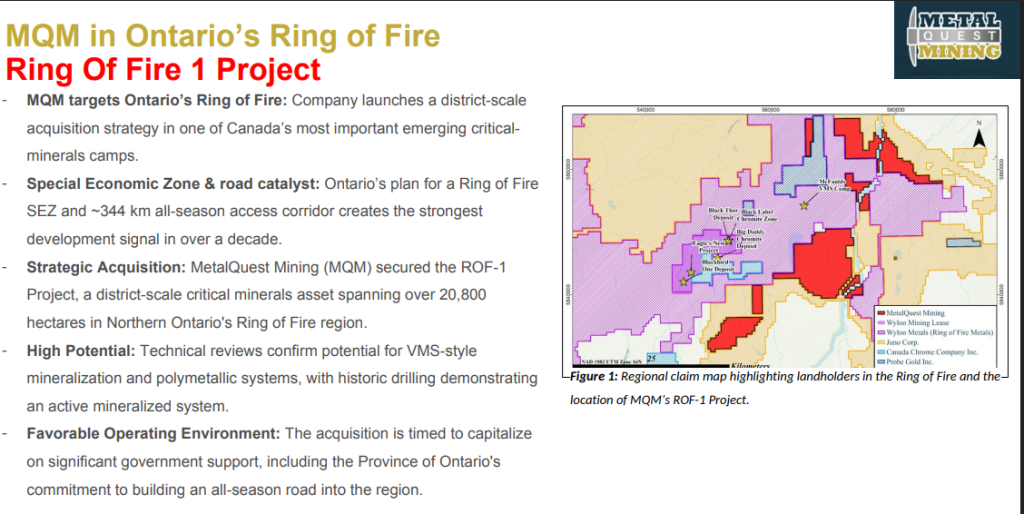

Moving on to the world-class, mineral-rich, Ring of Fire district, (“RoF“) north of Sudbury. Management states that ~$2–2.5 billion has been spent on drilling and discoveries across multiple commodities, but development was stalled by a lack of an all-season road, lower metal prices, and slow permitting.

There’s a land rush for properties in the RoF, with MetalQuest in the center of it. In real estate, when a major corporation builds a giant facility in town, surrounding housing stock soars in value. Likewise, a new all-season road in the RoF will make projects more viable, to the benefit of local communities and the Province.

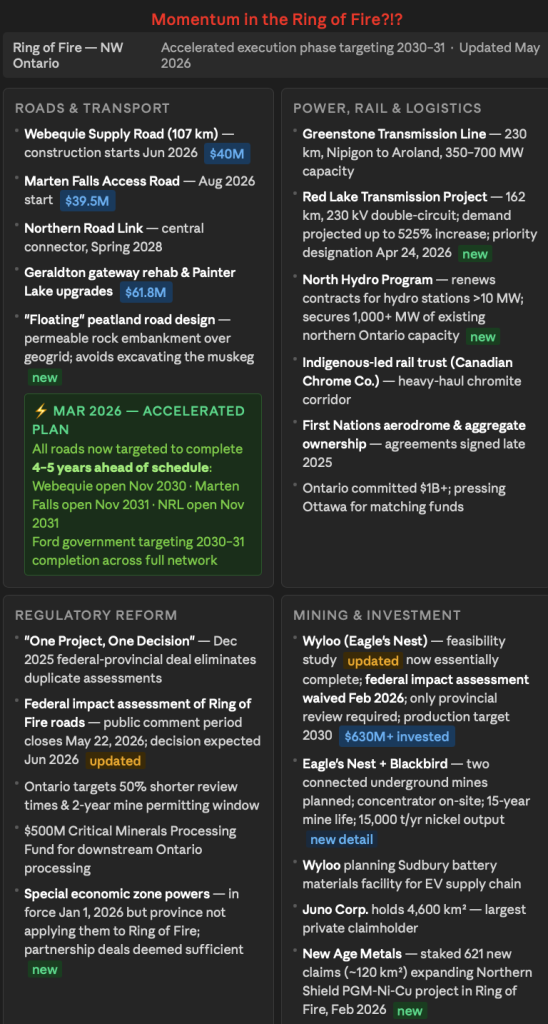

Importantly, in the past year the prospects for the RoF have meaningfully improved. Ontario’s Premier Doug Ford has finally committed to a major road project that could start construction this Summer, along with other significant initiatives.

Ontario is hot, gold Major Agnico Eagle just announced C$14B of investments through 2030. Look at the two RoF slides above showing MetalQuest’s recent activities. The Company has become a serious player in the area.

Admittedly, there have been false starts on pledged infrastructure builds dating back a decade or more. Why is this time different? Clearly, Canada can no longer rely on the U.S. for its economic wellbeing.

The transformation from economic & security ties with the U.S., to seeking closer alliances with Europe, Japan & India is not gradual. There’s a sense of urgency.

A busy image, considerable progress being made…

That means faster permitting times, real action not just words, for metals/mining, oil/gas & infrastructure projects. In my view, few areas stand to benefit as much as NW Ontario.

Bottom line: In my view, MetalQuest Mining is meaningfully undervalued due to its early stage and very large cap-ex requirements to build its 100%-owned, world-class iron project. While the cap-ex concern is understandable, readers are reminded that Harry Barr has done 43 significant transactions with much larger companies.

The Company could sell a stake in the Project and get free-carried until commercial production. Owning a minority stake in a Project worth billions would be a highly attractive outcome.

Mr. Barr will get something done on Lac Otelnuk. It might not be next month or next quarter, but a deal will be struck. There’s too much at stake for the Japanese and others in urgent need of LONG-TERM, SAFE supply of high-purity iron one for green steel production.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about MetalQuest Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of MetalQuest Mining are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, MetalQuest Mining was an advertiser on [ER] and Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.