Volvo Joins VERSES Genius™ Beta Program

3 Mins Read

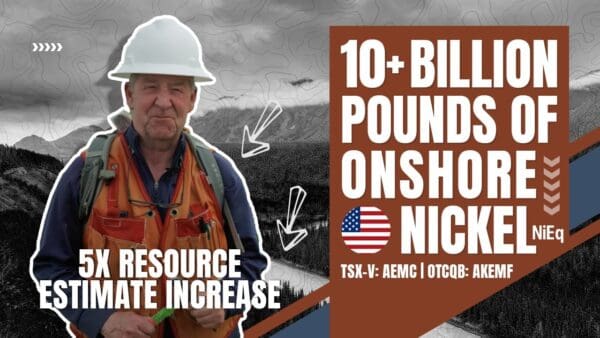

Alaska Energy Metals trading on the TSX-V-AEMC and the OTCQB-AKEMF has just released a substantially increased updated mineral resource estimate (MRE) on their Nikolai project in central Alaska. The market was generally expecting a double or triple of the existing maiden resource of ~1.5 billion…

Since the 1990s, Canada has been a leader in AI and deep learning, made possible by the research and innovations of the “Godfathers of AI”, Canadians Yoshua Bengio and Geoffrey Hinton. In fact, Canada has 10 percent of the world’s top-tier AI researchers, the second…

Gold is suddenly racing higher, powered by forces that have been building…

From The Maven Letter: 20 March 2024 AEMC’s share price has struggled…

From The Maven Letter: 13 March 2024 Why did gold suddenly shoot…

")

")

Bold, a financial technology company building an electronic payments infrastructure in Colombia, raised $50 million in Series C funding in a round led by existing investor General Atlantic. International Finance Corporation, a member of the World Bank Group, joined existing investors InQLab and Amador in the round. In total, Bold…

Kobold Metals – One of the largest mineral exploration companies in the world – backed by names like Bill Gates, Jeff Bezos, Richard Branson,…

From The Maven Letter: 20 March 2024 AEMC’s share price has struggled…

Fourth quarter and year ended December 31, 2023 Highlights

Palladium fell by 39% in 2023 after rising prices from 2018 to 2022 caused the…

The market is at a crossroads, transitioning into a new bull market. Investors should consider these unstoppable tech stocks for big gains.

")

")